Will connectivity service providers sustain themselves strictly on 5G connectivity revenues through 2030? Maybe not. Bearing Point forecasts negative two percent industry revenue growth to 2030. Will 5G help? The answer is not clear yet.

Many service providers expect revenue lift up to 15 percent from 5G. The issue is whether this is a reasonable expectation, and where the anticipated revenues will be produced. Will the boost--and how much--come from connectivity services (more accounts, more revenue per account) or solutions built upon 5G?

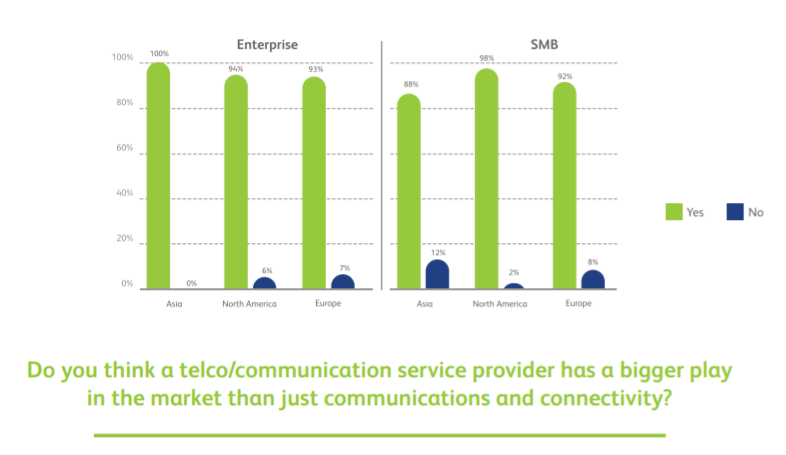

At least at this point, an overwhelming percentage of surveyed business customers believe connectivity providers do have a role to play in 5G-enabled business solutions, especially when telcos partner with app providers, integration specialists and others.

Connectivity service providers generally anticipate that 5G business-to-business (B2B) use cases will have a significant impact on current revenues. On average, service providers expect a 15 percent revenue bump, with North American and European suppliers slightly more bullish at 16 percent. How that happens is the big question.

Connection growth can help, especially if billions of new distributed internet of things connections are bought, and if a great bulk of those connections accrue to telcos, and not to rival suppliers, and if substantial numbers of connections are wide area, not local.

But most observers believe the bigger revenue upside will come from solutions, not connectivity, potentially. And that is likely where the big challenge will come.

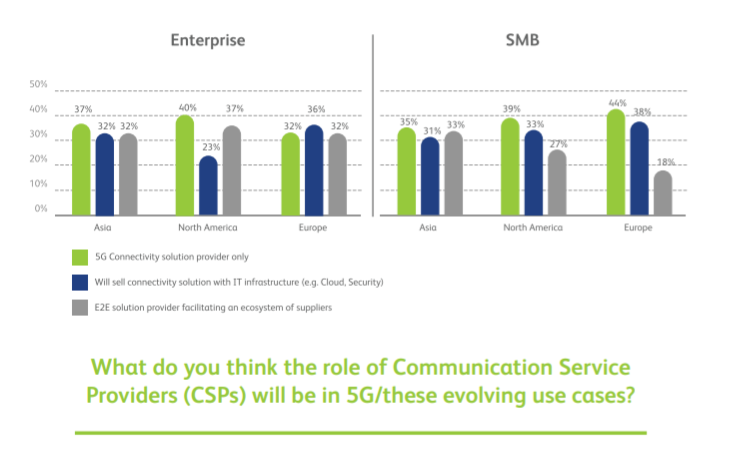

A survey by BearingPoint found that “roughly a third of enterprises and four in ten SMBs perceive the service provider’s role in 5G use cases as a simple connectivity provider.” Those are significant numbers, if they prove to be correct.

If service providers were to limit themselves to this role, and maybe five percent of enterprise and SMB ICT spend, then they will both be commoditized and struggle to fund 5G investments, particularly standalone 5G networks, BearingPoint argues. The economics simply won’t work, BearingPoint argues.

Perhaps the good news is that significant percentages of end users believe connectivity providers, partnered with other entities, will be reasonable choices as solution providers.

Ironically, business customers seem to be much more confident that connectivity providers have a key role to play as suppliers of 5G-enabled solutions than many service providers do, in Europe and Asia. But service providers might be more realistic than customers are, at the moment.

Asian service providers are more likely to focus their 5G efforts on more traditional connectivity-driven models than higher value services approaches, BearingPoint says. To be sure, 46 percent of Asian service providers see themselves as solution providers, going beyond the connectivity plus IT infrastructure services that are common today.

Another 17 percent see themselves as end-to-end actors facilitating an ecosystem of providers But Asian business customers have more confidence in their service providers. Nearly all customers believe telcos are positioned to be more than communications providers.

Full 92 percent of Asian businesses would consider buying new technology solutions from service providers BearingPoint’s survey finds Enterprise and SMB customers would rather work with service providers due to their ability to orchestrate ecosystems of partners, manage complex programs, their knowledge and expertise around 5G and the fact they trust them more than other market players.

Nearly 70 percent of Asian business IT leaders think service providers should be offering 5G solutions combining connectivity with IT infrastructure, applications and other capabilities that would be offered through an ecosystem of partners.

In Europe, service providers seem even more pessimistic about moving out of the connectivity role. Just a third of service provider executives believe their role will extend beyond basic connectivity and infrastructure offerings.

Only 10 percent of European service providers believe they will enact a role of end-to-end providers facilitating an ecosystem of partners. Yet 92 percent of European businesses agree that service providers have a bigger role to play in the market than simply providing communications and connectivity.

More than three quarters of North American service providers agree that creating vertical specific solutions using ecosystems of partners represents a big 5G opportunity, though. Half of North American service providers expect to evolve into 5G solutions providers, with 40 percent of these service providers anticipating a role in which they’re end-to-end providers facilitating an ecosystem.

North American businesses are most positive about the role service providers will play in 5G, with 96 percent saying they believe telcos will do more than provide connectivity.

No comments:

Post a Comment