Not so long ago, knowledgeable executives in the cable TV and telecom industries doubted the level of consumer demand for gigabit internet access, especially when tariffs were in triple digits.

Of course, with the coming of 5G, gigabit access for every device on the network will be a key design goal. And even if actual end user experience often is in the hundreds of megabits per second range on the move (gigabit will tend to be available in urban areas),

Randall Stephenson, AT&T Chairman and CEO, now says the company is “laser-focused in 2018 on building the world's premier gigabit network.”

Some might have doubted--given the capital investment--the ability to do so, as some now question the cost to build gigabit 5G networks.

But the business context has changed. Cost curves for gigabit networks have bent lower. Retail tariffs for gigabit service have dropped by an order of magnitude. And even when most customers do not buy the headline gigabit services, they are upgrading to faster intermediate tiers of service in the hundreds of gigabits per second ranges.

Fiber to home costs, though declining a bit, are not the key change. What has changed is regulator acceptance of the idea that gigabit networks can be built in areas where there is demand, without requiring universal builds at that level.

Also, even when new competitors do not take more than five percent to 20 percent market share in entire markets, those new competitors recreate consumer expectations, driving end user demand for higher-speed services at new price points.

That “build in response to demand” pattern has been a fixture of U.S. telecommunications since the passage of the Telecommunications Act of 1996, allowing competitors for the first time to operate and build their own networks.

The ability to use other platforms--5G fixed wireless, mobile 5G; other forms of wireless or untethered access in combination with mobile access--also promises lower costs. Eventually, many believe, wireless and mobile networks will even rival fixed networks in terms of performance and retail price.

On the other hand, it would be appropriate to note that the move to gigabit networks is only the foundation, not the goal. For AT&T, in its consumer fixed networks business, internet access by itself does not drive overwhelming amounts of revenue.

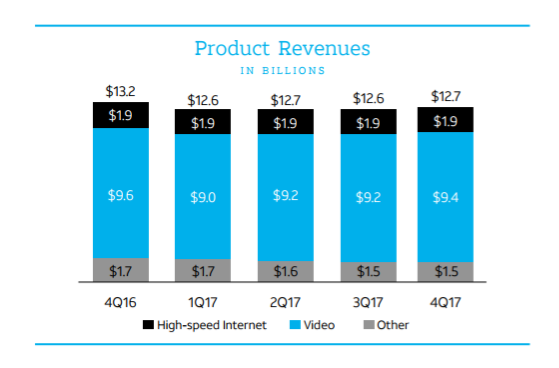

One takeaway from AT&T’s fourth quarter 2017 results is the importance of video entertainment, compared to internet access and voice as revenue drivers in the consumer segment of the fixed network business. Consider the wide gulf between U.S. video entertainment, internet access and other revenues: video drove 74 percent of fixed network consumer revenues.

Internet access represented just 15 percent of total, while the “other” category generated about 12 percent of total revenues.

One way of describing those results is to note that internet access is a “dumb pipe” service. Both voice and video entertainment are “apps.” So AT&T, in its fourth quarter, generated 85 percent of its consumer fixed network revenues from “apps” and only 15 percent from dumb pipe internet access.

That, in turn, illustrates why AT&T will look to applications, services and maybe platforms as it grows its internet of things and 5G businesses. Ignoring profit margin for the moment, apps and services are where the money is.

No comments:

Post a Comment