No question is more logical for anyone in the mobile services industry than “what happens to revenue and sales after the pandemic is contained?” There likely is no single answer, as the likely result will be a reversion to whatever trends were already in place, by firm, market and industry segment.

In other words, after perhaps a year of mild mobile service provider disruption, firms, markets and industry segments will revert to whatever trend held before the pandemic. In some developed markets, for some firms, that means a continued revenue down trend.

In developing markets, growth will resume at about the same rates as before the pandemic. In other cases, slight growth will happen, as that was the pattern before the pandemic.

Fixed markets, facing disruption even before the pandemic, will likewise revert to form, but with a higher likelihood of revenue pressure in developed markets and slight growth in developing markets.

The answers also will hinge on whether the post-pandemic trend looks like the recovery from the internet bubble in 2001 or the recovery from the great recession of 2008, both for economies in general and telecom service providers specifically.

If the former holds, global revenue sort of plateaus for a year, then resumes an upward march. If the latter holds, then a prolonged period of lower revenue might happen. But there is a major caveat: what happens in developed markets and developing markets might well diverge.

Developing markets might make a relatively-swift rebound after a year. Some firms, but not all, in developed markets might see the same. On the other hand, many firms could see prolonged weakness.

“From 2007 to 2009, many European operators’ average revenue per user dipped by more than 15 percent, and churn rates rose by the same amount for operators in both North America and Europe,” say consultants at McKinsey.

More important is the recovery, though. And there we might see some divergence three years out. After the great recession of 2008, some firms by 2011 had recovered. Other firms a decade later had not ever returned to 2007 levels of growth.

Much depends on which markets we look at. Growth has been faster in developing regions, and likely will be different from patterns in mature developed markets. So we might well assume that the recovery pattern will differ in those markets.

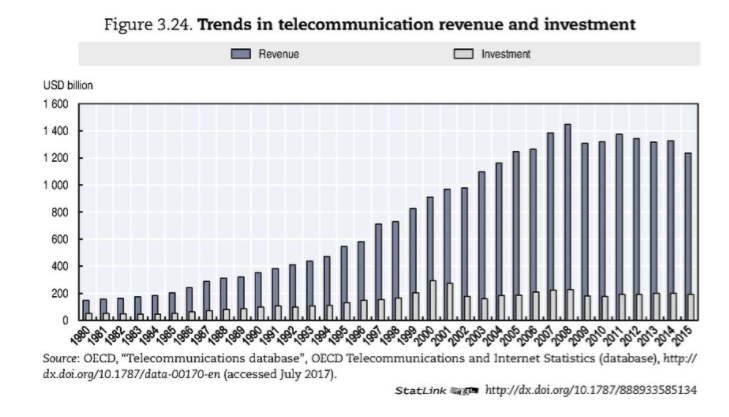

The Organization for Economic Cooperation and Development countries, on the other hand, saw only a one-year flattening of growth in the wake of the internet bubble in 2001, but saw sustained, multi-year drops in revenue after the great recession of 2008.

So it really matters whether we believe what follows the Covid pandemic resembles the recovery from 2001 or 2008.

In the U.S. market, for example, telecommunications revenue as a percentage of U.S. gross domestic product showed a brief slip in the wake of the collapse of the internet bubble in early 2001, but rebounded in a year. Keep in mind, this metric concerns “percent of GDP,” not absolute revenue figures.

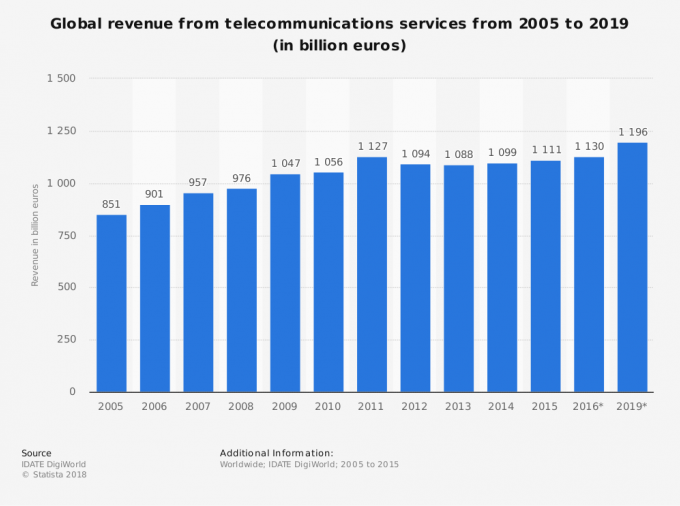

But some data suggests global revenue after 2008 was buoyed by growth in developing markets, even if developed markets did not recover.

The disturbing possibility is a global recovery that is slower than we saw in the wake of 2008, simply because the Covid response--shutting down national economies-- will cause a recession worse than 2008, as the International Monetary Fund now expects.

“It is now clear that we have entered a recession; as bad as or worse than in 2009,” said Kristalina Georgieva IMF managing director. “We do project recovery in 2021–in fact there may be a sizable rebound--but only if we succeed with containing the virus--everywhere-- and prevent liquidity problems from becoming a solvency issue.”

To be sure, the health of the economy is not directly linked to the health of the connectivity industry as a whole. There is evidence that communications spending was relatively unaffected in a negative way, and only for a short period, in the recovery from 2001.

In developed nations, though, revenue seems to have dropped since 2008. But that might be explained by other issues, not the direct impact of the great recession. New product substitutes, shrinking demand for virtually all legacy products, more competition and a fall of mobile and fixed data prices might explain revenue trends since 2008 in developed nations.

If that is the case, no matter how severe the 2020 recession might be, connectivity provider revenue trends might behave in ways that predate the recession itself.

That might include a relatively minor revenue hit in 2020, with a rapid recovery in 2021, with a stronger likelihood that happens in developing markets. Trends for many firms in developed markets have been negative since 2008, but for reasons largely unrelated to the recession itself.

The bottom line is that there is a good chance a modest revenue impact is followed by a reversion to whatever trends were in place before the Covid-induced recession.