It is conceivable that mobile operators globally will make more money providing home broadband using fixed wireless than they will earn from the flashier, trendy new revenue sources such as private networks, edge computing and internet of things. And that might be true even if those other new revenue sources represent vastly more connections, sites or contracts.

Wells Fargo telecom and media analysts Eric Luebchow and Steven Cahall predict fixed wireless access will grow from 7.1 million total subscribers at the end of 2021 to 17.6 million in 2027, growth that largely will come at the expense of cable operators.

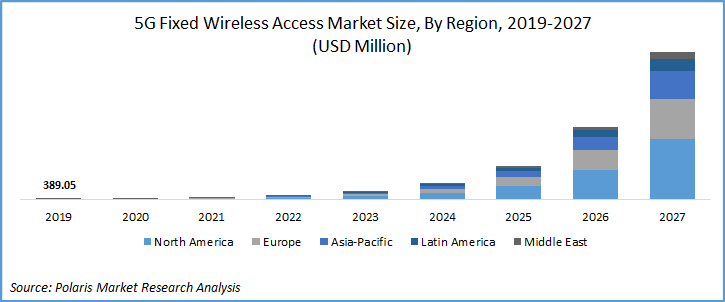

source: Polaris Market Research

If 5G fixed wireless accounts and revenue grow as fast as some envision, $14 billion to $24 billion in fixed wireless home broadband revenue would be created in 2025.

Consider the U.S. market. By some estimates, U.S. home broadband generates $60 billion to more than $130 billion in annual revenues.

If the market is valued at $60 billion in 2021 and grows at four percent annually, then home broadband revenue could reach $73 billion by 2026. $24 billion would represent about 33 percent of total home broadband revenues.

If we use the higher revenue base and the lower growth rate, then 5G fixed wireless might represent about 10 percent of the installed base, which will seem more reasonable to many observers.

Assuming $50 per month in revenue, with no price increases at all to 2026, 5G fixed wireless still would amount to about $10.6 billion in annual revenue by 2026 or so. That would have 5G fixed wireless representing about 14 percent of home broadband revenue, assuming a total 2026 market of $73 billion.

If the home broadband market were $134 billion in 2026, then 5G fixed wireless would represent about eight percent of home broadband revenue.

Do you believe U.S. mobile operators will make more than $14 billion to $24 billion in revenues from edge computing, IoT or private networks?

In fact, do you believe 5G mobility services will drive much revenue increase? The issue is opaque. U.S. mobile operators increasingly are taking the marketing tack of moving customers to higher-priced accounts featuring unlimited usage and then enabling 5G access as a feature of that upgrade.

So is it 5G driving the increase in revenue per account, or is it the upselling of service plans? Some of us would argue it is the latter, not the former.

The GSMA has argued that fixed wireless would be a key driver of 5G value.

By way of comparison, low average revenue per device might well mean that even high numbers of sensor connections do not drive especially notable connection revenues for mobile operators.

Nor might private networks or edge computing revenues be especially important as components of total revenue. It is almost certain that global service provider revenues from multi-access edge computing, for example, will be in the single-digit billions ($ billion) range over the next few years.

The same is true of forecasts of service provider internet of things revenue. The service provider 4G or 5G private networks revenue stream is likely to be small as well.

All that implies that 5G fixed wireless might be the most-material--and largest--source of new service revenues for mobile operators.

No comments:

Post a Comment