After decades of experience, it might now be time to conclude that telcos are not going to beat cable companies for internet access market share using any "wired" access platform. That is why 5G might be the most-important mobile platform since analog mobility itself.

Globally, mobile access already has proven to be the way most people use voice and internet access. But 5G will, for the first time, allow the mobile platform to compete fully with fixed access networks for the first time, both in terms of speed and retail pricing.

Telco results using what many would consider "the best" access platform--fiber to the home--illustrates the challenges of competing against cable operators with any cabled solution.

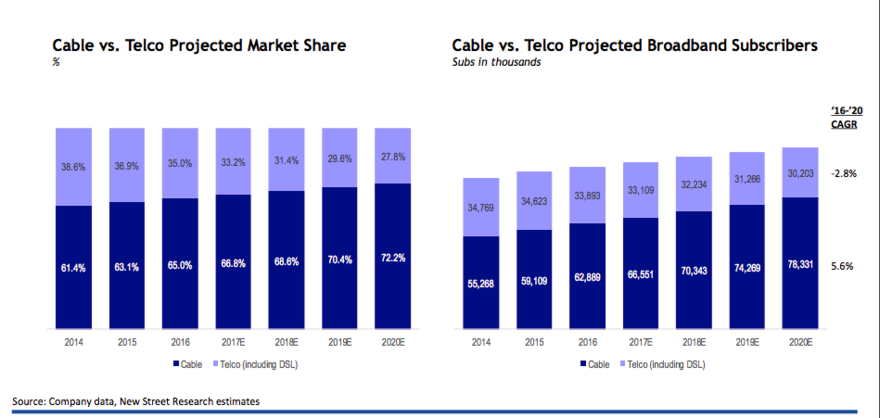

Facing accomplished competitors with scale, skill and other business resources, including their own facilities, a former incumbent telco might reasonably expect that its addressable market shrinks as much as half, because cable operators routinely take half of the customers in any market where they have the same scale of networks.

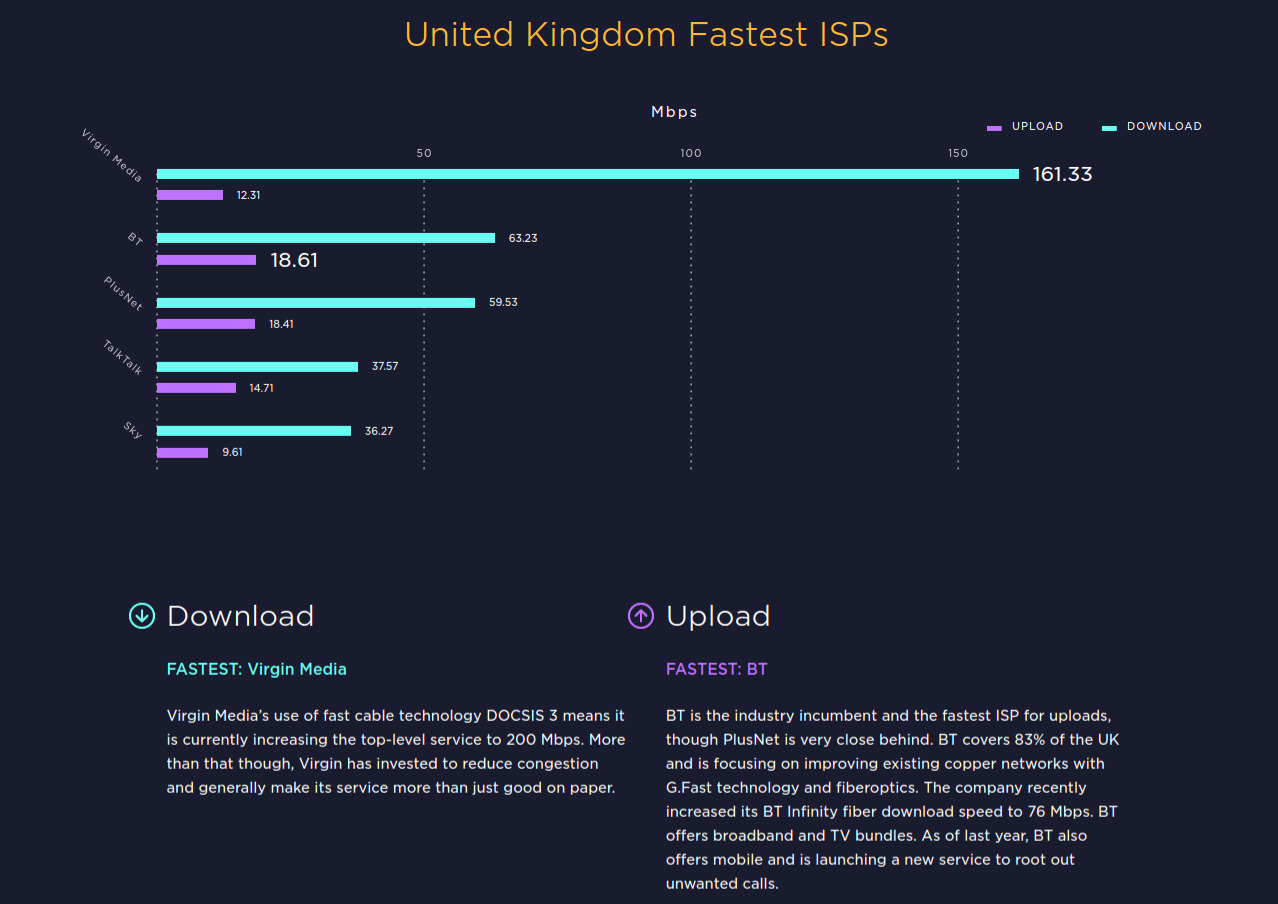

In the U.K., Virgin Media’s network reaches perhaps a quarter of locations, so national statistics do not actually tell us too much about what would be the case if Virgin had nearly ubiquitous coverage.

