Verizon now says its fixed wireless offer will be available in all 30 markets nationally where Verizon is introducing its mobile 5G service. “You should expect that every market that opens a 5G Mobility market will in due course be a 5G fixed wireless because it is one network,” said Ronan Dunne, Verizon Communication EVP.

And then we will see whether forecasts of significant adoption are proven correct. The question is whether fixed wireless might eventually represent 15 percent to 20 percent of active subscriptions supplied by fixed network ISPs, a figure some have suggested is a possibility.

That is deemed implausible by some. Maybe not. A significant role for fixed wireless is more likely if the actual universe of fixed network accounts is smaller than generally assumed.

By some estimates had U.S. fixed network broadband accounts were as high as 110 million in 2017. Other estimates peg the number of connected locations at about 100 million. By other estimates, there are a total of about 97 million U.S. internet access connections supplied by fixed networks (not including mobile internet access connections to phones and other devices).

Those figures appear to include business broadband accounts as well as consumer accounts, however. On the other hand, it is possible that business use of fixed wireless might grow the addressable market to the extent that fixed wireless is viewed as a suitable backup service. AT&T, in fact, has been marketing its 5G fixed wireless service exclusively to business customers, who do seem to use it as a backup to their fixed access connection.

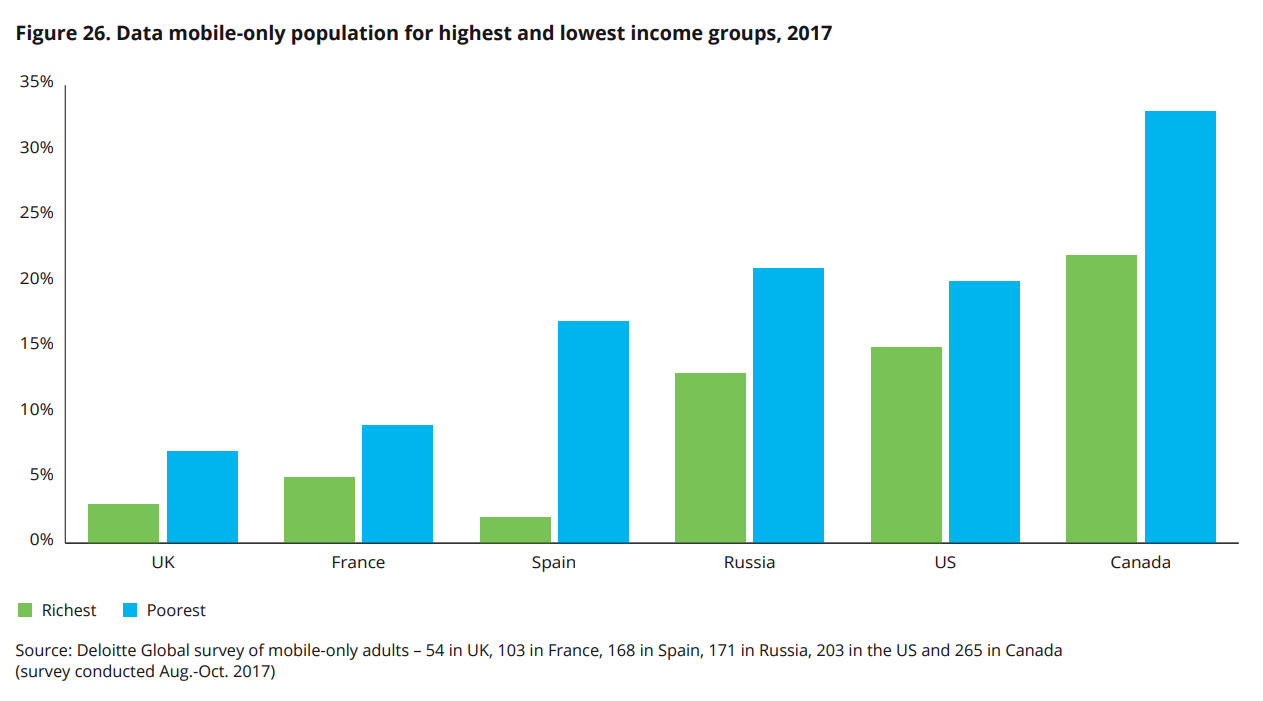

The potential universe for consumer fixed network internet might be smaller than often assumed. Some households do not wish to buy the service. Estimates by Pew Research suggest only 89 percent of U.S. residents use the internet at all.

And mobile substitution is a growing reality for 15 percent to 20 percent of U.S. households, according to Deloitte. The point is that the total addressable market for fixed network internet access might be as small as 82 million homes or as large as 88 million.

No all housing units are occupied. Vacancy rates can range from more than one percent for owned housing and up to seven percent for rental units. Some “homes” are not used all year, as a matter of course.

U.S. housing locations number somewhere between 129 million and perhaps 135 million. In 2014 the U.S. Census Bureau estimated housing units at a bit over 133 million, so the 135 million estimate seems reasonable.

Assume 10 percent of locations choose not to buy fixed network internet access because they do not use the internet. That suggests the addressable market is 121.5 million locations.

And perhaps 10 percent of U.S. homes use the internet, but exclusively from a mobile device. Remove the mobile-only households and 13.5 million more units get removed from the potential universe of buyers, reducing the market to a potential of about 108 locations.

But also keep in mind that some units are rooms in houses, boats, mobile homes or other units possibly not suitable for fixed internet access. Mobile homes represent about 6.4 percent of housing locations. About three percent of people live in group quarters, vans, RVs, and boats, according to 2014 U.S. Census Bureau data. So remove another six percent of locations from the addressable universe. That subtracts about eight million more locations, for a total addressable market of 100 residential locations.

If fixed wireless might eventually represent 15 percent to 20 percent of active subscriptions supplied by fixed network ISPs, and the addressable market is 15 million to 20 million locations, then fixed wireless could grab 15 percent to 20 percent market share.

Skeptics say Verizon’s fixed wireless effort so far is quite miniscule. True, but it is worth remembering that Verizon has deliberately chosen to restrict its roll-out, partly for marketing reasons (it wants to test demand), partly for technology reasons (it is waiting for full standards-based customer premises equipment and network gear), partly for operational reasons (Verizon will deploy, logically, where it faces the greatest capacity demand, and that typically is urban core areas, not suburban areas where many homes are located).

Also, Verizon’s use of millimeter wave spectrum for mass market services is quite novel. As with any radically-new technology, there is a learning curve.

So the spotty coverage is not too surprising. The careful roll-out is not unusual. And Verizon is coming up the learning curve. The early deployments of fixed wireless were careful and over-engineered, with install costs too high to sustain as a mass market service, using pre-standard, almost custom network elements.

But what has Verizon learned? Where it had to install external antennas early on, it now finds that “almost 80 percent of the antenna are indoors rather than outdoors,” said Dunne. “And that's critical for them, the ability to self-provision.” Install costs will plummet, as a result.

The early customer premises equipment was essentially using a cellphone chipset with low power output. The production-level gear now coming uses higher-power chipsets, available in the first half of 2020, will feature higher-power, meaning easier self-installs in a wider range of settings where the low-power gear might have encountered issues.

“We're building a mobility network that enables a 5G residential (fixed) offering, we're now in a position where we can lean into that,” said Dunne. The fixed wireless network, in other words, is not an overlay network on the 5G mobility platform, but part of it. And that also will help manage costs as the fixed internet access service becomes a mass market offering.

No comments:

Post a Comment