Multi-product business models work best a constant stream of big new revenue-creating products are created to replace mature products. For the mobile industry, which drives the whole telecom industry, the biggest question therefore is "what big new product drives the next wave of growth?"

It's an open question, despite the optimism about internet of things. After every human being who wants to use mobile phones has got one; after every human buys mobile internet access; what comes next?

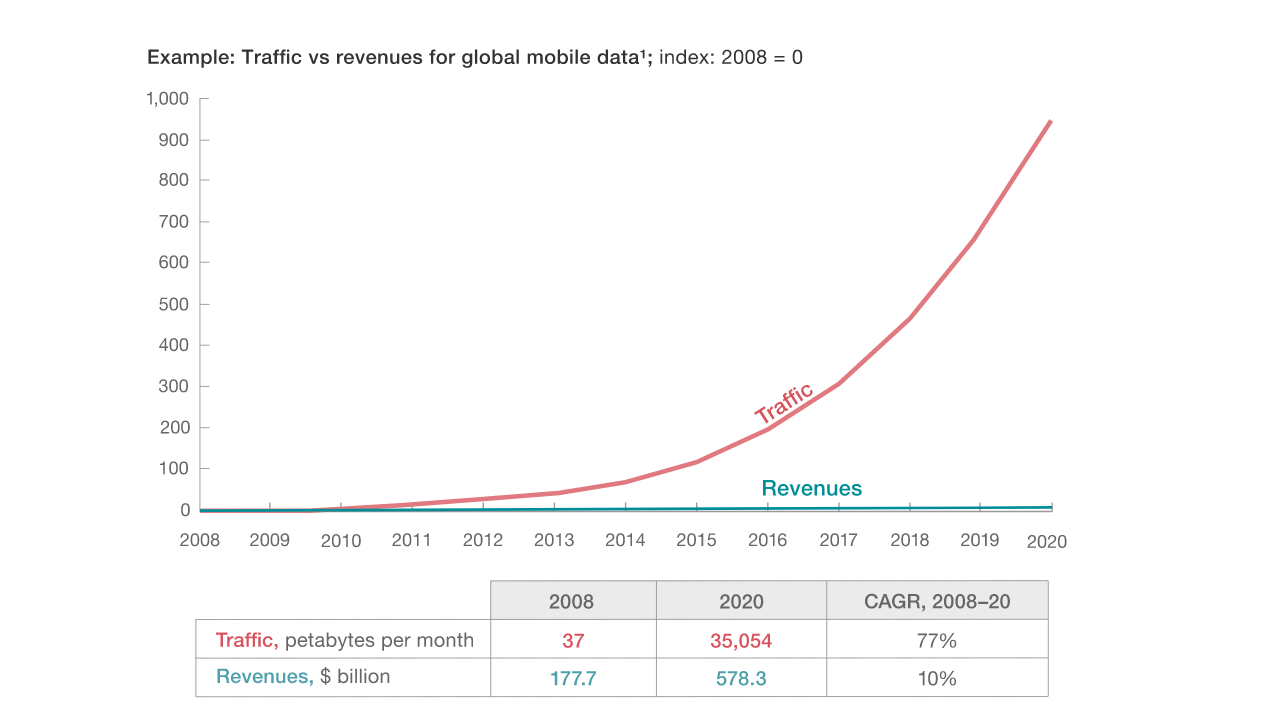

Whatever it is, it has to be big, as the global telecom industry already is about a $1.5 trillion annual revenues industry. To move the needle, any new sources have to be large, simply to replace lost revenues from legacy sources. Roughly speaking, to sustain three percent annual revenue growth, and assuming zero losses in all legacy sources, some $45 billion has to be added every year.

Do platform-based product substitutes lead to declining total industry revenues, an increase or are they basically neutral? The answer might well be “yes.”

When usage, the number of subscribers and users is growing fast, even legacy product abandonment does not necessarily slow revenue growth.

That might be true even when competition and technology are lowering prices per unit sold.

If there is a clear pattern at all, it seems to be that revenues grow about as you would expect from a standard product life cycle analysis: some growth early on, fast growth as mass market adoption happens, then slowing growth as markets saturate.

But that describes total industry fortunes only in a single-product scenario, and telecom long ago became a multi-product industry.

The result is slow growth in mature markets, faster growth in developing markets, with product changes happening in all markets, nearly all the time.

In the case of fixed voice lines, product substitution increased overall revenues, since sales were to “people,” not “places,” and there are more people than places where a voice line makes sense to buy.

In the case of text messaging, over the top alternatives shrank the total market, even as volume ballooned, since usage grew dramatically.

By 2021, fixed voice will represent only about 7.7 percent of total global telecom revenues, compared to mobile at 59 percent of total, according to researchers at Ovum.

Fixed network broadband will represent 18 percent of total revenues, while subscription TV represents about 15 percent of total revenues.

The global telecoms & media market will generate $1.58 trillion in revenues in 2021 from 11.96 billion connections, according to Ovum, which counts fixed network, mobile network and video services in its tally.

The mobile segment will dominate, with revenues of $933 billion and nine billion connections in 2021, Ovum predicts. However, fixed broadband will be the fastest-growing market, with revenues growing at a compound annual growth rate of 3.02 percent from 2016 to 2021, ahead of subscription TV at 2.51 percent and mobile at 1.91 percent.

Global broadband will generate $288 billion in revenues in 2021, ahead of subscription TV with $239 billion and fixed voice at $122 billion.

Not all estimates include video. But even some of those forecasts are in line with Ovum projections.

The relative importance of mobile, fixed broadband, and subscription TV markets varies by country and region.

In 2021, the mobile market will generate 87 percent of total telecom and media revenues in Africa and 70 percent in the Middle East, compared to 50 percent in North America and 49 percent in Western Europe, Ovum predicts.