It is not always so obvious why new services such as AT&T Watch, a $15-a-month streaming service, is so fundamental for mobile operators and retail- and consumer-focused telecom service providers.

The fundamental problem is that the core business model--connectivity services--is incapable of driving future revenue growth. In fact, we are likely to see an actual erosion of such revenue in developed and developing markets, sometime within the next five to 10 years.

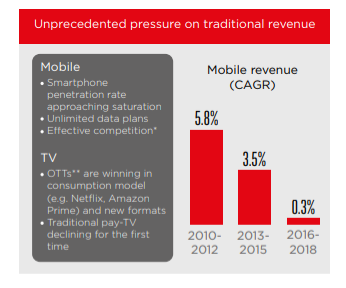

Already, mobile revenue growth in the U.S. market, for example, has dropped from nearly six percent in the 2020 to 2012 period to just 0.3 percent at present, according to GSMA.

Developing markets have a bit more time to respond. Since 2008, service provider revenue growth rates in developing markets dropped from 15 percent to three percent percent this year, while developed market growth dropped from four percent to zero, according to GSMA.

So movement into new value-generating lines of business--beyond connectivity--is essential, to replace lost core revenues. In the consumer services space, video entertainment has been the latest new service to offset declining voice and messaging revenues, and slowing internet access account growth in developed markets.

In developing markets, subscription growth has slowed, but not abated, and mobile internet access growth is nascent and growing. Still, eventually subscription growth will stop, and adoption of mobile internet will saturate. That is how product life cycles work.

Global telecom revenue in the 60 biggest markets will fall by two percent in U.S. dollar terms, to $1.2 trillion, in 2018, according to the Economist Intelligence Unit.

In developed markets, subscription growth has shifted from consumer access for phones, tablets and PCs to growth lead by internet of things devices and sensors.

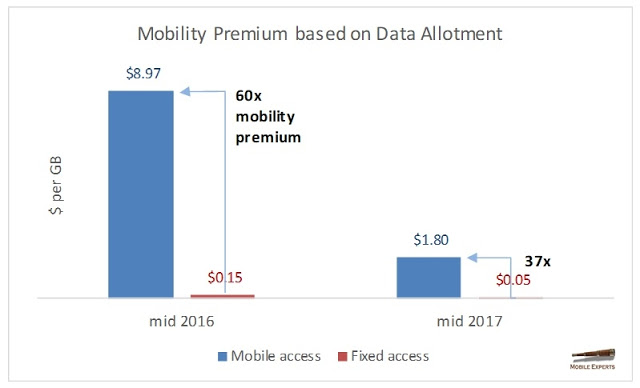

But one of the few growth areas for consumer services is mobile substitution for internet access. The coming 5G network will be foundational in that respect.

Using 5G, cost per gigabyte will fall 100 times, according to Mobile Experts. That drop in per-gigabyte pricing is essential if mobile alternatives are to be price competitive with fixed internet access services, allowing mobility suppliers to cannibalize the fixed network business.

There are other issues, such as the growing share of internet ecosystem revenues being claimed by device suppliers, content suppliers, app providers and platforms.

Since 2010, service provider share of industry profits has dropped from 58 percent to 45 percent, as every other segment has grown its share of profits, according to the World Economic Forum.

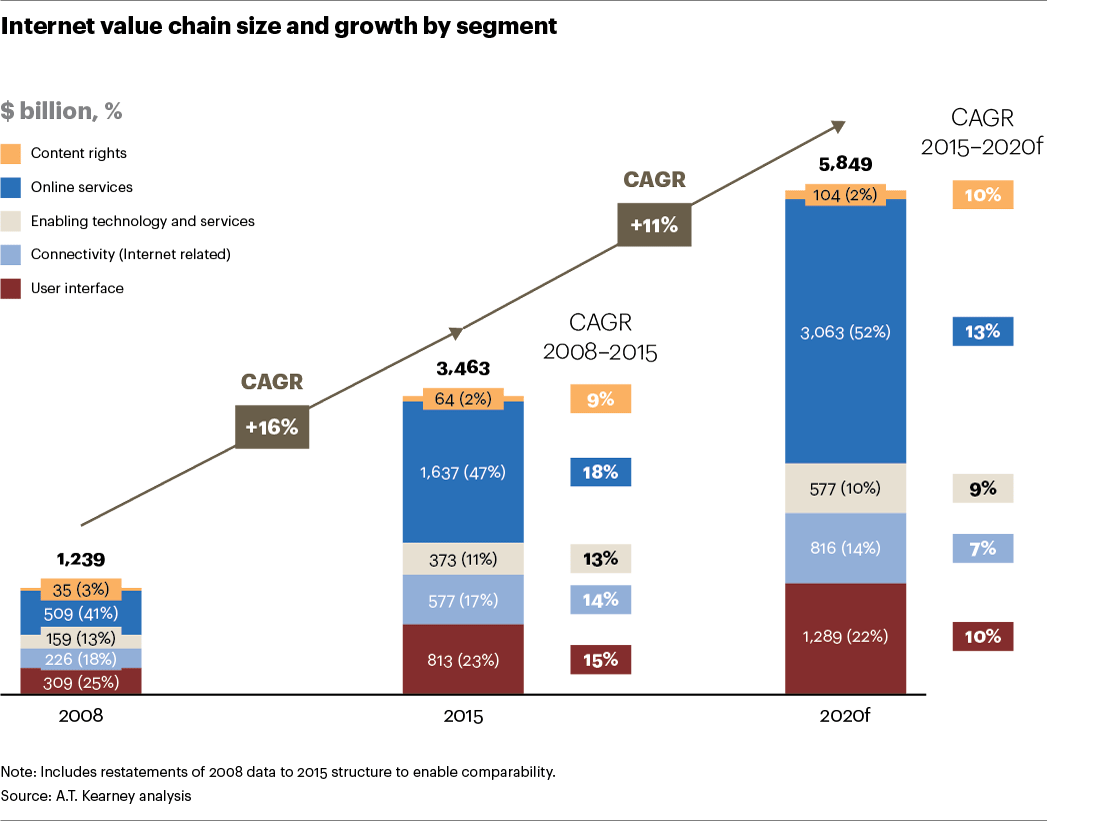

In 2008, internet access revenue was 18 percent of ecosystem revenue, dropping to 14 percent in 2015 and headed to seven percent by 2020, according to A.T. Kearney.

Overall, it can be noted that applications, content, devices and platforms represent 97 percent of the value and revenue in the internet ecosystem. By definition, these are the ways value and revenue is created beyond pipes.

And that is why connectivity services providers are compelled to seek growth in apps and platform areas. And that is why services such as AT&T Watch matter.

It is the model for future growth in additional areas, including internet of things, augmented reality, virtual reality, enterprise apps, connected vehicles and smart cities.

No comments:

Post a Comment