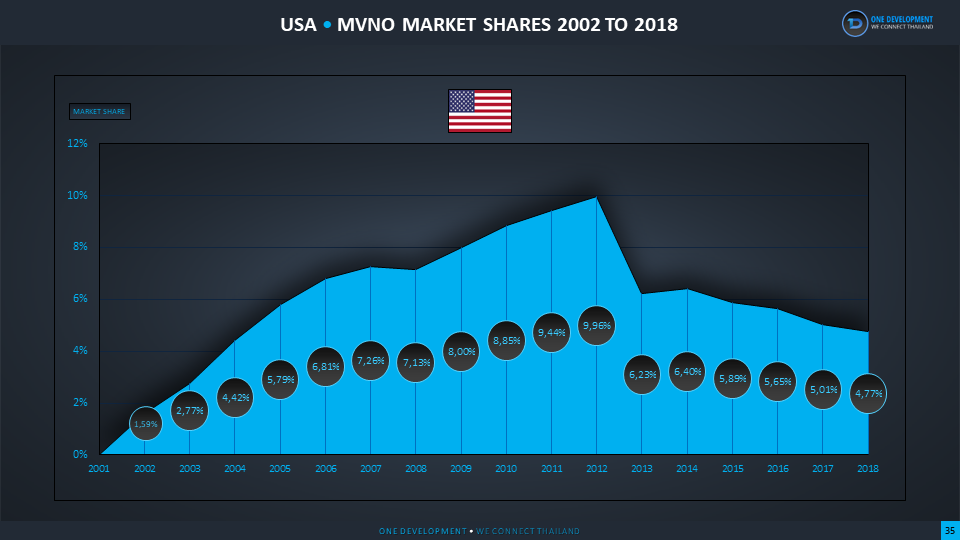

The U.S. market share (net new additions) and installed base held by mobile virtual network operators is headed for big change. More share is shifting to facilities-based providers. At the same time, new entrants using the MVNO model will eventually shift to facilities-based competition over time.

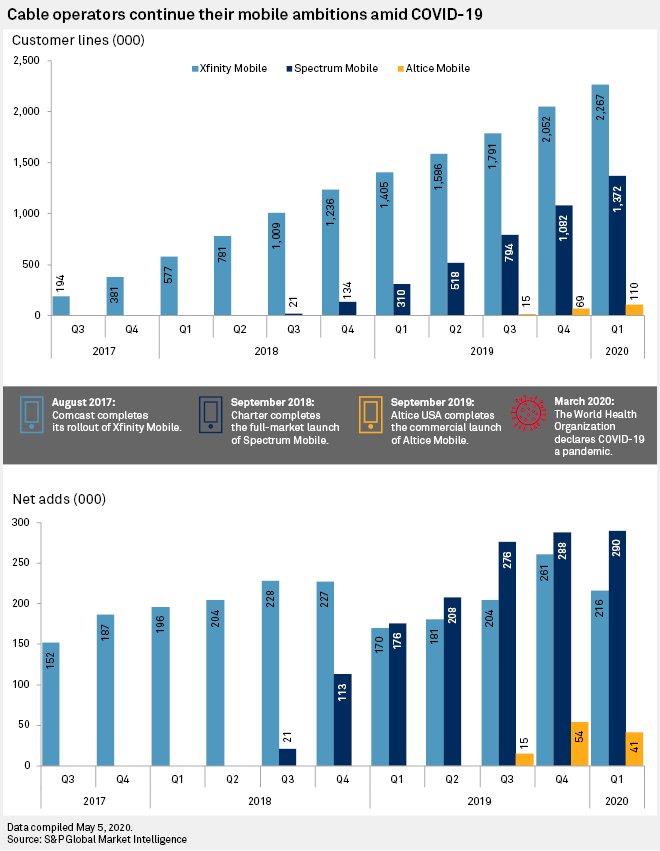

The important new market entrants include the biggest U.S. cable operators and Dish Network. All presently operate as MVNOs, but Dish already is building its own national network, and cable operators will shift partially to their own facilities over the next few years.

Also, Verizon recently made a big move into the MVNO space as a retailer, acquiring Tracfone, while the other leading national mobile service providers operate substantial “virtual MVNOs” under various brand names, offering more-affordable service under the subsidiary brands as a way of protecting prices on their core brands.

Sometimes, as an industry researcher, one reaches conclusions that are distasteful for suppliers. On one consulting engagement, a supplier that said it “could not” eliminate its dividend eventually wound up doing precisely that, before exiting the market entirely by sale.

Another time, arguing that more share would shift over time to facilities-based strategies, the owner of an MVNO said “you just told me my business is toast.” The answer actually is more complicated than that, as given the availability of capital, a firm always can gain share by acquiring assets.

Over a longer period of time, though, it might still be the case that more share and installed base will be gained by facilities-based providers, even if a few MVNOs can grow, for a time, through acquisition.

As many of us discovered during the very-late 20th century and very-early 21st century, acquired MVNO or other non-facilities-based accounts are highly unstable. I once asked a service provider what percentage of accounts gained by acquisition just six months ago were still customers of the acquiring company. “None” was the answer.

The point is simply that connectivity markets consolidate over time, no matter the segment. There always are specialty segments that can thrive for a time. What seems never to be the case is that they remain viable over the long term. That does not mean they go bankrupt. It does mean those assets eventually are sold, and perhaps sold again, winding up on the books of a facilities-based supplier.

That already is happening in the U.S. mobile market.

No comments:

Post a Comment