In the wireless business--mobile, untethered or fixed--supply and demand matters. Scarcity accounts for the value of mobile spectrum, for example. So any big changes in supply will be reflected in both demand changes and “asset value.”

To be sure, different blocks of spectrum are deemed to have different value, based on propagation characteristics. That is why 700-MHz spectrum for mobile, or 600-MHz spectrum , might often sell for much more than 2 GHz spectrum.

Of course, some also will note that costly spectrum is the second-biggest problem for a service provider dependent on licensed spectrum access. Having no spectrum is the bigger problem. The former problem makes the business case more difficult. The latter problem makes the business case largely impossible.

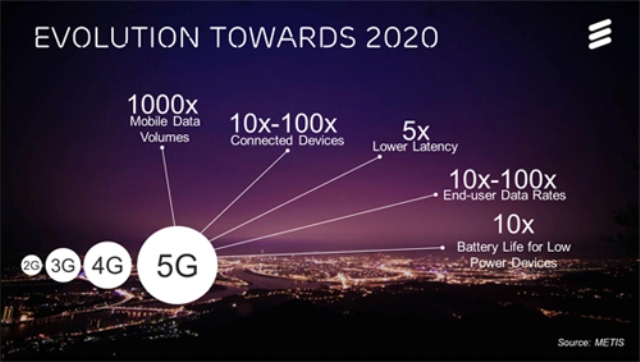

But business cases built on scarcity cannot survive unchanged if there is a dramatic step function in supply, or a dramatic step function in demand, up or down. And one has to account for a coming big step function in spectrum supply that will increase wireless and mobile supply by an order of magnitude or even two magnitudes.

Those radical changes in supply likely will affect the scarcity premium placed on lower-frequency signals. And so it will be with the coming era of millimeter wave communications.

In the U.S. market, millimeter wave frequencies have been commercially deployed for decades, and talked about as the next frontier for mobile communications for just about that long, as well.

It might be worth noting that fully 90 percent of radio frequency spectrum lies in the millimeter wave regions between 30 GHz and 300 GHz.

Recent tests suggest of 28 GHz and 73 GHz radio systems “demonstrate that, even in an urban canyon environment, significant non-line-of-sight (NLOS) outdoor, street-level coverage is possible up to approximately 200 meters from a potential low-power microcell or picocell base station,” the researchers from NYU Wireless say.

In other words, as a capacity tool, millimeter wave small cells might cover a diameter of about 400 meters (about a quarter of a mile). That might not be as helpful for rural access, but in an urban environment, would be significant. The NYU Wireless tests suggest an order of magnitude boost in capacity is quite possible.

The Federal Communications Commission plans to initially open up nearly 11 GHz of high-frequency spectrum for mobile and fixed wireless networks, of which a whopping seven gigaHertz will be available for unlicensed use.

The rules create space for service in the 28 GHz, 37 GHz, and 39 GHz bands, and a new unlicensed band between 64 and 71 GHz.

The FCC also wants to release another 18 GHz of spectrum encompassing eight additional high-frequency bands, for a total of 29 GHz of new communications spectrum.

Bringing stakeholders together to understand changing supply and demand issues, and the business model for Internet access, is a key focus of the Spectrum Futures conference. Here’s a fact sheet and Spectrum Futures schedule.