Most of us are familiar with the 80/20 rule, which suggests that roughly 80 percent of value or outcomes are generated by about 20 percent of actions. Formally, it is the Pareto theorem.

Pareto applies to most aspects of the connectivity, data center or computing businesses. It even applies to revenue generated by mobile cell sites. Half of mobile revenue is driven from traffic on about 10 percent of sites. Fully 80 percent of revenue is driven by activity on just 30 percent of cell sites.

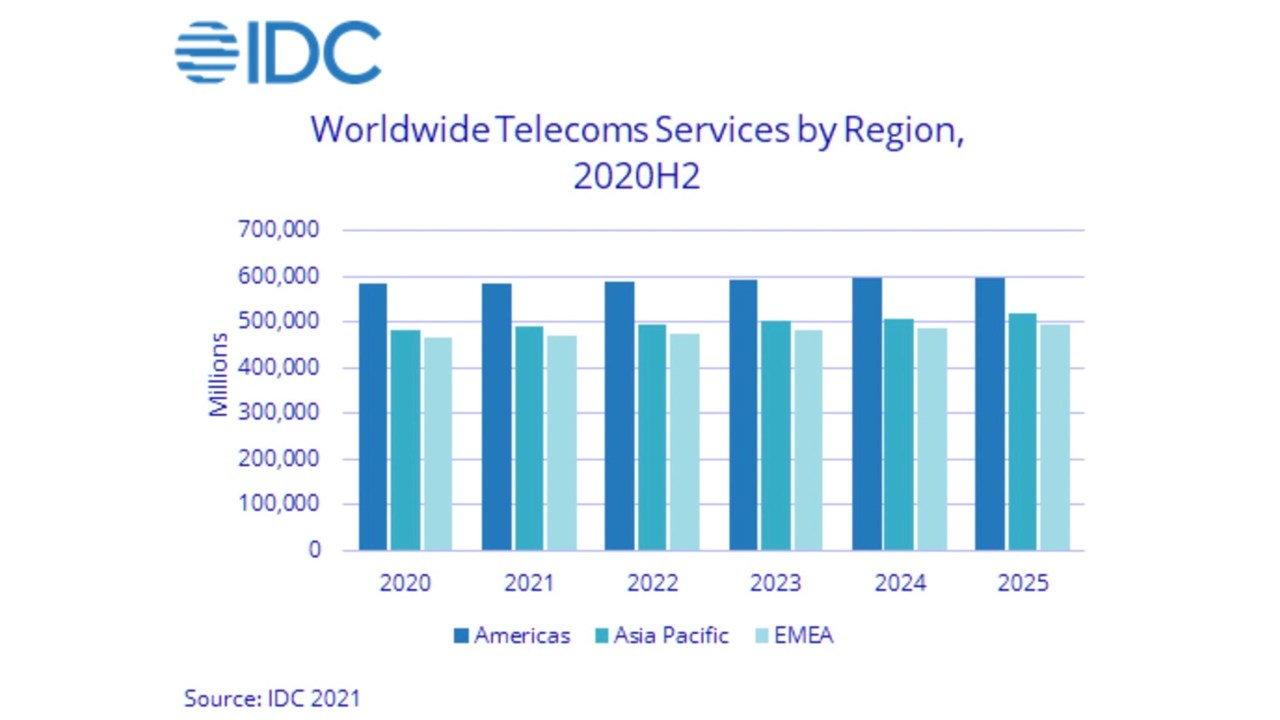

Beyond cell site revenue generation, mobiltiy has been altering global telecom revenue patterns for decades. And while a classic Pareto distribution has not yet been reached, we seem to be moving closer. Fixed network revenue continies to grow, but not as fast as mobile revenue increases. On the cost side, heavier fixed network capex is driving less growth, compared to lighter capex for mobile and faster revenue growth.

Over the next 10 years, we might see a closer fit between Pareto theorem suggests and what global telecom revenue shows.

Pareto also seems to apply broadly to global connectivity provider revenue and profits as well. Annual global connectivity provider revenue has been estimated at about $1.5 trillion for 2021 and 2022 (including video entertainment subscriptions).

But as much as $820 billion to $1.1 trillion in revenue is earned from mobile services. Being conservative, assume mobile revenue globally is $820 billion, while total revenue is $1.5 trillion. That implies mobile represents 55 percent of total revenue.

At the same time, one can note that fixed network data revenues were about $400 billiion in 2020, while voice contributed about $170 billion, for a total of about $570 billion, or 38 percent of total revenue.

Globally, most people using the internet do so using the mobile network. Most people in developed regions have access to both fixed and mobile modes. The percentage of people using fixed internet access alone is almost too small to measure.

The “mobile-only” pattern of internet access has been in place for close to a decade, as mobile internet usage began to spike upwards since 2010, to the point that half of all the world’s people were using mobile internet by the end of 2019, according to GSMA figures.

The shift of subscriptions from fixed to mobile happened about 2002.

At the same time, one can note that fixed network data revenues were about $400 billiion in 2020, while voice contributed about $170 billion, for a total of about $570 billion.

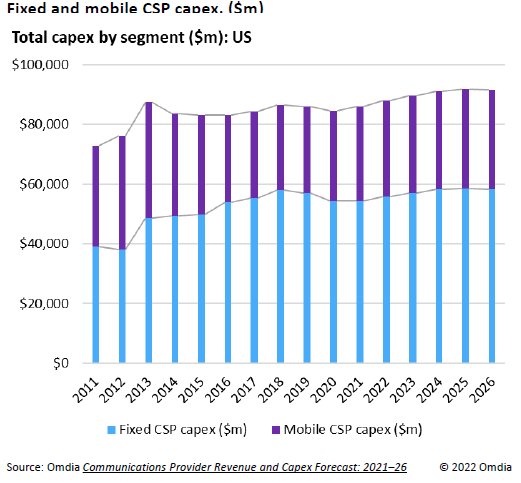

On the other hand, capital investment for the fixed network was about 68 percent of total in 2021. So you see the pattern: nearly 70 percent of capex to generate 38 percent of revenue. Conversely, 30 percent of capex spent on the mobile networks generates 55 percent of total revenue.

Though not an idealized Pareto distribution, the distribution of revenues and capital investment is beginning to approach the Pareto distribution. .

No comments:

Post a Comment