The U.S. cable industry has fared relatively better in the competition with telcos for at least some logical reasons, aside from arguable industry culture advantages. In the competition for fixed network voice and mobile services, cable has been the attacker, starting with zero market share and winning accounts from the incumbents.

In the following chart, cable TV mobile accounts are shown in purple. T-Mobile share is shown in green; AT&T account share in gray; Verizon share in blue. Virtually nobody expects cable account share to do anything but grow.

In home broadband, cable has benefitted from the relative slowness of telco adoption of fiber-to-home platforms. Simply, cable has leveraged its lower-cost hybrid fiber coax platform to radically boost performance at much-lower cost than telcos have been able to do.

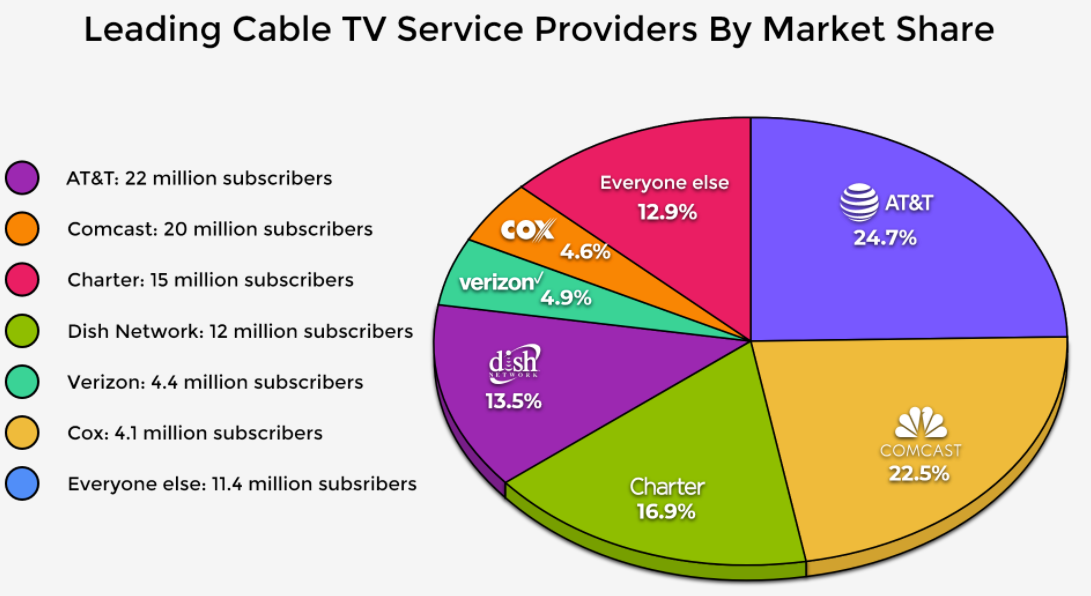

In video services, where cable was the incumbent, there was a slow attrition of some market share to telcos. The big share held by non-cable providers was in the hands of the satellite providers, and AT&T at one point owned all of DirecTV, immediately making AT&T one of the largest providers of linear video subscriptions in the U.S. market.

That stake in DirecTV has been spun out to private equity group TPG, but AT&T retains a 70-percent interest in the venture.

Still, terrestrial fixed network market share held by telcos was relatively small.

In recent decades, competition between telcos and cable has shifted. Video share has remained relatively constant, with the overall market gradually shrinking. The fixed network voice market is declining, for all leading providers.

Home broadband has emerged as the revenue growth driver. And while cable has held close to 70 percent of the installed base in that market, many observers--perhaps most--now expect telcos to take more share as FTTH becomes more common.

Nationally, telcos have about 30 percent share of the home broadband installed base. The issue is how much additional share telcos can gain as they ramp up FTTH platforms and as 5G fixed wireless becomes a factor for Verizon and T-Mobile.

All that likely means that mobility will become the new growth battlefield between cable and telco.

No comments:

Post a Comment