A survey of mid-size, multi-site enterprises conducted by Netertes Research suggests a large number are seriously looking at replacing a Wi-Fi network with a 4G-based private network alternative. As you would expect, Wi-Fi predominates, with more than 86 percent of respondents using Wi-Fi. But many use private networks based on 4G, 3G, 2G or Zigbee.

Most organizations will keep their existing primary network, but six percent say they will add a new network based on a different technology. Perhaps a quarter plan to shift their primary wireless network to a new technology.

None plan to abandon private networking for carrier-provided options.

The leading option to replace an existing network or to be an added network is some

variation on 4G, including the new option of Citizens Broadband Radio Service. About 41 percent of those making a change say they will do so.

Of 302 study participants, many came from just four industries: manufacturing, 18.5 percent;

retail, 16.9 percent; healthcare and pharmaceuticals, 15.9 percent; and hospitality and tourism, 14.6 percent.

The remainder came from: education, 10.9 percent; financial services, 7.6 percent; energy and utilities,3.6 percent; warehousing and storage, 3 percent; logistics and transport, 3 percent; commercial real estate management, 2.6 percent; and other, 3.3 percent, Nemertes says.

Some 71.8 percent of respondents work for firms making $300M or less annually. About 82.8 percent have fewer than 20 locations. The remainder are split roughly evenly between mid-sized

companies (16.2 percent earning $300M to $1B annually, 5.4 percent having 21 to 50 locations) and large companies (12 percent earning more than $1B per year, 11.8 percent having more than 50 locations).

It is a truism of chaos theory and the behavior of complex systems that very small changes in initial conditions can lead to very-significant and unexpected long-term changes. And that is why nobody really can predict, with conviction, what new revenue models, business models, applications and use cases will develop in the 5G era, just as there was similar uncertainty in the 3G and 4G eras.

Some of us would argue there is a definite reason for that uncertainty. Where it is conceivable to make predictions in a simple system that does not change too much, such certainty is almost precluded in any complex system.

Telecom planners might have had a good grasp of the advantages of adopting signaling system 7. Very few, if any, foresaw the importance of text messaging that was a byproduct of SS7 adoption. And that was back in the days when telecom arguably was not a complex system.

Since the global telecom industry adopted internet protocol as its next generation network, instead of asynchronous transfer mode, connectivity has been incorporated into the internet ecosystem.

Though many will not recall, debates about the choice of next generation network (IP or ATM) were heated around the turn of the century. A decade later, IP had won. But that has proven to be much more than a platform or protocol choice. Instead, the industry business model was forever changed.

Formerly able to control all apps created for use on its network, telecom now is an open connectivity platform where application development is nearly completely open to third parties. And that means telecom cannot control the creation and development of applications and revenue streams that happen to use the network.

Obviously, that also means connectivity providers and the telecom industry have given up the ability to control the scale or pace of app development, or much of the value proposition connectivity networks represent. Nor has the industry been able to halt the creation and spread of rival apps that cannibalize core telecom services and apps.

And that, in a nutshell, is the reason futurists and industry executives have been generally unable to accurately predict the development of new use cases, applications and business models in the era of 3G and 4G, and will similarly find the same task difficult in the 5G era is that each of those network generations might be considered complex systems.

And one attribute of a complex system is that they are virtually impossible to model reliably, as chaos theory suggests.

A complex system is composed of many components which may interact with each other, and where small initial changes can have very-large, unexpected outcomes (the butterfly effect).

Examples of complex systems often are said to include Earth's global climate, organisms, the human brain, power grids, transportation or communication systems, social and economic organizations (cities).

An often-used example is an ecosystem. And it is reasonable to describe the entire connectivity business (fixed, mobile, satellite, other networks) as now existing as part of a larger internet ecosystem. And if a single complex system is intrinsically difficult to model, an ecosystem of complex systems arguably is impossible to model accurately over time.

In large part, uncertainty about 5G exists because all complex systems are inherently highly dynamic, where no single actor in the ecosystem can direct progress. Also, the connectivity business as a whole now is part of the internet ecosystem.

It is easy enough to point out the differences between the connectivity function and the applications and services that take advantage of internet connectivity. But even those important distinctions do not fully capture the differences.

Ever since the global telecom industry decided that internet protocol was the next-generation network, the industry has had to adapt to a business ecosystem where the creation of services and apps can easily be conducted by third parties with no business relationship with any connectivity provider.

