Is the era of mobile-driven telecom revenue growth nearing its peak? An odd question, it might seem.

But lead revenue sources have changed several times in the history of telecommunications, from account growth to long distance to mobility; consumer to business lead growth and back again; with periods where mobile growth was driven by accounts, then voice usage, then messaging and now mobile internet access.

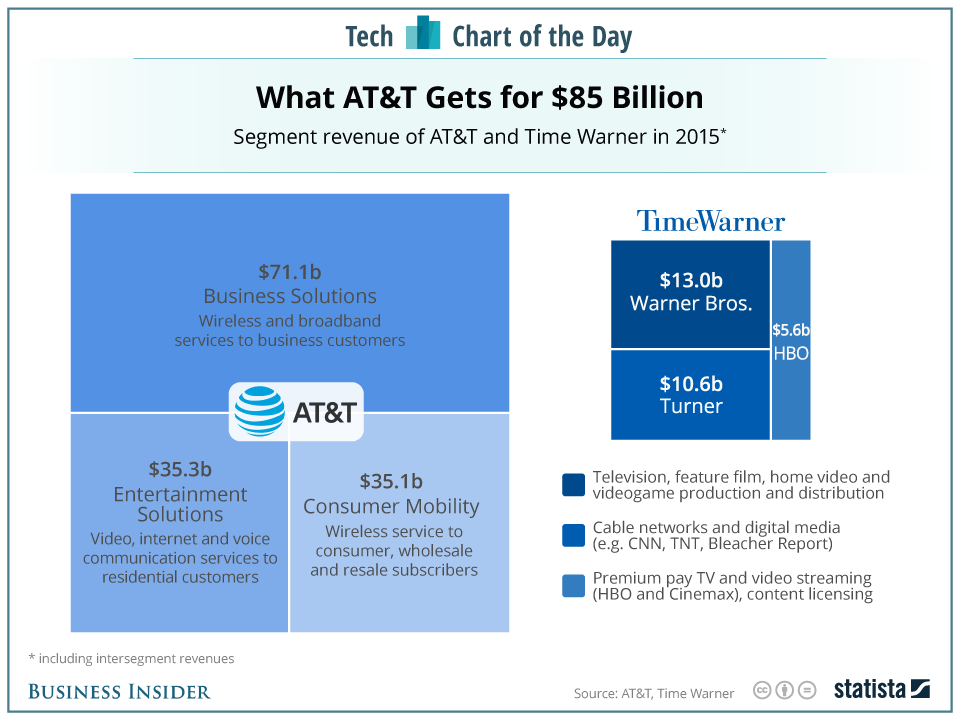

Consider AT&T, whose growth, at a high level, shifted from fixed network services to mobility, but whose next wave of growth will be fueled by content services. After the acquisition of Time Warner’s content-producing assets, entertainment will be the second-biggest producer of AT&T revenues.

While business solutions (mobile and fixed) will be the largest single revenue segment, entertainment will be second at perhaps $65 billion, with consumer mobility third at $35 billion or so.

AT&T’s moves suggest it believes further revenue growth is not going to come from consumer mobility, even if that had fueled decades of incremental revenue leadership. With accounts now saturated--virtually everyone who wants to use mobility now does--revenue growth has to come from selling more things to mobile and other customers, or convincing customers to buy in larger quantities.

You see the limitations of the “increase quantity” strategy clearly in the use of “unlimited usage” plans for domestic voice, messaging and internet access. AT&T and the other leading mobile operators are not paid more when customers use more.

The “growth by acquisition” trend seemingly will be unchallenged over the next decade, as acquisitions have contributed most of the growth in developed markets since about 2000.

The bigger trend is the shift away from “mobility” as the revenue growth driver. Once the driver of industry and firm growth, even mobility has reached the peak of its product life cycle. New sources, with equivalent scale, must now be found. In the near term, entertainment content is one answer. Tomorrow, it is likely to be enterprise services supporting internet of things.

In fact, the firm projects a five-year EPS growth rate of nearly eight percent, with a majority of the growth fueled by the Time Warner content operations. .

There have been waves of growth in the telecommunications business over the last 50 years, and in many developed markets, signs of a peak already are in place. In Western Europe, revenue growth now is negative, and has been for some years.

It will be some time before hard decisions must be taken by executives and firms in many developed markets where mobile accounts and revenue still are growing, if at lower rates than has been the case over the past couple of decades.

What the AT&T acquisition of Time Warner shows is that, in the U.S. market, the era of consumer mobility has reached its limit.

No comments:

Post a Comment