At least some mobile service providers hope subscription-based entertainment video will be a big deal, representing the latest evolution of entertainment video from movie theater to television, to cable TV (plus satellite and telco delivery) to Netflix and other over the top services, and then possibly to mobile consumption of OTT subscription video.

There are good reasons for believing that migration will happen. The shift from desktop to mobile happened in search, internet browsing, social networking and now video. Smartphones and other mobile devices are--or are becoming--the preferred devices for many of our day-to-day activities.

The most significant change in the status of competition in the market for the delivery of video services has been the introduction of Sling TV by Dish Network and DIrecTV Now by AT&T, the U.S. Federal Communications Commission says.

Others might also note the importance of the AT&T acquisition of DirecTV, which vastly expanded the addressable universe of homes AT&T could reach from less than 21 percent to virtually 100 percent of U.S. homes.

One sign of the robustness of competition is that profit margins, which once were as high as 40 percent, had fallen to about 10 percent in 2015, and likely are a bit lower in early 2017.

The FCC says profit margins were 15 percent in 2014 and 20 percent in 2013. That might be unappetizing in one sense, but arguably is meaningful in a context where other legacy services, whatever their profit margins, do not contribute much revenue. Video services represent a huge percentage of potential access provider revenue, if margins are not so high.

By some estimates, internet access gross margins (at least for cable operators) might be as high as 60 percent, while voice services might have profit margins near 20 percent. Telco margins likely are not that robust.

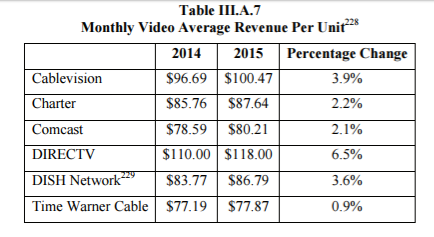

If cash flow matters--and it does--then the revenue video entertainment represents is hard to match, averaging between $80 and $110 a month, per account.

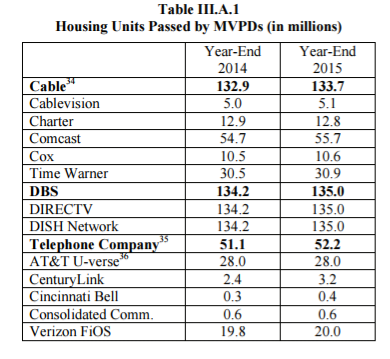

According to SNL Kagan, there were 134.2 million housing units in 2014 and 135 million housing units in 2015. The FCC therefore assumes that cable and satellite companies cover nearly every household in the country.

At the end of 2015, cable suppliers accounted for 53 percent of all subscribers, down from 53.4 percent at the end of 2014. Direct broadcast satellite (DBS) providers accounted for 33.2 percent of subscribers at the end of 2015, down slightly from 33.3 percent at the end of 2014.

Telephone companies accounted for 13.4 percent of MVPD subscribers at the end of 2015, up from 12.9 percent at the end of 2014.

Total subscribers declined in 2013, 2014 and 2015, with the suppliers losing about 1.1 million video subscribers in 2015.

But total video revenue increased from $112.7 billion in 2014 to $115.6 billion in 2015, partly because of rate increases and partly because of subscribers upgrading to higher levels of service.