Though much remains to be determined, it is at least possible that new thinking about the role of a fixed network; the role of media in the access network and the capital investment to support gigabit internet access will revolutionize traditional thinking about the cost of broadband access networks in the U.S. market, and possibly others.

Originally, telco and internet service provider thinking about fiber to the home investments was that this was the “best” way to create a ubiquitous, high-bandwidth, future-proof consumer access capability, even as continuous investments have been made to digital subscriber line platforms.

Cable TV operators, using a different access platform, have deployed trunking fiber deeper into the network as well, but to neighborhoods containing triple-digit homes.

While both telcos and cable TV operators have been able to use “fiber to the neighborhood” designs, cable has wrung much more advantage from its designs, than have telcos. AT&T’s “U-verse,” for example, has not had the marketplace success of hybrid fiber coax running DOCSIS 3.1.

Nor has the telco “fiber to neighborhood” design been able to keep pace, in terms of internet access speeds.

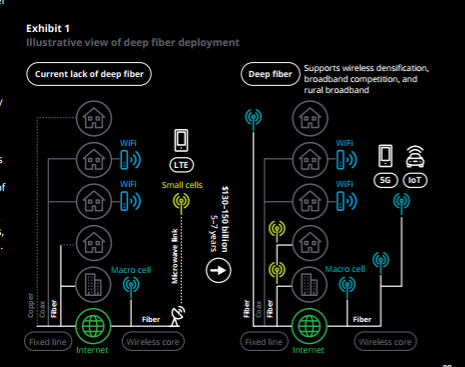

In the 5G era, it appears that the role and value of the trunking network is anchored by mobile backhaul, namely the creation of a dense small cell network. That is different.

In the new thinking, the fiber deep network is “primarily” driven by the need to support fiber deep trunking to dense small cell networks. Just how dense remains an issue, but Verizon, at least, is thinking of fiber to about every other light pole, as an example.

The new fiber deep network--designed to support the small cell network--also has other strategic advantages, though. As Verizon sees matters, using high fiber count cables, the same physical media can support enterprise and smaller business connections.

Also, with a fiber deep network reaching literally “to the light pole,” fixed 5G becomes feasible, allowing Verizon to provider gigabit internet access to consumers, instead of building a fiber-to-home network.

The big strategic advantage is that fiber deep networks potentially change the economics of access network upgrades.

By some estimates, as much as $130 billion to $150 billion in additional optical fiber deployment in the access and distribution networks to support U.S. 5G and allow telcos to compete with cable TV operators, over the next five to seven years.

Some of us doubt that will wind up being the case, at least not over the five to seven year timeframe. There are several reasons. First, and most compellingly, there are rival strategic claims on available capital.

Service providers also must make strategic acquisitions to gain scale and also move up the stack into the applications and platform spaces. Tier one providers that have made big acquisitions have to pay down debt from making those deals.

Stranded assets are another issue. In the facilities-based U.S. market, any tier-one fixed network service provider has to expect to strand at least 50 percent of newly-deployed access assets. No rational executive is going to invest billions, or scores of billions, knowing that half those assets will not generate revenue.

Consider “where” new optical infrastructure is called for, according to Deloitte.

According to Deloitte, $15 billion to $20 billion is required to support densification of the mobile networks (5G small cells).

Some $35 billion to $40 billion is needed to connect rural residents. About $60 billion to $100 billion is needed to bring fiber-to-home networks or other gigabit internet access speeds to residences.

Some might argue that the capital to support mobile network densification ($15 billion to $20 billion) is essential and affordable.

What is questionable, given the opportunity to use 5G-based fixed wireless, is the $60 billion to $100 billion in fiber to home, where half the investment will be stranded, and not generate revenue. This bucket of spending is questionable.

The $35 billion to $40 billion to support rural internet access likely will prove amenable to other solutions than fiber to the home, namely wireless in several forms, or mobile networks, using fiber trunking but not fiber to the home.

The point is that huge amounts of capital will be needed to make strategic acquisitions for scale; others for scope (moving up the stack); to pay down debt and then to invest in access networks and spectrum.

Under such conditions, no rational executive is going to strand so much capital in the access network. For that reason, one might argue that the $130 billion to $150 billion investment over five to seven years is too high. Faster speeds (hundreds of megabits to gigabits per second) can be supplied in other ways that are far more capital efficient.

No comments:

Post a Comment