One of the issues for connectivity providers trying to create new revenue streams--aside from a reputation for not being good at innovation--is the challenge of finding innovations that represent enough incremental revenue to justify the cost of developing them.

It is one thing to see projections of the new revenue from private 5G networks; something else to figure out how much of that opportunity realistically can be addressed by connectivity providers.

We face the same problem when trying to estimate the value of edge computing or internet of things markets as well. How much of that opportunity realistically could be converted into revenue for connectivity providers?

Since estimates of edge computing, unified communications, IoT and private 5G always involve a mix of infrastructure sold to create the networks; management solutions of some type; design, installation and operating support and some connectivity revenues, the issue is how to estimate realistic connectivity service provider roles and therefore revenues.

History suggests connectivity providers might have a role earning up to five percent of any of those proposed new areas of business, based on past experience with local area networks in general, or business services such as enterprise voice, conferencing and collaboration.

The global unified communications and collaboration market might have reached about $47.2 billion in 2020, IDC says. But most of that revenue was earned by entities other than connectivity providers.

For example, revenue booked by Microsoft, Cisco, Zoom, Avaya and RingCentral totaled about $26 billion for the year. Those five firms represent 55 percent of total UCC revenues for the year, IDC figures suggest.

Relatively little UCC market revenue is earned by connectivity service providers.

Direct connectivity provider revenue from local area networks is almost completely related to broadband access bandwidth sold to enterprises, smaller businesses and consumers. Almost all the rest of the revenue is earned by hardware and software suppliers, third party design, installation and maintenance firms, chip and device vendors.

The point is that the traditional demarcation point between cabled public networks and private networks--wide area and local networks--happens at the side of a building or in the basement. WAN and connectivity service providers make their revenue.

The demarcation point between mobile customers and the public networks is the device. The capacity services supplier owns everything from spectrum to tower, then tower to switches and other controllers, then the core network. The consumer owns the phone.

Traditionally, the “private network” has been the province of different firms than public networks, which is why interconnect firms and system integrators or LAN specialists exist.

Even in some “core” WAN areas--including virtual private networks--third party specialists and infrastructure suppliers dominate the revenue production. Software-defined WANs, for example, can be created at the edge using gear owned by the enterprises who set up the SD-WANs.

SD-WANs can also be created by managed services firms, which includes connectivity providers. But most of the revenue is earned by infrastructure suppliers or managed services specialists, not connectivity providers.

