For the foreseeable future, net changes in telco revenue can happen only at the margin. Over the next decade, mobile operators, for example, will replace half their 4G accounts by 5G accounts. So the issue is whether average revenue per account stays the same; increases or decreases.

Assuming at least a stable ARPA, the balance of revenue changes will come in fixed network services. And there the issue is whether new revenue sources offset expected losses in consumer and business service revenue.

Keep in mind that revenue-neutral product replacement is necessary, but will not help telcos grow total revenues. Product replacements only swap legacy revenue for new sources, as in the example of 4G accounts being replaced by 5G accounts.

All things equal (operating costs; marketing costs; capital investment; revenue per account), swapping 5G for 4G results in zero net revenue gain. All revenue growth beyond zero must come in other areas.

On a global level, revenues appear flat. But revenue contributors change substantially every decade. In fact, telcos routinely lose half of present revenues every decade. That seems unthinkable, but has happened.

“Over the last 16 years we have grown from approximately 25 million customers using wireless almost exclusively for voice services to more than 110 million customers using wireless for mostly data services,” said Lowell McAdam, former Verizon Communications CEO.

It is an illustrative comment for several reasons. It illustrates Verizon’s transformation from a fixed network services company to a mobile company. But the comment also illustrates an important business model trend, notably that of firms in telecom needing to replace about half their current revenues every 10 years or so.

In the U.S. telecom business, for example, we already have seen that roughly half of all present revenue sources disappear, and must be replaced, about every decade.

According to the Federal Communications Commission data on end-user revenues earned by telephone companies, that certainly is the case.

In 1997 about 16 percent of revenues came from mobility services. In 2007, more than 49 percent of end user revenue came from mobility services, according to Federal Communications Commission data.

Likewise, in 1997 more than 47 percent of revenue came from long distance services. In 2007 just 18 percent of end user revenues came from long distance.

Though revenue attrition has been clearest for fixed network voice, the same process has been seen for mobile voice, text messaging, long distance revenues, mobile roaming and business customer revenues overall, in many markets.

We can disagree about how much new revenue some communications service providers will have to create over a decade’s time, to replace lost legacy revenues.

