With the news that Sprint and T-Mobile US are once again talking about a merger, it is worthwhile to note that big mergers of almost any sort have a high failure rate, or fail to deliver promised strategic advantages.

According to one study by KPMG, perhaps 83 percent of studies U.S. mergers actually failed, in terms of increasing equity value of the new entities.

About 32 percent of merged firms showed equity value increase, while almost 70 percent actually reduced shareholder worth or, at best, were neutral.

Perhaps tellingly, the amount of increase--where it happened--is arguably less than if the firms had not merged, KPMG found.

Of course, that gamble obviously gets taken frequently, in the telecom and other markets. Sometimes “being early” is as bad as “being too late.” Recall that back in 1998, AT&T, then a long-distance voice provider, acquired the largest U.S. cable TV provider, Tele-Communications Inc., in a $48 billion deal.

The logic was simple. AT&T owned no local access networks, and needed such assets to compete with the former Regional Bell Operating Companies, which provided local access, but were moving into the long distance and other new lines of business.

As crazy as it might seem in retrospect, the big prize was viewed as the ability to use TCI’s cable TV assets to provide local phone service, not the ability to enter the video entertainment business. The internet access business was yet nascent, and while viewed as an advantage, it was the local phone revenue streams that drove the transaction logic.

Nor was that the first such proposed deal. In 1993, RBOC Bell Atlantic Corp. also tried to buy TCI for $16.7 billion, less to support its long distance voice operations but to gain leverage in the coming “information superhighway” arena (internet and content). The deal would, at that time, have been the largest-ever U.S. merger.

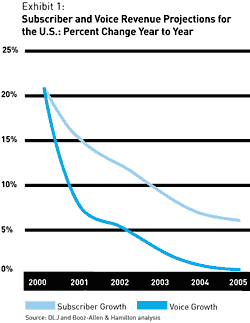

In retrospect, the whole strategic thrust was misplaced, as the voice business was at the cusp of major decline as a driver of revenue and profit. At the time, voice conservatively was described as a $100 billion annual business.”

Presumably that referred to the amount of local access revenue, as total fixed network revenues in 1998 were closer to $246 billion. In 1999, long distance voice alone represented about $111 billion.

The point is that the big revenue upside driving the AT&T merger with TCI was viewed as local voice services.

Instead, U.S. voice line usage peaked around 2000, with revenues peaking about 2002. And revenue growth shifted to mobility (product substitution) and internet access (fixed network).

So the question is whether a merger of Sprint and T-Mobile US, intended to strengthen the new firm’s ability to compete against Verizon and AT&T in the mobile segment, is any better, as a strategy, than spending capital and effort to gain share in the voice business was in 1998.

It already seems possible that revenue growth and value are shifting again. Where voice growth was replaced by revenue gains from mobile substitution and fixed network internet access and entertainment video, so one might well ask whether growth in the next phase might shift again.

Already, observers predict that the value of a fixed network is shifting, with more value driven by small cell backhaul and enterprise customers. Mobile account and internet access revenue growth is flat.

Others might argue that the whole point of consolidation (Sprint combining with T-Mobile US) is the ability to raise prices in the mobile segment of the business, which is the practical meaning of the argument that a merged entity could better compete with the likes of AT&T and Verizon.

On a practical level, since antitrust regulators signaled a year ago that such a combination would be challenged, it is not clear that anything major has changed.

A few such horizontal mergers have been opposed in recent years (AT&T plus T-Mobile US; Sprint plus T-Mobile US; Comcast plus Time Warner Cable). And even though vertical mergers that do not reduce the number of competitors in a market have been cleared (Comcast plus NBCUniversal; AT&T plus DirecTV), even some proposed vertical mergers (AT&T plus Time Warner) are being challenged by antitrust authorities.

One key question is the minimum number of suppliers needed to ensure reasonable levels of competition. It is empirically unclear whether, in any market, the minimum number of suppliers is as low as two, or as high as four.

It is possible that three major contestants would still provide reasonable competition in the mobile market, even if such consolidation also allows more pricing power within the market. Of course, the markets are in motion. Long-term roles for fixed and mobile operators are fluid; new competitors are emerging and revenue sources are evolving.

At some point, when Comcast and Charter emerge as bigger providers, possibly as facilities-based suppliers, such a merger might not have the same consequences. Or, alternatively, it is possible that a Comcast or Charter actually becomes the owner of one or both of those assets.

In principle, that leaves open the possibility that the “mobile market” could still be lead by four providers (Verizon, AT&T, Comcast and Charter, each owning either Sprint or T-Mobile US). ]

Other combinations also are possible, of course.

The point is that antitrust action that was signaled a year ago still seems likely, should a Sprint-T-Mobile US merger be proposed again. And even if unopposed, the likelihood of long-term sustainable success is somewhat doubtful (the markets are changing and big mergers fail more than they succeed).

No comments:

Post a Comment