And that changes everything. Yesterday, telecom was a complex system of its own. Today, the whole connectivity function is part of the broader internet ecosystem. The fundamental change is that connectivity providers no longer control the scale or pace of business development of the whole ecosystem.

Where today the assumption is that system conflicts must be resolved and resolved centrally and uniformly, a complex system actually requires decentralized control.

Where a complex system inherently features conflicting, unknowable, and diverse requirements, today’s assumption is that requirements can be known in advance, and will change slowly. That leads to the assumption that tradeoff decisions will be stable.

But complex systems have inherently unknowable behaviors.

Where today’s notion is that system improvements can be, and are, introduced at discrete intervals, complex systems evolve continuously. Where it once was believed that the telecom industry could make changes where the effects could be predicted sufficiently well, complex systems do not support such certainty.

Where it was believed that the configuration information for any specific change was accurate and could be tightly controlled, a complex system actually means changes happen in an inconsistent environment.

All of that explains why nobody really can predict what will develop in the 5G and subsequent eras of mobility.

Consumer internet access plans in the fixed and mobile network domains have not changed much over the last couple of decades. Fixed network services are differentiated by speed; mobile plans differ by data allowances.

But one of the potential benefits of 5G, with its virtualized core and ability to support network slicing--creating virtual private networks that could support speed tiers--is a chance to revamp the way mobile data gets sold, in ways that arguably make it easier to sell value.

One clear example is a shift in mobile data pricing from “amount you can use” to “how fast do you want it?” That would allow mobile service providers to create tiered pricing plans that are based on “speed” rather than “data allowance.” The notion is that consumers more easily can see the value of “faster or slower” compared to “more or less.”

The former approach arguably creates products that are differentiated in distinct qualitative ways, instead of varying only by volume. The difference is that different speed plans are akin to three types of squash, where volume-of-consumption plans are similar to one type of squash, sold in one pound, 10 pound or 50 pound sacks.

The argument is that such tiered-speed plans can be combined with usage allowances, no-contract or contract plans, contract length or perhaps type of device that offer consumers the ability to tailor their plans to consumption in a more personalized way.

Heavy users who want the fastest speeds, lowest latency or perhaps even assured performance would be able to buy such plans, even if the quality of service plans might sell at business customer prices.

Other subscribers will be able to pay less for moderate usage, moderate speeds and best effort service levels. All that allows both for product differentiation, higher average revenue per account and hopefully more customer satisfaction as well.

So far, no U.S. mobile operators have tried this approach to retail packaging. Also, as all the four major providers now offer flat rate, unlimited usage plans, it is not possible to scale retail prices with usage. Adding speed tiers might also allow a chance to partially tie usage to retail price.

History suggests we might well be wrong about what new use cases will develop in the 5G era, as much of what operators expected for 3G and 4G similarly failed to develop as expected. Mobile operators expected that video calling and movie downloading would be big killer apps for 3G. That did not happen until 4G, but even then, streaming replaced downloading as the use mode for entertainment video.

In fact, some would argue the killer app for 3G was mobile access to email (remember BlackBerry). Others imagined 3G mobile phones would coordinate with traffic cameras to suggest the best routes for drivers to take, while 3G camera phones allowed photos to be sent websites. Music and video streaming were other potential killer apps that became widespread realities in the 4G era, however, not in the 3G era.

As 4G was becoming a reality, some argued 4G killer apps might include live mobile video, mobile gaming, cloud-based apps, navigation with augmented reality or telemedicine might develop as killer apps. Several of those predictions arguably proved correct, especially the usefulness of cloud apps of all sorts.

Apps expected for 3G actually appeared in 4G, it is safe to say. And virtually nobody seems to have anticipated apps such as Uber. Researchers at Nokia Bell Labs broadly identify eras of value enabled by mobility.

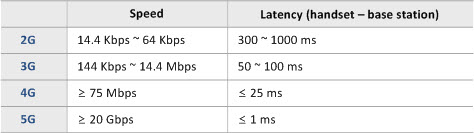

As it turned out, 3G was not adequate to support many of the applications developers had hoped to be able to create and commercialize. Speed was the most-glaring deficiency, but some argue security and latency also were issues 4G could address.

Early arguments for 4G actually sound similar to the argument for 5G in one respect: speed. On 3G networks, web browsing and video were painful experiences, which is why offload to Wi-Fi became so common. source: IEEE

“Everything” except voice, texting and picture taking would happen faster, it was said. That also is among the primary reasons 5G is touted as well.

