If I am reading this churn data correctly, it is going to be hard for new mobile service providers--Comcast, Charter Communications and Dish Network, for example--to break into the top ranks of the U.S. mobile business.

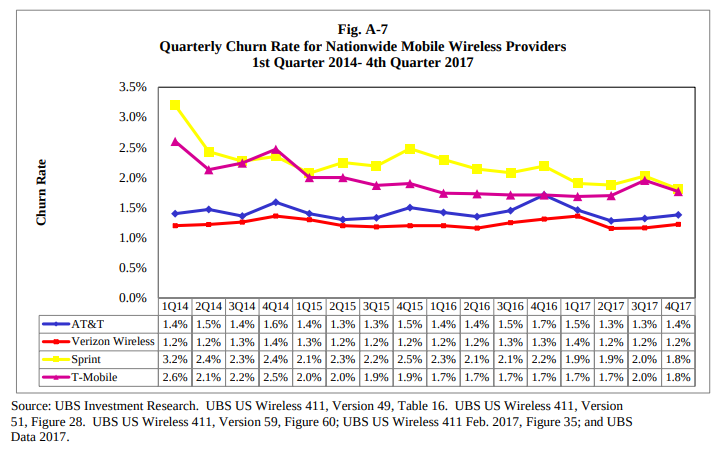

If I read the data correctly, the four national mobile providers lose between and seven percent and 5.5 percent of their installed base of customers each year. However, most of those losses arguably are to one of the other big four (soon to be big three) service providers.

The U.S. mobile business, in other words, is nearly a zero-sum game where one major provider’s wins come at the direct expense of one of the other existing providers. In any given year, perhaps half of one percent or less might actually shift from one of the top national providers to any of the other third parties.

It takes a long time for a competent new entrant to actually make market share inroads at such low rates of growth. Profitability is another issue. To the extent that mobility is a scale business, lack of scale means high costs and low profits.

For cable operators, that might be less a concern, since adding mobility also protects the rest of the cable bundle, while cable operators might hope to retain an advantage in operating costs and capex by using their hybrid fiber coax networks for access operations.

All mobile virtual network operators together had no more than about five percent share of the installed base of U.S. mobile accounts in 2017. Since then, some would estimate, that share has shrunk.

In 2017, perhaps five percent of all mobile accounts were supplied by MVNOs.

What is always tricky is the way MVNO accounts are attributed. In 2017, for example, perhaps 40 percent of all MVNO accounts were affiliated with one of the four national carriers. So it is possible that only about three percent of MVNO accounts actually are owned by third parties.

The larger point is that it will be difficult to take share from the top three national providers. They do not lose that many accounts each year, and most of the lost accounts are gained by one of the other two big service providers.

No comments:

Post a Comment