Forecasts of 5G revenue have to be considered in a nuanced way, in large part because a displacement process will be at work: an existing 4G account that is converted into a 5G account often has relatively slight net impact on revenues or profit, even if gross revenues are certain to grow.

In other words, 5G might be relatively revenue neutral in a net sense, even though we can fully expect 5G revenues to grow substantially. At least so far, much of the incremental revenue lift we have seen from 5G has come from convincing subscribers to move from lower-priced service plans to higher-priced plans.

Moving subscribers to higher-priced unlimited usage plans that include 5G as a feature provides one example of the upgrade process. But such changes might only indirectly be attributable to “5G” adoption.

Most of the net change in 4G or 5G revenues will be driven by replacement. For existing customers, 5G adoption also means abandonment of 4G.

That process of displacement has been happening since 2G, when many consumers had become mobile users, and upgraded from 2G to 3G services.

The other issue is the degree to which new incremental service revenues can be created. There is much optimism about new revenue sources.

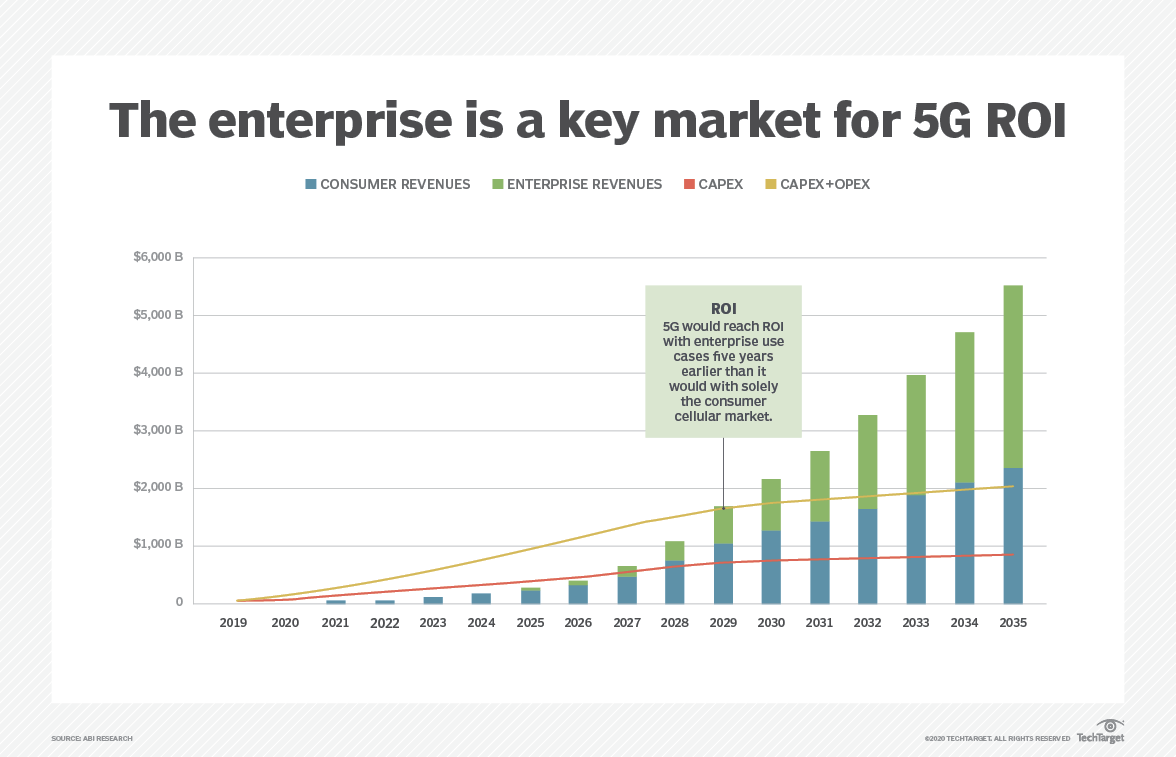

This forecast developed by ABI Research for Interdigital shows the possible importance of "industrial" revenue, compared to consumer revenue, even if most observers might consider this outcome a very-slight possibility.

The key assumption here is that return on investment comes from enterprise services, not consumer services. That presumably assumes that profit margins on enterprise services are much higher than consumer profits, even if consumer revenues continue to provide the majority of total service revenues.

Whether this proves to be correct is the question.

No comments:

Post a Comment