That is not the same as arguing 5G does not offer experience advantages, for some applications and use cases, merely that initial coverage will be spotty. Also, there are different justifications for consumer users than for network suppliers.

The ability to support advanced applications, device density and lower cost per bit are advantages for network operators. The 4G network does not have the ability to support dense networks of sensors, for example, ultra-low latency or ultra-high bandwidth apps. As a practical matter, even when those attributes are not important for many use cases, the cost of supplying mobile data is a real issue, as consumers keep demanding use of more data, but are unwilling to pay substantially more.

Lower cost per bit is especially important for mobile service providers, given the expected growth of usage. Looked at only from the perspective of the network platform, mobile operators will have to supply ever-more bandwidth to consumers with relatively-fixed ability to pay. source: Keith Malinson

There are other network platform advantages. The 4G network was not inherently designed to be virtualized; the 5G network core will do so, with important potential savings in capital investment and operating cost. In principle, 5G will allow--based on growing support of open source approaches--a mix and match strategy for radio access networks. That will increase competition, and therefore lead to lower costs for RAN investments.

The larger point might be that many proposed exotic and new applications envisioned for 5G might not flourish and become commonplace until 6G. That broadly has been the case for 3G and 4G. Some proposed 3G apps did not become widely possible until 4G. Some proposed 4G use cases might not become routine until 5G is firmly in place. And the exotic 5G apps will often become commonplace only in 6G or later.

It is not an easy matter to predict whether 5G will produce higher average revenue per account in the U.S. market. For starters, not all the leading service providers will charge a price premium for 5G. T-Mobile US continues to say it will not charge any price premium for 5G. AT&T has not yet unveiled consumer 5G pricing.

And Verizon and Sprint both charge a $10-a-month premium for 5G access, as part of their unlimited plans, including all Verizon unlimited data usage plans and Sprint’s top unlimited usage plan.

Though T-Mobile US says it will not charge a price premium for customers of its 5G network, both Verizon and Sprint are charging $10 a month more for 5G, on the top-end unlimited plans, in Sprint’s case, or on any unlimited data usage plan in Verizon’s case. That means there is some potential for revenue increases on 5G plans, for Sprint and Verizon, to the extent that consumers choose to buy unlimited-usage plans.

Sprint’s 5G service is reserved only for its $80-per-month "unlimited premium" customers. The 5G network will not be available for use to Sprint customers buying $70-a-month or $60-a-month unlimited plans.

Access to Verizon’s 5G Ultra Wideband network is $10 per month with any of Verizon’s unlimited usage plans.

Virtually all observers expect 5G data consumption will increase, at least on the part of early adopters. Sprint CTO John Saw said 5G customers are consuming three to five times more data than its 4G LTE customers.

Several likely reasons: early adopters tend to be heavier users and faster networks mean users consume more data in equal amounts of time.

In South Korea, average customer data usage on 5G was 24 gigabytes in June 2019, which was 2.6 times higher than the 4G average of 9.1GB.

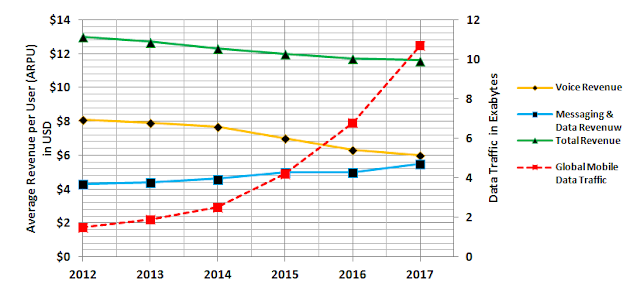

If 5G follows the pattern of 4G, there will initially be a period where 5G ARPU is higher than 4G ARPU, at least for some service providers. But 5G is launching in a context of declining ARPU for the leading mobile operators in the U.S. market.

Data ARPU, on the other hand, might be increasing, in part because users are buying plans with larger usage allowances.

That trend has been underway for some time, as noted by Teleanalytics.

