What do prices for U.S. C-band spectrum tell you about the value of mid-band spectrum? At a strategic level, the C-band arguably will be as foundational for 5G as the AWS spectrum was for 4G.

But much else has to be interpreted. Most reports focus simply on the amount of revenue raised in the auction (more than $80 billion) and the implications for mobile service provider balance sheets.

The total amounts spent are important, but also misleading, as the C-band auction also involved the largest single offering of low-band or mid-band spectrum, ever. The 280 MHz of capacity was easily four times the amount of AWS spectrum that proved to be foundational for 4G networks, and four times the amount of the Citizens Broadband Radio Service spectrum at 3.5 GHz sold in 2020.

To be sure, the millimeter auctions held so far, and any to follow, represent more raw capacity, balanced by signal propagation issues that limit coverage. But millimeter wave spectrum has to be evaluated on different metrics than the low-band and mid-band spectrum.

Capacity might be an order of magnitude or more higher than mid-band spectrum and at least a couple of orders of magnitude more than low-band. That does not mean bidders will pay an order of magnitude more for that spectrum.

Looking at the AWS-3 auction, the recent Citizens Broadband Radio Service and the C-band auction, AWS-3 made 65 MHz of capacity available. The CBRS auction held in 2020 represented about 70 MHz of licensed capacity. The C-band auction was for 280 MHz of capacity.

Price hinges on value, and the CBRS auction represents assets with the most restrictions (where it can be used, power limits). The nationwide CBRS average price per MHz-POP across all categories in the auction was $0.217 price per MHz-POP.

The AWS-3 auction in 2015 had a national average price per MHz-POP of $2.20.

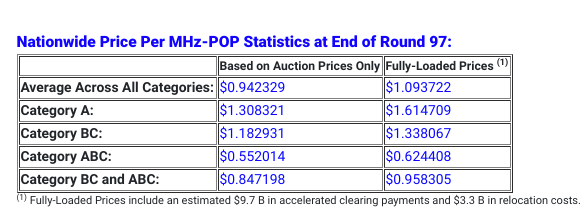

The C-band auction had an average national price of $0.94 per MHz-POP. After expected clearing costs, the average price might reach $1.09 per MHz-POP.

Also, some of the C-band spectrum blocks were considered more valuable because the spectrum could be cleared and put to commercial use sooner. The Block A frequencies--100 MHz in five 20-MHz sub-blocks in the 3.7- to 3.8 GHz range--are expected to be cleared for use by December 2021.

The B Block--100 MHz of five 20-MHz sub-blocks, will take perhaps a year longer to clear. The C block--80 MHz of 20-MHz channels--might also take a year longer to clear.

So A Block spectrum was expected to sell at higher prices, and did.

According to analysis by Sasha Javid, COO of BitPath, the average price per MHz-POP for a Category A license was about $1.31, while that for BC licenses was $1.18 and $0.55 respectively.

Compare that to past spectrum transactions of mobile capacity (auction or asset purchase in secondary markets), where millimeter wave assets have sold for as little as $0.014 per MHz-POP, while some AWS-3 spectrum has sold for as much as $2.73 per MHz-POP.

The C-band auction will be expensive for the winners, in part because so much capacity was purchased: volume matters for spectrum purchases as for most other commodities. But the price per MHz-POP will be substantially lower than for the crucial AWS-3 spectrum, which arguably was foundational for 4G networks.

For AT&T, Verizon and arguably a few others, C-band assets are essential to maintain relevance in 5G services. It is a cost of being in business, in other words.

So the purchases are essentially a requirement for sustaining the business--table stakes--and less a means of gaining business advantage against competitors. Many fiber-to-the-home investments have similar character.

No comments:

Post a Comment