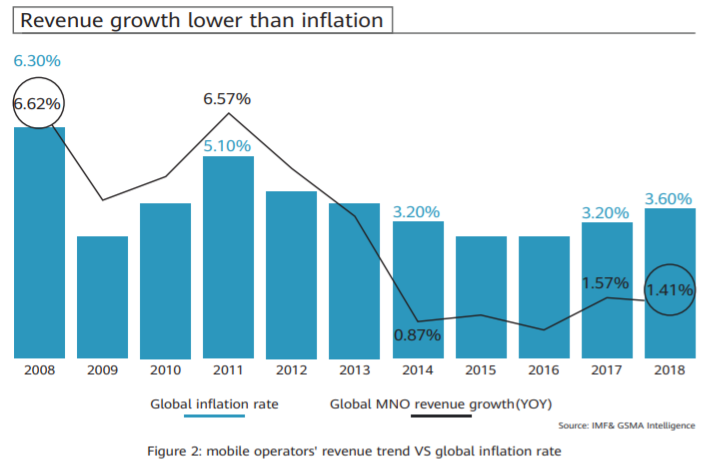

Mobile service provider revenue growth rates over the past decade have fallen from a range of six to seven percent to less than 1.5 percent, though rates are higher in some countries. That arguably is the single greatest issue mobile operators face, though not for the first time.

In the monopoly era, revenue was not much of an issue. Service providers earned a fixed rate of return on investments, there were no competitors and the profits from international long distance, domestic long distance and business customers produced enough profit to subsidize consumer consumption.

All that changed with deregulation and privatization beginning in the 1980s and gaining wider prevalence through the 1990s. Within about a decade, long distance voice had ceased to provide both the gross revenue and profit to support the rest of the business.

Competitors began to take market share, forcing a long wave of restructuring for most companies, designed on one hand to reduce costs, on the other hand to gain scale out of market to boost revenues.

So an early adaptation to a failing business model was expansion into new geographic areas or acquisition of competitors. Mobility, though, was unquestionably the major replacement for lost long distance revenues.

In later iterations, as subscriber growth saturated, we saw the emergence of text messaging and then mobile internet access as new revenue growth drivers. So the next huge challenge for a growing number of mobile operators is what replaces mobile internet access as the next big driver of revenue growth?

In one sense, 5G is not that driver. “High-speed 5G services will drive up mobile data traffic but with little-to-no uplift in average revenue per user average revenue per user,” says Martin Lund, Metaswitch CEO.

But many hold hope that 5G plus other key innovations, including edge computing and internet of things, might be big enough to sustain mobile revenue growth at the margin.

Long term, some would argue even that will not be sufficient to sustain firm viability. Basically, diversification into additional lines of business, up the stack or across the ecosystem, will also be necessary.

That is why many believe new non-connectivity revenues are so important. They reduce reliance on connectivity revenues, might produce higher profit margins but also importantly move connectivity providers out of that niche in the ecosystem.

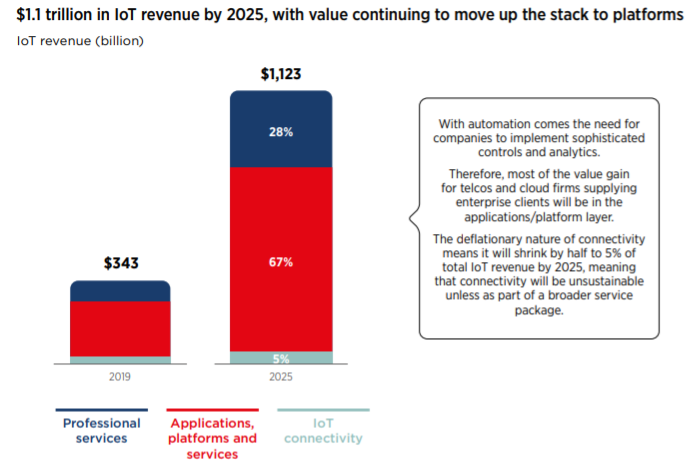

Looking only at internet of things, for example, GSMA Intelligence estimates that only about five percent of total IoT revenues will be garnered by suppliers of connectivity. That might prove to be a significant revenue source, to be sure. But it does not capture much of the upside of IoT, which will be in applications, platforms and services.

To reap a bigger harvest, connectivity providers will have to consider moving into apps, platforms and services, as difficult as that might be.

No comments:

Post a Comment