It is impossible to minimize the strategic importance of mobility as a driver of global connectivity revenues. And it might already to argue that the next big wave of revenue growth is going to come from investments related to cloud computing, edge computing and content delivery, one way or the other.

Simply put, most of the revenue, and most of the revenue growth, now come from mobile connectivity services. Something else eventually will emerge to drive revenue growth, and consultants at EY suggest the outlines of where the expected growth will come from.

For all the justifiable importance of optical fiber access in telco networks, it is possible to make the argument that fiber-to-home investments will be relatively muted, globally, as priorities continue to shift elsewhere. The simple observation is that most of today’s revenue is earned on the mobile network, not the fixed network, and that tomorrow’s revenue might well be earned elsewhere than from mobile connectivity itself.

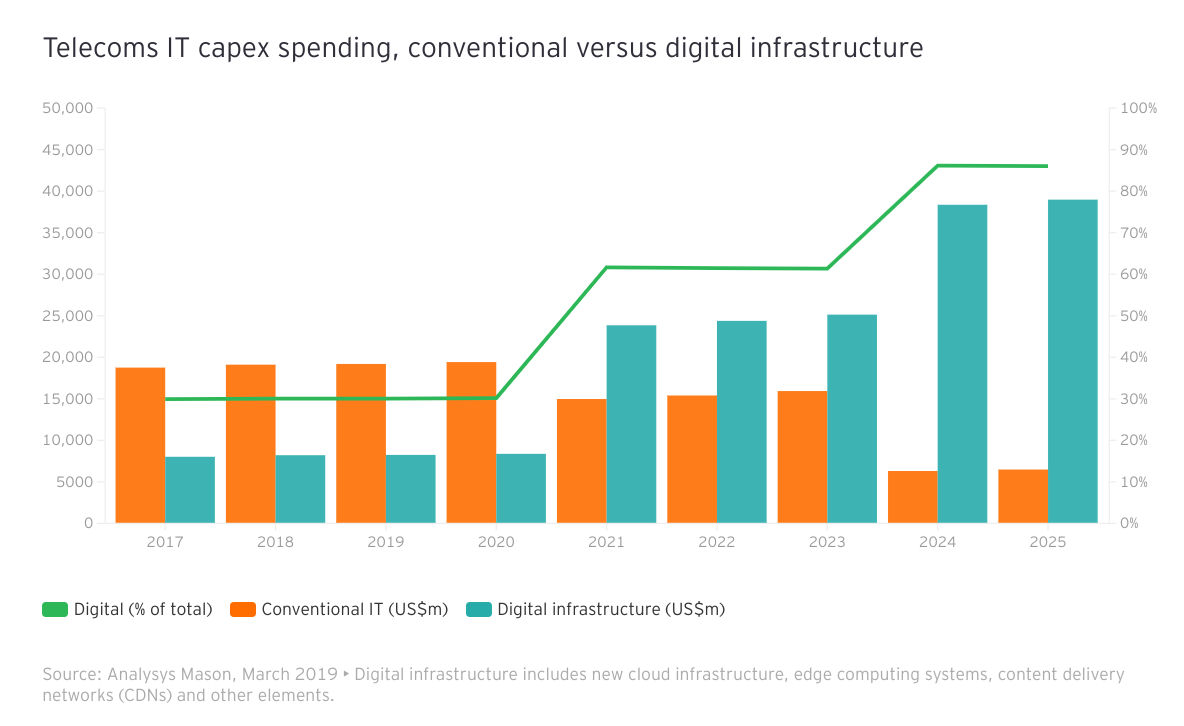

Assume this EY forecast of telco capital investment is correct. Assume the orange bars include local access network capex (mobile and fixed), while the green bars are investments to support edge computing, cloud infrastructure or content delivery networks. The EY forecast suggests that investments in the access network are going to drop, to support other initiatives.

In part, one might argue that access capex will drop because some big 5G builds will be tapering off, allowing more investment in complementary assets (edge computing, content delivery infrastructure, analytics and other investments) to support new revenue opportunities.

The EY forecast likely includes both fixed and mobile network capex, plus support for any related businesses telcos might be in (data centers, for example), plus the other investments in information technology telcos make (buildings, rolling stock, computing infrastructure not directly related to the network).

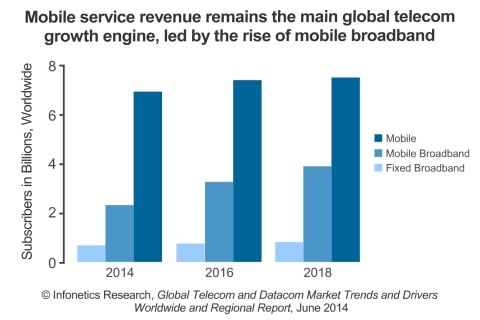

Still, mobile capex tends to dominate global telco capex, as this forecast by Infonetics suggests. Virtually all fixed network investment these days is for broadband, as voice and other services simply are carried over the broadband infrastructure, while investments to support voice are nil.

In fact, fixed network capex has dropped dramatically since about 2000.

That capex profile parallels the revenue generation profile for telcos globally, where almost all the revenue growth comes from mobility and mobile broadband, compared to fixed network broadband and voice.

And one implication of the limited capex for fixed networks is that there is probably not going to be much expansion of current modernization efforts (replacing copper with optical fiber to the premises).

That is especially the case if one assumes that overall capex climbs dramatically, as the EY analysis suggests.

No comments:

Post a Comment