For those who worry about the impact of a three-provider U.S. mobile market, one might offer up the situation in Canada, where three national carriers exist, compared to four in the United States.

The United States, with four major service providers, is in the big pack of “average” price countries. In other words, there is some apparent evidence of market power leading to higher prices in Canada, with three providers, compared to the U.S. market, with four providers.

One might point to other drivers, such as a regulatory regime that is less supportive of competition, as possible influences as well. It is not unusual for large telcos--or large firms of any type, anywhere--to oppose new competition.

Still, levels of Canadian competition seem restrained, compared to U.S. levels, in part because Canadian government seems more willing to bar new competition, by law, including rules that restrict the level of foreign competition. Generally, there is less regulatory support for competition in Canada, compared to the United States.

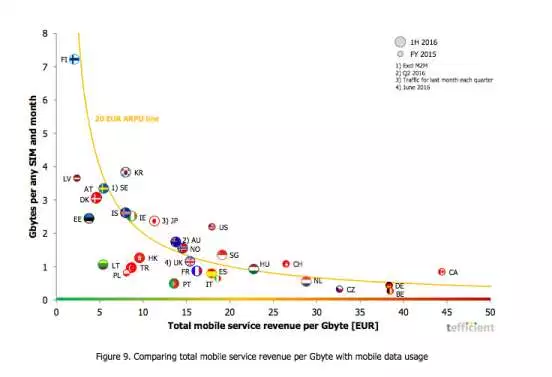

Numerous studies have shown that Canada has the highest mobile phone service prices among developed countries. In fact, one study by Tefficient suggests Canada has the highest prices among developed countries.

Any study of highest mobile prices necessarily has to be put into context. But most who live in Canada or roam into Canada might agree that prices seem high. That might strike some as a bit odd.

Canada and the United are not just continental neighbors but similar in many economic measures, such as gross domestic product per person.

As always, international comparisons of prices require adjusting for purchasing power parity. Prices are most relevant when compared against the price levels within any single country, as when a “percent of income” is used, rather than prices in any given currency.

It also matters which specific plans are chosen for comparisons between service providers and nations. Where many plans are offered, some variance is noted, in terms of cost rankings, within and between countries.

Significant also is that any study of retail plans does not include promotional discounts that consumers might be using to reduce effectively-paid prices.

Nor do studies tend to adjust findings based on actual buying behavior. In other words, some plans might be especially expensive, but might be bought by almost no customers, or relatively few.

The bottom line is that it is not easy to forecast what happens to competition in the U.S. market if the number of leading mobile firms is reduced from four to three. Logic and economic theory suggests less competition means more pricing power. Virtually all equity analysts who follow the U.S. mobile industry believe that is the outcome of market consolidation from four to three national providers.

Perhaps one difference is that other competitors already are emerging in the U.S. market, notably Comcast and Charter. Using different platforms and business strategies, they could act to restrain market power by the leading mobile service providers. So, in principle, might other contestants from other parts of the internet ecosystem.

That might be easier now that many ways of using spectrum are developing, ranging from much more unlicensed spectrum to shared spectrum; spectrum aggregation and small cells and millimeter wave assets.

In the long run, some might argue, market power in mobile communications will be challenged in new ways, in any case.

No comments:

Post a Comment