Business strategy in competitive markets largely free of regulatory constraints and major entry barriers tend to evolve towards a specific and stable market structure including the “rule of three” and the “rule of four.”

The rule of three states that a stable market is led by three firms. The rule of four refers to the expected market share in a stable market, where leader market share is twice that of provider number two, and where the number-two supplier has share double that of the number-three provider.

Which does raise an obvious question: is telecommunications the sort of business “free of regulatory constraints and entry barriers?” Many would say that is not the case. If so, the rules of three and four might not ever apply.

That was the case in the days of monopoly telecom, but that era has given way to competition.

Competitive telecom markets already exhibit reduced regulatory constraint (deregulation) and lower entry barriers (wholesale access, for example).

And though BCG founder Bruce

Henderson believed industries such as consumer electronics, software and computing hardware, investment banking and telecommunications would be the exceptions to the rule, others might argue the classic rule of three and rule of four pattern already has emerged in the internet ecosystem, software and hardware.

Others might note that one way of changing a market share position is to disrupt the industry, changing the basis of competition; the product; the experience or the value.

Bruce Henderson, founder of the Boston Consulting Group is credited with a few foundational ideas about business, including the notion of the experience curve, which explains how the cost of products decreases with volume.

“Costs characteristically decline by 20 percent to 30 percent in real terms each time accumulated experience doubles," Henderson posited in 1968.

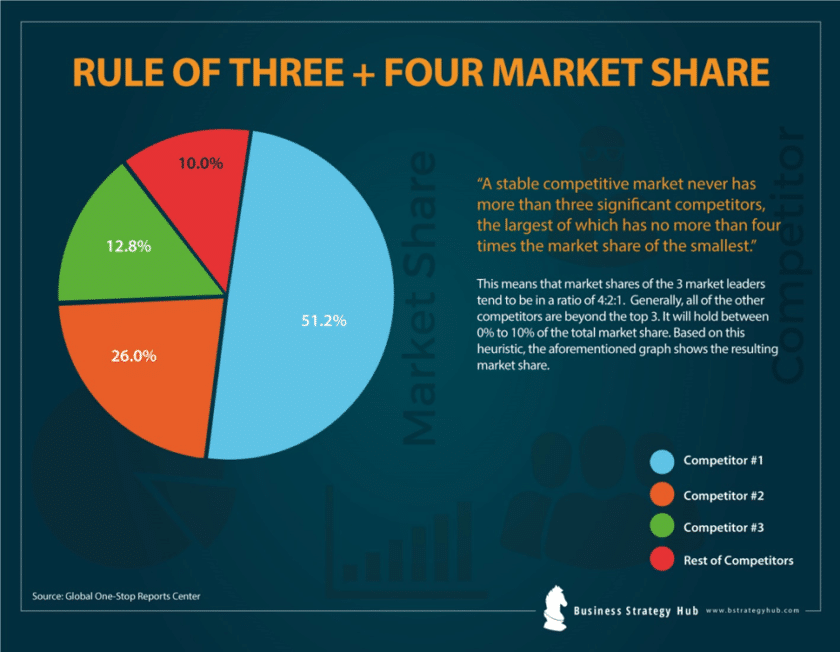

Among his other key ideas is the shape of market structure under conditions of competition. "A stable competitive market never has more than three significant competitors, the largest of which has no more than four times the market share of the smallest,” Henderson argued. He called that the rule of three.

Related is the “rule of four,” which speaks to expected stable market share structure. Henderson argued that stable and competitive industries will have no more than three significant competitors, with market share ratios around 4:2:1.

Industry structure will become stable once the market share between two companies reaches a ratio of 2:1, Henderson theorized. “At this point, it is neither advantageous nor practical for either company to decrease or increase share,” Henderson noted.

Those ratios also have been seen in a wide variety of industries tracked by the Marketing Science Institute and Profit Impact of Market Strategies (PIMS) database.

Researchers Rajendra S. Sisodia and and Jagdish N. Sheth analyzed the evolution of about 200 competitive markets about the year 2000.

“Competitive markets evolve in a predictable manner and, once mature, exhibit many similarities across industries and geographies,” said Jagdesh Sheth. Stable markets tend to be dominated by three major, volume-driven firms

The three large firms typically represent 70 percent to 90 percent of the total market share. To be viable, a leader requires a market share of at least 10 percent, Sheth argues.

The starting point for a new market is almost always a new technology, and new markets tend to be highly fragmented, Sheth says. Early entrants tend to be product specialists in such areas.

New markets tend to have few technical standards at first, with low barriers to entry and exit, and a decidedly local geographic focus. If the market satisfies a legitimate need, it will generate excess capacity as more entrants emerge.

That leads to consolidation, standards-based competition and rationalized competition. Government regulators or collective industry data sharing, electronic exchange and other measures to improve the speed and ease of transactions often are part of the rationalizing process.

Scale and efficiency, in other words, become important as the market matures.

The mature phase in any industry also has some common characteristics. When markets become saturated, growth slows dramatically. That tends to raise costs and reduce profit margins.

As total revenues decline over time, firms tend to focus on profit margins rather than gross revenue, as, by definition, gross revenues are shrinking overall. Operational efficiency becomes paramount, as there is limited upside from investing in new features and products.

Outsourcing and other moves to lower breakeven costs are logical.

Investment will be optimized and controlled, as deploying new capital produces a limited financial return.

Other firms begin to exit the business and merger activity increases.

The takeaway is that every firm has to decide whether it really can hope to become a leader of the industry or must operate as a specialist of one sort or another. Any firm realistically contending for leadership of the market must decide whether it is realistic to make an assault on the market leader, or whether it is feasible to supplant the firm which is number two in share.

When market share reaches a clear 4:2:1 pattern, observers might say the market is so settled that the effort to change share is doomed to failure. Few mobile markets are in such a settled condition.

No comments:

Post a Comment