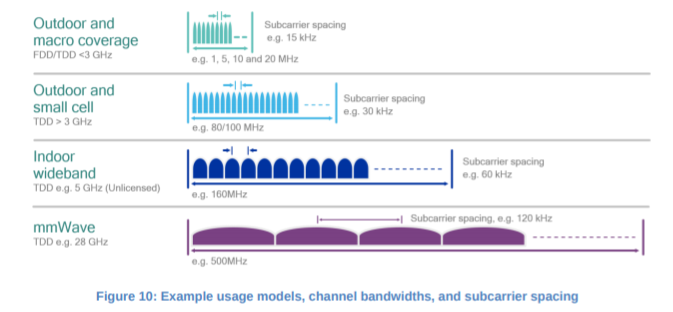

One key argument for 5G is that it supports vastly more bandwidth than does 4G. In fact, the practical argument for 5G is that it allows mobile operators to supply capacity at lower cost per bit, a necessary requirement to maintain profit margins as mobile operators must supply ever-greater consumption allowances at roughly fixed prices.

5G is, by design, capable of 10 to 20 times the downstream speeds of 4G. But it is not intuitive that 5G supports an order of magnitude more bandwidth than 4G. Could we not increase bandwidth just as much by allocating more spectrum for 4G?

In other words, since spectrum and capacity are directly related, why not simply run 4G in millimeter wave bands? The easy answer is that each next-generation mobile network takes advantage of improvements in coding efficiency and modulation complexity that were not possible in the older generation network.

In principle, even if 4G were simply extended to new bands, the new network would forfeit the 10-fold to 100-fold advantages in bandwidth efficiency and latency reduction. New networks also are designed to use wider channels, which additionally increases bandwidth within each channel.

Another answer is that 5G uses much-wider channels than older mobile generations. Long Term Evolution (4G) supports channels up to 20 MHz. 5G NR, on the other hand, supports channels featuring many hundreds of MegaHertz. As with all communication systems, wider channels mean more potential bandwidth.

Also, wider channels also mean less bandwidth “wasted” in the form of guard bands.

Ignore for the moment the practical reality that chipsets and radios are not designed to support 4G in millimeter wave frequencies. 5G networks, designed to support machine-to-machine communications, also incorporate the ability to support vastly-greater number of sessions and devices in each cell.

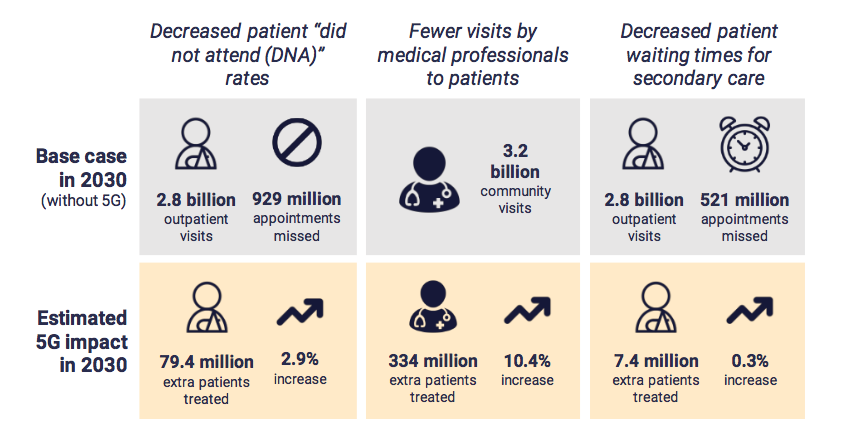

5G-enabled virtual health consultations could reduce patient ‘did not attend’ rates by nearly three percent in 2030, according to STL Partners. Furthermore, the time saved by medical professionals would enable increase their number of consultations by over 10 percent.