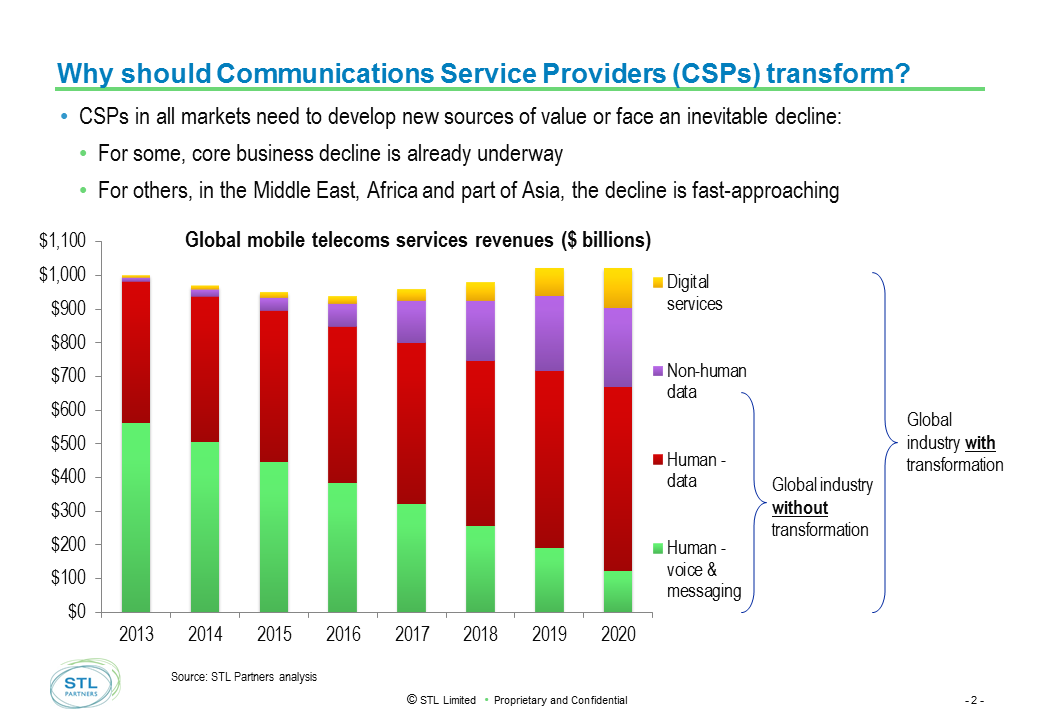

If global telecom revenue is about $1.6 trillion to $2 trillion, and assuming about half the revenue is earned in mature markets, then the revenue subject to disruption ranges from $800 billion to $1 trillion.

Half of that represents $400 billion to $500 billion. That, hypothetically, is the potential amount of global revenue that might be lost, and would have to be replaced. The good news is that most of the replacement will come as 5G displaces 4G subscriptions.

What is equally certain is that a huge amount of revenue from new services will be necessary, even if consumer purchases of Internet access--and replacement of 4G by 5G--happens.

One fundamental rule of thumb is that, in mature markets, service providers must plan for a loss of about half of current revenue every decade or so. That might seem shocking, but simply reflects historical developments.

Nor is that rate of change unusual. In the digital consumer electronics business, it might not be unusual for an executive to predict that half the products that drive sales volume in 10 years “have not been invented yet.”

What is new for the telecommunication business is that product replacement now is a fundamental issue, even if for 150 years the only product was voice.

In 2001, in the U.S. market, for example, about 65 percent of total consumer end user spending for all things related to communications and video services went to "voice."

By 2011, voice represented only about 28 percent of total consumer end user spending.

Over that same period, mobile spending grew from about 25 percent to about 48 percent. Again, you see the pattern: growth of about 100 percent (losses of 50 percent require gains of 100 percent, to return to an original level, as equity traders will tell you).

Video entertainment spending likewise doubled.

In the U.S. market, one can note roughly the same pattern for long distance and mobile services revenue. Basically,mobile replaced long distance revenue over roughly a decade.

At one time, international long distance was the highest-margin product, followed by domestic long distance.

That changed fundamentally between 1997 and 2007.

Over that 10-year period, long distance, which represented nearly half of all revenue, was displaced by mobile voice services.

In the next displacement, broadband is going to displace voice.

That is not yet an issue in some regions that still are adding mobile and fixed network subscribers, but already is an issue in most developed regions, where voice and messaging revenues already are declining.

Though some might continue to hope that higher Internet access revenues will offset voice and messaging revenue dips, the magnitude of voice revenue declines will be so sharp that in many markets, even additional Internet access revenues will be insufficient in that regard.

In fact, rates of revenue growth have been dropping in all regions since at least 2005, according to IBM.

At least so far, ability to fuel growth by extending service to customers with low average revenue per user will continue to drive revenue growth, even for legacy services, for a while. The only issue is when saturation is reached in each particular market.

When that happens, the same pressure on voice and messaging revenue already seen in mature markets will be seen in presently-growing markets.

Those changes can be hard to discern, as the top line obscures changes in revenue contribution from the largest sources. Voice, messaging and long distance services have fallen dramatically. Consumer fixed network usage of voice no longer drives financial results, its place taken by internet access (broadband).

Mobility now drives growth in most markets, and especially the data services component of mobile revenues. Subscription growth still is highly meaningingful in developing Asia and Africa.

source: Delta Partners

Basically, 5G mostly prevents telco revenue from declining. It does not drive revenue growth. If we expect continued declines in fixed network voice, then broadband and other new services will have to be relied on for most of the growth, in most markets, by most operators.

The lucky scenarios will happen when mobile-first operators actually are able to drive higher ARPA in the 5G era.