Estimates of annual global telecom service provider revenue vary by about $300 billion to $400 billion, from a low of about $1.4 trillion to a high of about $1.8 billion. For most people, that only matters because the anticipated boost to service provider revenues from new products such as multi-access edge computing, internet of things or private networks is likely to be one percent for any specific new product and smaller than 10 percent of the difference in overall market size in aggregate.

In life and in nature, a Pareto rule tends to hold. Up to 80 percent of variances in outcomes are attributable to perhaps 20 percent of actions. For mobile operators, that means consumer and business phone connections, despite the obvious promise of new services.

The likely exception will be 5G fixed wireless. Revenues from that new product will dwarf IoT, private networks and edge computing. 5G fixed wireless might, in some markets, represent as much as eight percent of home broadband revenuesfor example.

Under normal circumstances, global service provider revenue grows by at a slow rate. Growth in the 1.5 percent range or less is the present status for the industry overall, though some markets and some companies see higher growth than the average.

The point is that organic revenue growth can be as low as $20 billion to $30 billion in a typical year. So any new product that generates $20 billion to $30 billion in industry new revenue in any given year is a big deal.

It is almost certain that global service provider revenues from multi-access edge computing, for example, will be in the single-digit billions ($ billion) range over the next few years. The same is true of forecasts of service provider internet of things revenue. The service provider 4G or 5G private networks revenue stream is likely to be small as well.

The point is that new revenue sources such as edge computing, IoT and private networks are unlikely to move the global service provider revenue needle over the next several years, and perhaps not for a decade.

Those revenues might be more important in a handful of markets, however, such as large countries that are early adopters. Even there, however, the large installed base of revenue means the incremental growth from the new services will make a generally slight contribution.

In some part, the growth challenge is the result of the size of the installed base itself.

When including the value of subscription TV services, the global telecom services market (mobile plus fixed) amounts to about $1.8 trillion in annual revenues, according to Precedence Research. The firm uses a cumulative annual growth rate of 4.85 percent from 2022 to 2030, a figure most observers would likely agree is too optimistic.

Grand View Research estimates revenue in about the same range. But others, such as Analysys Mason, tally global revenue at a lower level. closer to $1.4 trillion.

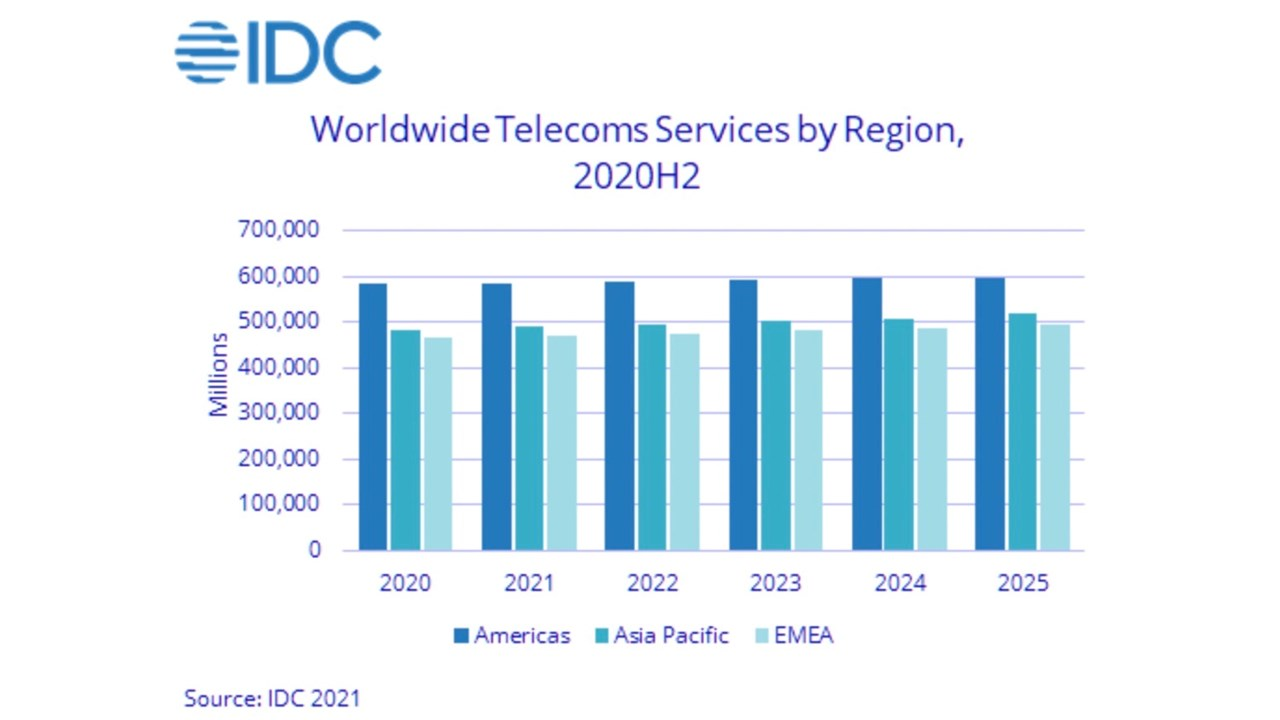

IDC forecasts are close to those of Analysys Mason, with 2021 revenue in the $1.5 trillion range.

As a rule, I have found the more-conservative figures are closer to reality.

No comments:

Post a Comment