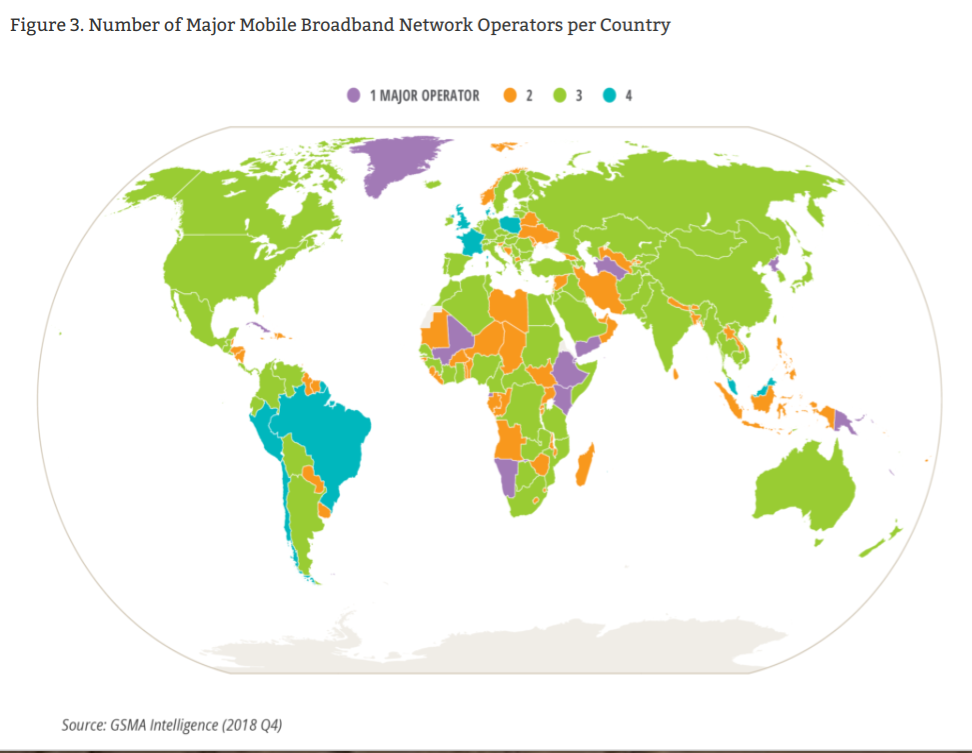

With some exceptions, the mobile service provider business tends to feature three leading providers in any single country. And that might be the best sustainable outcome, in at least some countries.

Though many would note that the existence of mobile virtual network operators will increase competition, it also is an industry fact of life that capital-intensive connectivity networks will always be relatively few in number. It is an oligopolistic industry because so few facilities-based firms can exist profitably.

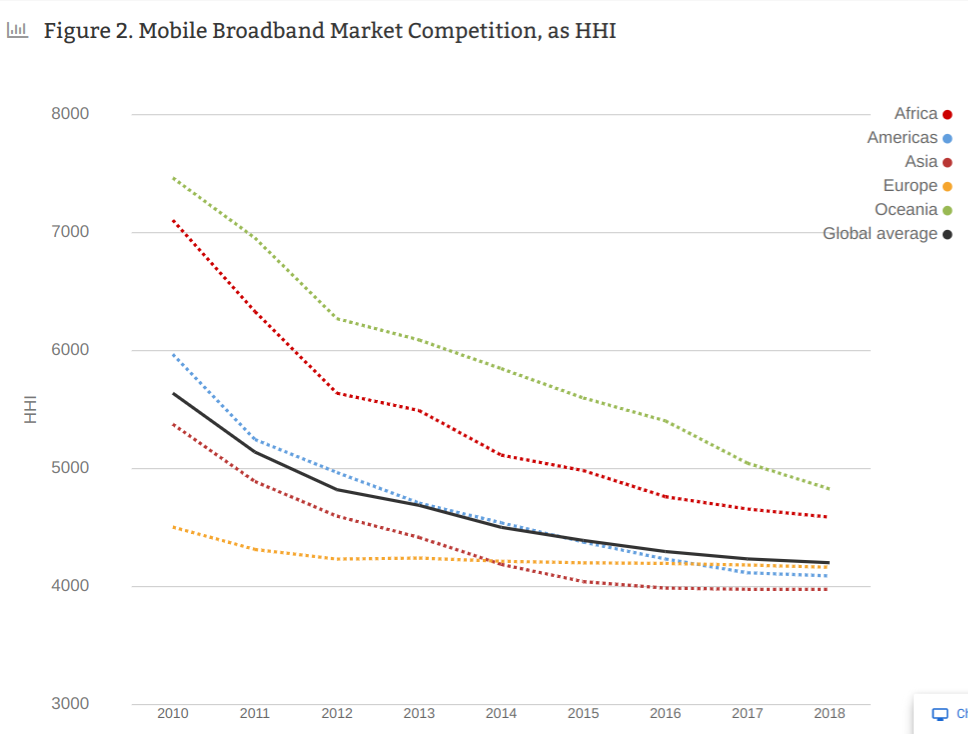

With the caveat that nationwide telecom systems always tend to be few in number, virtually every mobile market is highly concentrated, using the Herfindahl-Hirschman Index (HHI), a widely-used measure of market concentration.

