India’s mobile and telecom business is not immune from challenges facing other service providers in global markets, with traditional revenue streams maturing and new revenue sources therefore needed to fuel the next era of growth, a report by KPMG argues.

Voice revenues have been the mainstay of India telecom, but in 2018 voice revenue dropped 30 percent. In 2019, voice revenue is expected to drop another 15 percent to 20 percent. Not even growing subscription volumes are going to compensate for those revenue declines.

In 2019, industry revenue is forecast to drop about nine percent, according to Deutsche Bank researchers.

KPMG analysts therefore argue that India’s mobile industry has to earn revenues from value, services, apps and use cases beyond connectivity, advice universally applicable globally as well, GSMA argues. The whole industry has to move beyond connectivity to really profit from internet of things opportunities, for example, says GSMA.

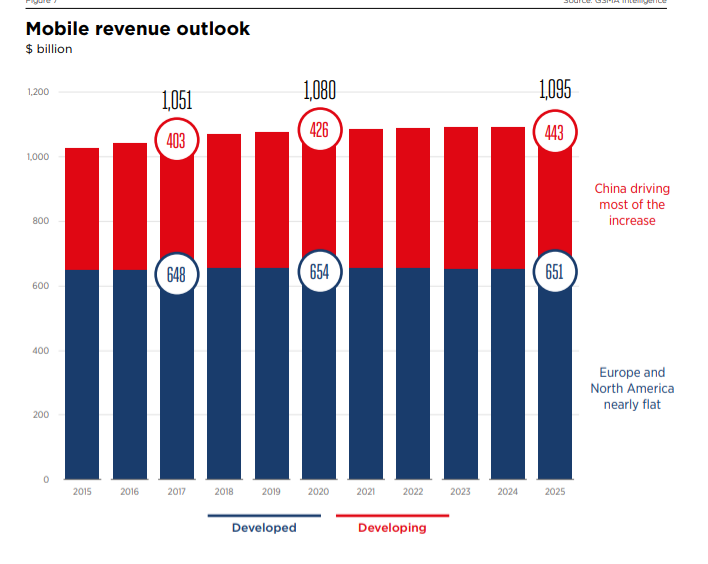

Global mobile revenue will be pretty close to flat through 2025, GSMA predicts.

Of course, the issue is what, precisely, mobile operators can do to become more-effective digital enablers (acting as platforms) or actual providers of services and apps. Equally important is how mobile service provider revenue is increased by any of those new roles.

One might well argue that much of the value of a mobile operator comes from being the enabler of internet apps and services provided by all other third parties. In addition, the mobile operator is itself the provider of some revenue-generating apps (carrier voice, carrier messaging, carrier video subscription services).

The obvious problem is that a couple of those sources are shrinking, in most markets, and for most service providers. Carrier video entertainment, on the other hand, is a growth opportunity for some.

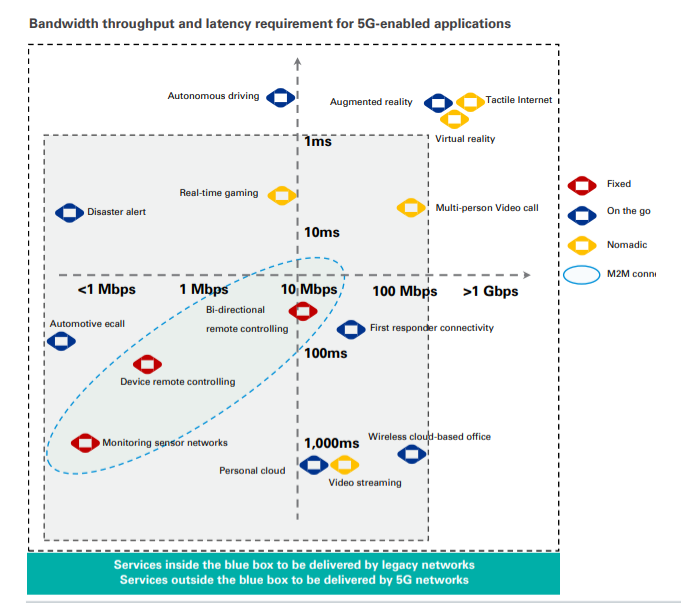

But most of the upside from 5G is going to come from enterprise apps related to internet of things, KPMG says. At this point, ultra-low latency or battery life might be more important than bandwidth as an enabler of new use cases.

To be sure, connectivity services are the distinct role connectivity providers play in the internet ecosystem. But telcos, cable companies and other internet service providers are not the only logical or potential suppliers of connectivity. Nor will most providers be able to sustain themselves on the strength of connectivity subscriptions alone.

As hard as it always is, connectivity providers are likely to have to consider taking on new roles in the ecosystem. It might once have been unthinkable for mobile operators to act as subscription video providers, autonomous vehicle platforms or drone platforms. But such initiatives--as hard as they might be--are going to be explored as connectivity business expands beyond “access” and moves into new applications, KPMG suggests.

No comments:

Post a Comment