This is the moment when mobile service providers risk being forced back to being simply a utility, as electricity generation or railway networks were before them, Rethink Technology Research now argues.

Such arguments generally have a couple major assumptions. The first is that spectrum abundance will enable new competitors to enter the mobile market at lower costs.

In some markets, that will be particularly true for cable operators, who will leverage their fixed networks for backhaul, creating new mobile networks anchored by small cell coverage.

Source: Rethink Techology

In yet other cases, indoor venue providers will create neutral host facilities that support indoor access for all mobile service providers. That could lead to the rise of new indoor coverage providers whose business model is neutral host support for indoor mobile coverage.

In other cases the impact will largely be indirect, as enterprises build local 4G networks that, like Wi-Fi, remove some demand from the mobile network. The value of “unlimited usage” plans might be affected if the functional equivalent of Wi-Fi access for 4G or 5G is widely available.

In that view, the core value of the mobile network will remain its support for full mobility in outdoor spaces, while a range of other mechanisms are used to support indoor access (Wi-Fi, aggregation of licensed plus unlicensed spectrum; neutral host facilities).

It is not clear how all that shakes out.

Small cell networks built on new and unlicensed spectrum could have complicated effects. Indoor coverage networks could work to lower overall capital investment in mobile networks, as Wi-Fi effectively does. But such networks might also allow creation of new app layer functionality that, at least in part, renders mobile operators dumb pipe providers in new ways.

“Enterprise small cells, particularly those operating in unlicensed spectrum, could be the undoing of mobile network operators, relegating them to “utility” commoditization, and falling revenues, as both license free spectrum and shared are taken up aggressively by new competitors,” says Caroline Gabriel, director of research at Rethink Technology Research.

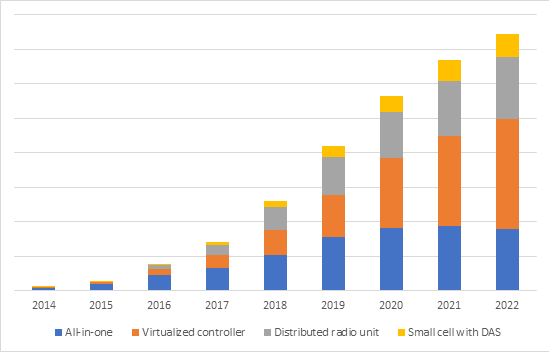

The rising popularity of enterprise small cells will mean that by 2022, enterprise units will account for almost half of all small cell deployments, up from seven percent in 2014.

The installed base will reach 14.8 million in 2022, up from 185,000 in 2014 and owners who invest in enterprise small cells will operate a financial grip on the market in the 2020 time frame.

There will be a rise in the importance of unlicensed spectrum driving enterprise and vertical small cells to scale with LTE-LAA roll-outs starting in 2018 and the more disruptive MulteFire running about nine to 12 months behind. By 2020 these two will account for 25 percent of all new deployments.

No comments:

Post a Comment