A market with an HHI of less than 1,500 is considered to be a competitive marketplace, an HHI of 1,500 to 2,500 to be a moderately concentrated marketplace, and an HHI of 2,500 or greater to be a highly concentrated marketplace.

No mobile market actually can be deemed “competitive” using the HHI test. On the contrary, every mobile market is highly concentrated.

Some might argue that relative lack of competition explains the price of mobile data, which because of less than robust competition costs users an estimated $3.42 per gigabyte, according to the Alliance for Affordable Internet.

In cases where only a single facilities-based supplier operates, breaking up a broadband monopoly can create a savings of up to $7.33 per GB for users, the Alliance for Affordable Internet argues.

Across Africa, for example, a continent with generally less robust competition, the average cost for 1GB data is 7.12 percent of the average monthly salary. In some countries, 1GB costs as much as 20 percent of the average salary, says the Alliance.

If the average U.S. earner paid 7.12 percent of their income for access, 1GB data would cost $373 per month.

Average revenue per user or account is generally falling everywhere in the consumer segment of the connectivity business, including the key mobility business. Analysts at PricewaterhouseCoopers believe declining ARPU also is linked to commoditization of mobile service, though price declines might also be related to lack of competition.

To be sure, the notion that commoditization and differentiation are polar opposites, with higher profit margins for the latter, lower profit margins for the former, also might be confused with the degree of competition in each market, user preferences in each market or service provider strategies.

“Most markets in the region are on the edge of commoditization,” says PwC. “Only Indonesia, still dominated by a single player, remains considerably differentiated.” Analytically, it is difficult to separate commoditization from monopoly power, even if, conceptually, the concepts are distinct.

PwC consultants also have argued that two fundamental paths forward exist for connecitivyt providers: take an applications or networking role. As a rule, the former role is arguably best suited for leading tier-one service providers, the latter role perhaps best suited for the second or third market share holder in each market.

In large part, that is a function of the capital investments the shift to an app provider role entails. One might also question how successful most suppliers have been in their “move up the stack” efforts.

Indeed, with the shift of revenue growth to various connectivity products, ranging from software-defined wide area networks for enterprise customers to internet access for consumers, the revenue driver now is the “dumb pipe” internet access function.

Competition has not helped, in that regard, as price pressure has developed.

The whole point of cloud-native, virtualized networks is the ability to mix and match network elements with software, avoiding vendor lock-in and combining lower-cost commodity hardware with control software that can be separated from the network elements.

In the context of mobile networks, that should ultimately mean the ability to use any compliant radio access network with any core network. That is not yet possible, but is coming, with work on Open RAN and Telecom Infra Project, for example, supported by major tier-one service providers such as Telefonica and Docomo.

NTT Docomo, for example, has announced multi-vendor interoperability across a variety of 4G and 5G base station equipment compatible with the international standards of the Open Radio Access Network (O-RAN) Alliance, using gear fromFujitsu Limited, NEC Corporation and Nokia.

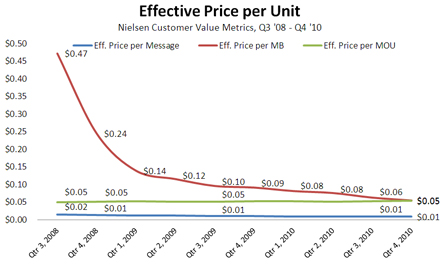

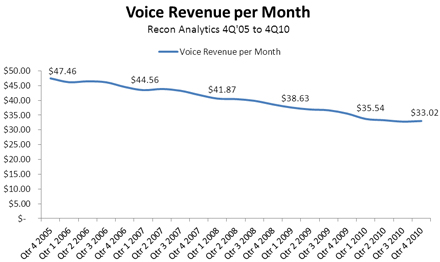

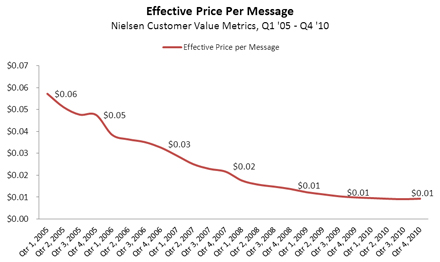

Whatever else 5G might represent, it probably will not increase mobile operator consumer account data revenues. Since 2005, nothing has done that. In the U.S. market, the availability of unlimited usage plans has not helped, in that regard.

It might also be fair to say that other mobile generations, from 2G to 4G, have boosted data revenues, but net revenue gains have been muted as voice and text messaging prices have plummeted.