Telecom now is a leaky bucket: new revenues are filling the bucket, but the bucket has holes. Those holes are declining voice and messaging revenues. In some markets, entertainment video and even internet access revenues also are mature, and face declines.

So one clear strategic issue is how to maintain the revenue fill rate into the top of the bucket at a level that more than compensates for what is leaking out the bottom of the bucket.

The big problem is that there is little present evidence that the fill rate is going to match the leak rate globally, despite continued growth in Asia and Africa.

Most observers of global telecom revenue will note that, with a couple of possible exceptions, industry revenue has grown continuously, for as long as we have kept records.

So one clear strategic issue is how to maintain the revenue fill rate into the top of the bucket at a level that more than compensates for what is leaking out the bottom of the bucket.

The big problem is that there is little present evidence that the fill rate is going to match the leak rate globally, despite continued growth in Asia and Africa.

Most observers of global telecom revenue will note that, with a couple of possible exceptions, industry revenue has grown continuously, for as long as we have kept records.

On the other hand, one has to wonder whether telecom revenue will reach a peak at some point in the relatively-near future, as mobile adoption reaches saturation in every country and as every customer buys as much internet access as they prefer.

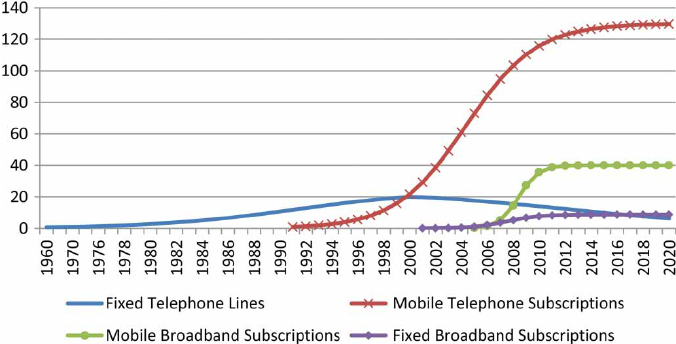

Looking only at the country of Malaysia, the trends are clear enough: Mobile growth is reaching an absolute peak, as is mobile broadband. Fixed line voice is declining, and has been dropping since about 2000, while fixed network internet access has grown to replace the lost fixed network revenue, but itself is nearly saturated.

That does not mean service providers will stop innovating--or trying to do so--or seeking to add big new revenue sources. But that new revenue will mostly balance lost revenues in the core business, as voice, messaging and eventually, even internet access revenues fall.

Indeed, replacing lost revenue now is a major industry challenge. The global telecom industry is about a $1.5 trillion annual revenues industry. To move the needle, any new sources have to be large, simply to replace lost revenues from legacy sources.

Roughly speaking, to sustain three percent annual revenue growth, and assuming zero losses in all legacy sources, some $45 billion has to be added every year. But that is not realistic. With actual declines in voice and messaging revenue, and coming shrinkage and margin compression in newer sources such as internet access or video entertainment, service providers might have to replace as much as half of all current revenue in about a decade.

Revenue erosion big enough to remove half of revenue within a decade is roughly equivalent to a seven percent a year decline. So even if new sources grow three percent a year, losses still will happen.

To sustain revenues at their current level might therefore require annual growth of seven percent. That is not going to happen, in most markets. As James Sullivan, J.P. Morgan head of Asia equity research (all of Asia except Japan) telecom revenue growth is now less than GDP growth.

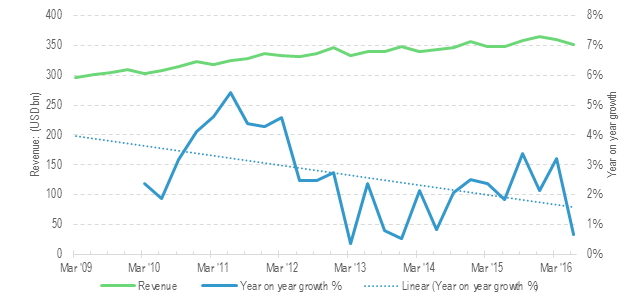

68 major telecoms groups – aggregate revenue, 2009-2016

Other analysts make the same argument, namely that revenue growth, at a global level, now is less than one percent.

Peak telecom is coming.

No comments:

Post a Comment