The race for 5G bragging rights now includes Sprint, which argues it will have the first mobile 5G network up and running in the first half of 2019, obviously also with at least some phones able to use the network.

“We're working with Qualcomm, and network and device manufacturers in order to launch the first truly mobile (5G) network in the United States by the first half of 2019,” says Sprint CEO Marcelo Claure.

T-Mobile US has argued it will launch the first U.S. 5G mobile network in 2020. AT&T and Verizon plan 2018 launches of fixed 5G.

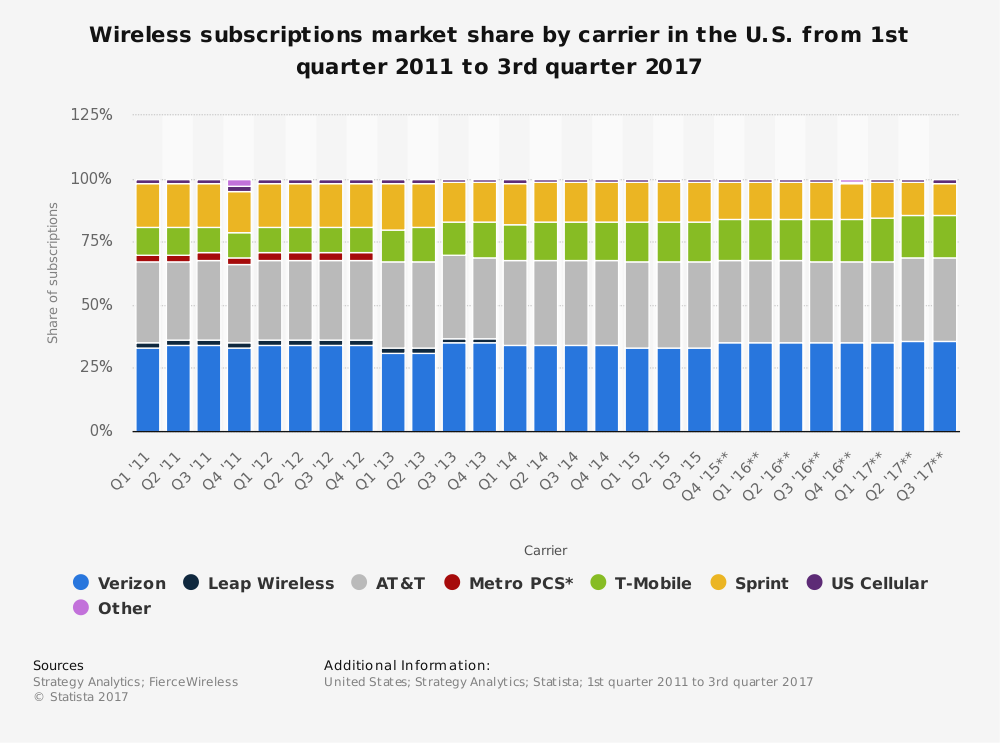

It remains to be seen what longer-term advantages might be reaped by early 5G launches. U.S. mobile operator market share is remarkably consistent. With churn rates down around one percent for most of the leaders, very little share can be taken from other providers.

Company assessment of assets, growth opportunities and weaknesses drive the different approaches. Sprint has lots of fallow 2.5-GHz spectrum that can be used to create a new 5G network largely from existing tower locations. Sprint also does not own a fixed network of its own that can be leveraged to support small cells.

T-Mobile likewise has much 600-MHz spectrum that likewise can be deployed from existing tower locations, and, like Sprint, T-Mobile US does not have fixed network assets to leverage for small cell backhaul.

Verizon, on the other hand, has a trove of 28-GHz millimeter wave spectrum to deploy, and has some fixed network infrastructure to leverage for backhaul, both inside and outside its traditional geographic footprint (its own facilities in the Northeast, XO Communications assets outside that footprint.

That means Verizon has more to gain from small cell deployments, which in turn suggest the strategy of taking market share away from other fixed network internet access providers.

AT&T has the biggest U.S. fixed network footprint, and therefore the greatest leverage where it comes to building small cell networks. Like Verizon, AT&T owns millimeter wave licenses that will require small cells.

As a marketing challenge, selling fixed 5G, where small cells are available, will be easier than marketing 5G everywhere, in the early deployments. It will be easier to target fixed wireless advertising, for example, than it would be to control advertising for a 5G network whose coverage initially is limited.

That is a historic problem when next-generation networks are built. It is hard to match media marketing to the actual current extent of the network (which neighborhoods can buy, and which cannot).

No comments:

Post a Comment