System integration is one of the roles expected to emerge as a revenue opportunity as 5G private networks get traction, though perhaps the biggest opportunities remain in sales of infrastructure to support private networks, as is the case for Wi-Fi.

BT is moving to become a system integrator, inking a deal to sell, install and support Ericsson 5G gear to businesses and organizations in sectors such as manufacturing, defense, education, retail, healthcare, transport and logistics in the United Kingdom.

Revenue estimates for ecosystem participants can be substantial, representing double-digit billions in sales as early as 2023.

But most of the revenue will come from hardware and software infrastructure to create the networks or system integration. Revenue from managed services related to connectivity might be 10 percent of total revenues.

5G private networks might represent $7.5 billion in spending by enterprises in 2025, some estimate. Polaris estimates a 2027 market worth $8.3 billion by 2027.

Others estimate $16 billion in private network spending by that point. Sometimes analysts revise their projections upward virtually every year.

Mobile Experts estimated in 2019 spending at less than $3.5 billion by 2024. A year later the forecast was boosted to just shy of $10 billion. The early 2021 forecast showed figures were consistent with the 2020 estimate.

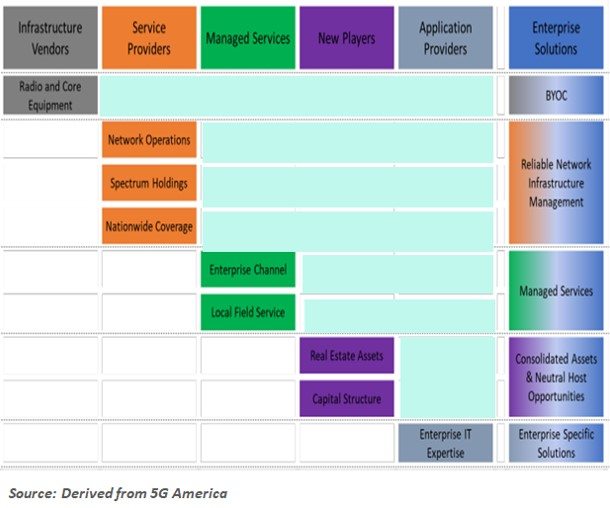

Beyond the issue of overall market size, there is a key matter of ecosystem and value chain roles. Some portion of the 5G private networks market consists of infrastructure purchased by enterprises to support their “do it yourself” private networks. The analogy is hardware and software purchased directly by end users to support their own Wi-Fi networking.

5G private networks will likely be a fragmented ecosystem, with equally fragmented revenue upside.

No comments:

Post a Comment