In the United States cable operators have close to 100 percent coverage of telco networks, that is an easy task.

Verizon’s experience with its FiOS service suggests a telco facing a cable operator might get 40 percent to 45 percent of the internet access market, even when fiber to the home is the access platform.

"At the end of the second quarter of 2017, cable had a 64 percent market share versus 36 percent for telcos,” said Bruce Leichtman, Leichtman Research Group president and principal analyst.

Unless something breaks the current trend, telos could collectively become something of an afterthought in the access business, with market share as low as 28 percent by 2020, according to New Street Research.

Mobile and wireless will help in several ways. Those methods will change coverage, capacity and potential pricing elements of service. Wireless access at gigabit speeds, with lower capex, will mean that mobile access (in mobile or fixed mode) will be retail performance and price competitive with fixed access for the first time.

Today, FTTH in the U.S. market strands as much as 60 percent of the deployed FTTH capital. If the maximum share is range bound around 40 percent to 50 percent, then any solution that minimizes stranded assets will improve the business case.

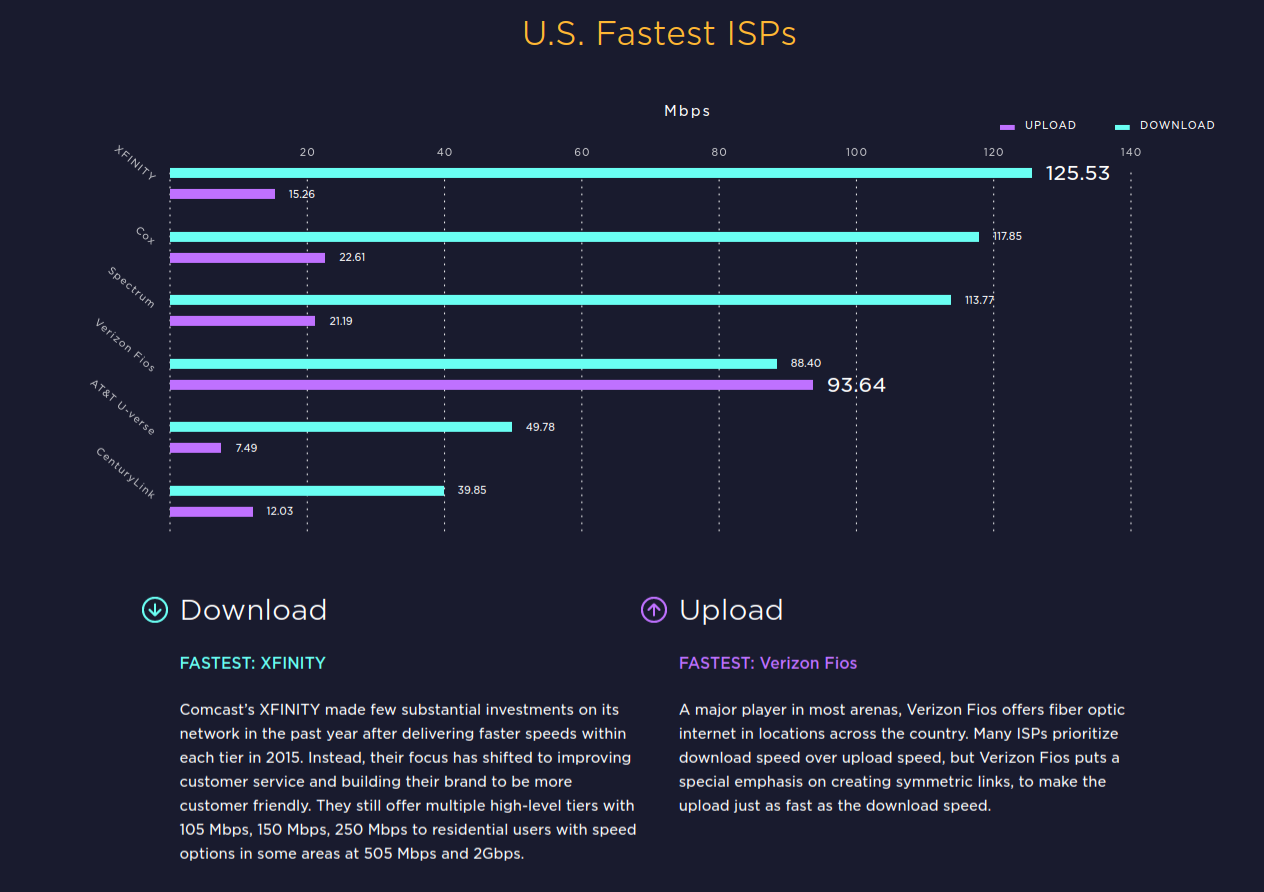

And telcos really need to find some workable answer to cable platforms, which have grabbed the lead in speeds and in the U.S. market leadership in terms of market share.

In 2016, for example, on U.S. fixed networks, “average” speed increased 40 percent in a single year, and most of that was driven by Comcast and other cable TV operators.

In the United Kingdom, in 2016, Virgin Media, the U.K. cable operator, was far and away the fastest ISP, offering speeds more than twice as fast as BT or BT’s wholesale customers and about four times faster than ISPs using unbundled local loop access.

No comments:

Post a Comment