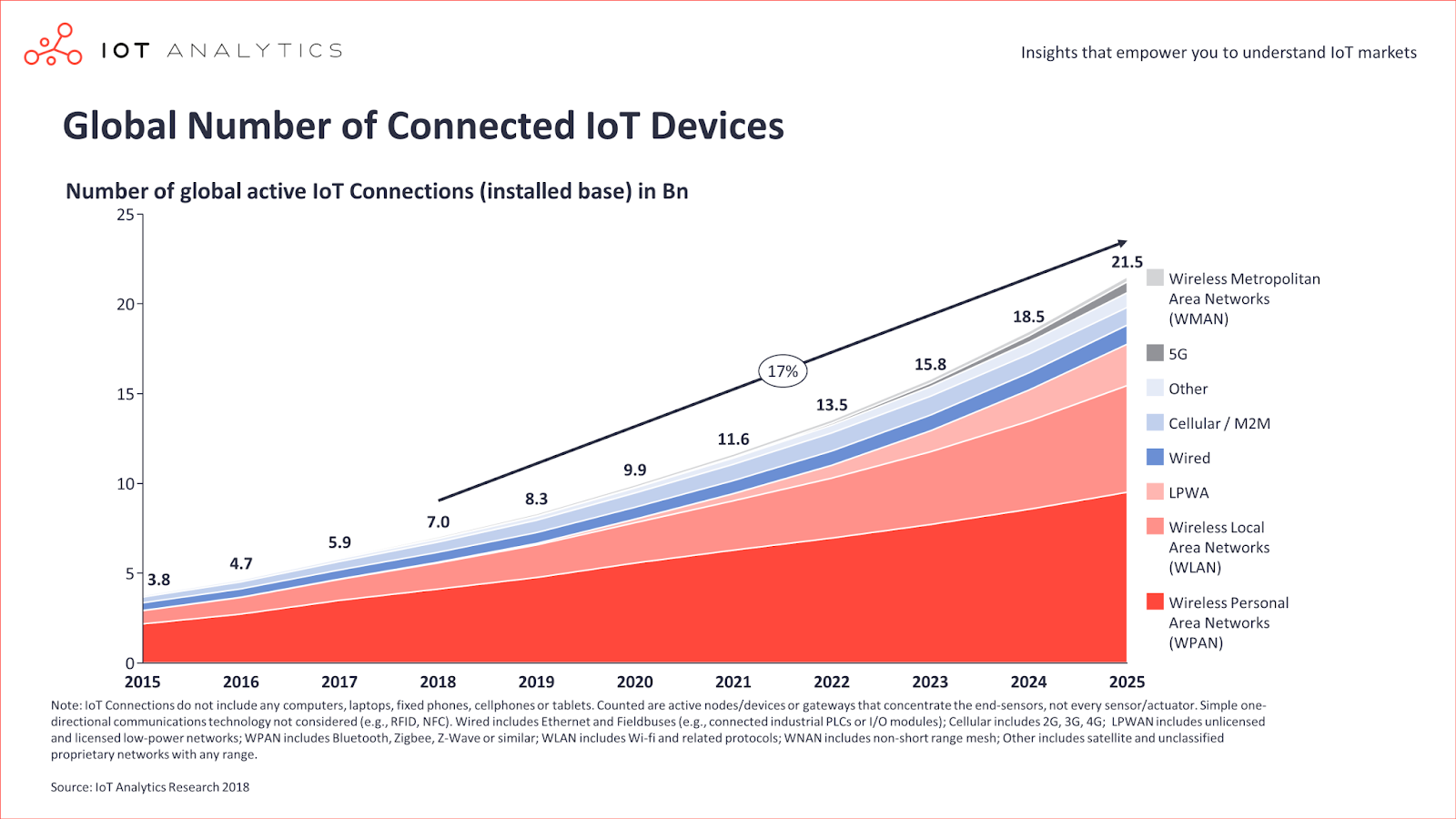

Much the same can be said for internet of things revenue upside. Most of the revenue will be earned by LAN hardware and software suppliers, sensor and devices suppliers and app providers. WAN connectivity will be a contest between specialized WAN providers using unlicensed spectrum and mobile operators using licensed spectrum.

But all WAN connectivity collectively will be a small part of the IoT revenue opportunity.

source: IoT Analytics

In edge computing, most of the actual “computing” will be done by hyperscalers and others, even when mobile and fixed network operators supply real estate or access connections. It already seems clear that most telcos are not going to try and challenge hyperscalers for the actual “edge computing” function.

Private 5G is mostly going to create revenue for infrastructure sales (hardware and software), as private 5G or 4G are local area networks, like Wi-Fi. The enterprise or the consumer “owns” that network.

All of which raises an interesting question. “Everybody” seems to concur that businesses and enterprises will drive most of the incremental new revenue from 5G. What if that expectation is wrong? And it could be wrong, in the early days.

Consider private 5G or edge computing or IoT opportunities. How much enterprise or business revenue do you actually believe connectivity providers in any single country can generate, compared to any other initiative in consumer segments?

Consider fixed wireless, for example, in the U.S. market.

You can get a robust debate pretty quickly when asking “how important will 5G fixed wireless be?” in the consumer home broadband market. Will it matter?

Keep in mind that the fixed network home broadband market presently generates $195 billion worth of annual revenue. Comcast and Charter Communications alone book $150 billion annually from internet access services that largely are generated by home broadband customers.

Mobile service providers have close to zero--and in some cases actually zero--market share.

Taking just two percent means new revenues of perhaps $4 billion annually, within a couple of years. How long do you think it will take T-Mobile to earn that much money from IoT, edge computing or 5G private networks? T-Mobile’s effective answer is “too long,” as it is not pursuing those lines of businesses in an active sense.

T-Mobile is launching new initiatives for consumer home broadband and business mobility services, though.

And the growth path for T-Mobile is clear. Instead of supplying new customers, with new needs, with new products, T-Mobile in its home broadband push only has to take a few points of market share in an established market.

So it is possible that early incremental new revenue will be found by at least some mobile operators not in the sexy IoT, edge computing or private networks but in the less-sexy business of home broadband.

Not to mention profits. The cost of creating a $1 billion revenue stream in IoT, edge computing or private networks--within a few years--will be somewhat daunting. The cost of creating $4 billion in home broadband revenues in the same time frame might be a simpler matter of applying marketing effort.