The number of potential rural internet access platforms keeps growing.

Altaeros, for example, sells a blimp-based "SuperTower" for mobile coverage. Altaeros partnered with Ericsson to deploy a multi-sector 4G Long Term Evolution base station in rural Maine.

SuperTower blimps float at heights six to eight times higher than most cell towers, cost up to 70 percent less than macrocells and provide coverage equivalent to a network of 30 conventional cell towers, Athaeros says.

Altaeros was founded at MIT in 2010 and has raised funding from SoftBank Group Corp. ($14.5 million), Mitsubishi Heavy Industries, the Suhail Bahwan Group and Ratan N. Tata.

Google Loon, Facebook Aquila and several proposed constellations of low earth orbit satellites also are conceivable ways to provide lower-cost internet access in rural and thinly-populated areas.

The actual size of the rural untethered access opportunity can vary wildly based on one’s assumptions.

Estimates of rural need vary. Some 23 million people in rural areas of the United States are said to have no access to a fixed network, though nearly all have satellite access from at least two providers.

From a service perspective, “locations” matter more than “people at those locations,” since facilities have to be build to reach fixed locations such as houses. In 2016, by one estimate, some six percent of U.S. homes purchased a satellite internet connection.

If there are roughly 126 million U.S. homes, that implies 7.5 million U.S. satellite internet customers. That clearly is wrong. Even the satellite providers do not claim to serve that many customers. A reasonable estimate of U.S. satellite internet customers is about two million.

By other estimates, 14 million locations have slow service from cable or telcos or are not served at all. Few of those locations actually have no fixed network service. On surveys availability, about one percent of respondents say they do not have the ability to buy internet access services.

That implies, on a household base of 126 million, that about 1.3 million locations actually have zero fixed network access. Keep in mind that the two U.S. satellite internet providers claim nearly two million customers (some of which are businesses, not residences).

The point is that market sizing estimates that postulate 23 million or more “unserved” people actually represent a rather small percentage of locations, and it is locations that must be served (mobile actually serves “people”).

Also, one problem is definitional. Some studies people who choose not to buy or people who do not wish to use the internet as “not able to buy internet access.” There is a difference between people who choose not to buy a product that is available and people who want to buy, but cannot.

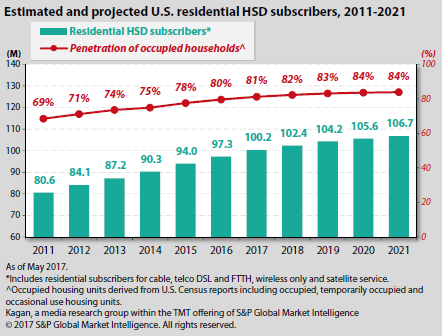

U.S. internet access adoption is about 82 percent. If there are 126 million U.S. households, perhaps 95 percent of which are occupied, then 100-percent adoption would imply about 120 million locations buying internet access. That might imply a reasonable saturation level of demand at about 107 million households, or nearly the level that might be reached in 2021.

In other words, 107 million households might be the saturation level for fixed network platforms (untethered options include mobile, fixed wireless, satellite, balloons, unmanned aerial vehicles, blimps).

Of course, demand does not exist at that level. Some households (perhaps five to 10 percent simply do not wish to buy). And some percentage of households (growing in number) buy alternatives such as mobile internet access.

It is reasonable to suggest that, in addition to sheer availability, there is a “lack of speed” problem is more substantial. So the market potential for new platforms includes both locations that have zero fixed network access plus locations where access is available, but “slow.”

That probably means an order of magnitude greater market potential than the number of fixed network unserved locations.

The broad point is that rural internet access problems (no service or slow service) are as likely to be fixed by untethered solutions (mobile, fixed wireless, satellite, balloon, unmanned aerial vehicle or blimp) as any fixed solution, especially as the business model for fixed service continues to deteriorate.

No comments:

Post a Comment