Perhaps it is not too early to argue that new 6G network capabilities will emerge, but will have less to do with mass adoption of new use cases and value than most would expect. The reason is that computing architectures now separate network functions from app functions.

If that is the case, then new apps should emerge independently from the networks, as new business models, use cases and features are created by devices and apps on those devices, not the network transport and access providers.

Indeed, one might argue that is the whold point of the layered architectures underpinning all modern apps, devices and computing.

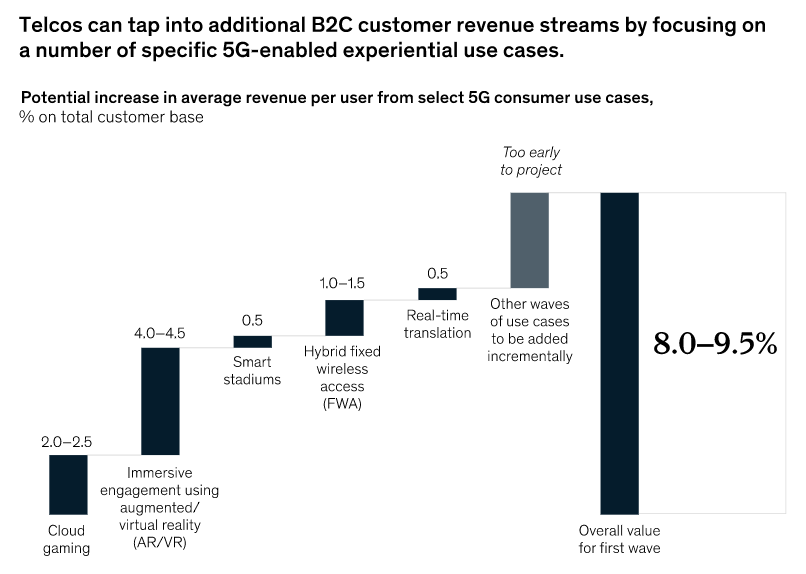

Expectations for 5G new revenue sources sometimes included consumer revenue upside as well as business revenue opportunities. Some might argue that faster speeds have boosted average revenue per account, as 5G service plans sometimes are marketed at higher prices than equivalent 4G accounts.

So far, though it is early in the 5G era, fixed wireless seems to be the only identifiable new revenue source with material upside impact, aside from gains from “5G consumer accounts” that essentially are a substitute for the former 4G accounts consumers were buying.

The value proposition is not always clear. In some cases, the value might be faster speeds, or non-material bragging rights. In other cases, 5G might be bundled with other values consumers value, such as billing predictability in the form of unlimited usage plans.

In other words, customers bought the unlimited plans, with 5G being a feature of those plans.

In some cases, no ARPU lift from 5G has been seen. In other cases, 5G is correlated with higher ARPU.

Still, fixed wireless seems to be the first “new” 5G revenue driver that materially lifts service provider revenue. 5G home broadband market share and revenue impact are material elements for T-Mobile and Verizon, for example. In some cases, fixed wireless might be said to account for nearly all net new account adds in recent quarters.

Virtually all the other new use cases, including private networks, edge computing or IoT, have yet to show similar identifiable revenue impact. That does not mean they cannot do so, only that they have not done so yet.

So far, aside from fixed wireless and replacement of 4G accounts by 5G, it would be difficult to quantify 5G revenue success.

And though it remains quite early as well, the talk about 6G likewise focuses on lead themes that might, or might not, actually be tangible revenue drivers for mobile service providers, even if new services, use cases and value do emerge.

6G will be a “sensing network,” some believe.

“The logical next step is to extend these radio sensing capabilities beyond specialized machines and applications and place them in every cell and node of the wireless communication infrastructure that surrounds us today,” say Thorsten Wild, Nokia Bell Labs Head of Next Generation Wireless and Harish Viswanathan, Nokia Head, Radio Systems Research group.

As always, there will be multiple ways to solve any particular problem or create a capability. Whether it is the network that does so, a device or an application, is the issue.

“In outdoor environments, the network could detect the location, speed and trajectory of all vehicles and pedestrians in an area, issuing warnings if any of their paths are about to intersect,” the researchers say. “Or the network could simply search the block for empty parking spots.”

“At work or at home, the network could detect if a vulnerable person has fallen and even “hear” their heartbeat, alerting emergency responders about possible trauma,” the authors say.

Of course, those functions also could be performed by devices, including smartphones, or apps running on smartphones and other devices, without 6G networks necessarily doing so.

So the same fundamental issue likely faces 6G, just as similar issues have faced all networks in the internet era, when applications are separated from network features and services. Devices and apps already can “sense falls.”

With artificial intelligence capabilities developing rapidly, who would argue that networks will be mass drivers of new use cases when devices and apps likely can be deployed faster?

Perhaps we now are in a period where network capabilities (speed, latency, positioning) will clearly be relegated to physical layer roles, as apps and devices are the primary developers of new use cases and capabilities.

No comments:

Post a Comment