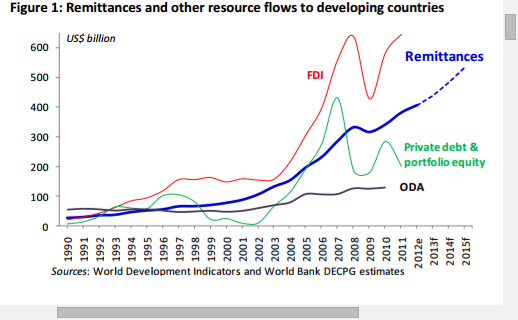

One should not underestimate the impact of widespread smartphone usage as a boost for economic development. In fact, private investment, remittances and other market-based investment in developing regions vastly outstrips the amount of official development assistance provided by governments and other aid agencies.

In fact, such private market investment and financial flows outstrip official development aid by at least an order of magnitude.

Increasingly, smartphones and Internet apps (especially social media and other communications patterns), plus banking and money transfer using mobile phones, are playing a key role in many investment and remittance operations.

Early on, perhaps 10 percent of the gross domestic product of Kenya moved through M-Pesa, the mobile payments service. By 2014, more than 20 percent of Kenya’s GDP moved through M-Pesa. That can be estimated at 42 percent if one counts both sender and recipient activity.

The latest developments are happening in services and systems to allow lenders to better assess credit risk, when traditional measures are unavailable.

Connecting small business owners and entrepreneurs with trade finance is the mission Rwandan company Kountable accomplishes using mobile phones and a method of assessing creditworthiness using social networks. The whole point is fast and accurate due diligence on ability to repay a loan.

Launched in May 2015, deals ranging from as low as US$2500 and as high as $500,000 have been facilitated, says Chris Hale, Kountable CEO.

Kountable is not a loan originator, however. It provides assistance to lenders and borrowers. Basically, Kountable reduces risk when a supplier and financing entity agree to enable delivery of goods to a merchant.

“We help you purchase raw materials, stock or inventory and get paid by your end client so you don’t have to worry about funding these purchases as part of your transaction,” says Hale.

“We are focused on business finance needs that require short term support which does not exceed one year and though there are no limits on how much, we want to benefit as many businesses as possible so we want to keep the bulk given to each business within the range that we have handled in the past ($2500-500,000),” Hale says.

Kountable measures creditworthiness by evaluating an entrepreneur’s social capital—their network of contacts and relationships. In cases where an applicant does not actively use social networks, a score can be constructed from email data.

The scoring alogorithm, as with any other method, assumes that one’s past business relations, activities and behavior tend to predict future behavior.

Ideally, though, an applicant’s kScore is generated by measuring the activity and size of social networks (social networking sites) as well as phone and text messaging contacts and email profiles.

Based on an algorithm that looks at several dimensions of all that data, applicants are scored with a numerical value between 500 and 1000 that is a proxy for creditworthiness based on social capital.

The company says it can make a credit score in five to 10 working days.

Kountable works to raise funds in the United States for such entrepreneurs using the kScore, offering lower rates than otherwise would be available.

The Kountable business model is a two-percent-per-month financing fee on the value of loans made by third parties.

The significance is that, since about 1995, private activities have vastly surpassed the value of official development assistance as sources of capital inputs in developing countries. Kountable is part of that trend.

No comments:

Post a Comment