It sometimes is difficult to comprehend just how much mobile spectrum (capacity) supply will change as millimeter wave assets are made available and small cell architectures are deployed. Historically, both smaller cell sizes and additional spectrum have been the principal ways mobile operators have added spectrum.

In addition to those tools, aggregation of licensed and unlicensed spectrum, plus huge amounts of new spectrum, are going to upend business models.

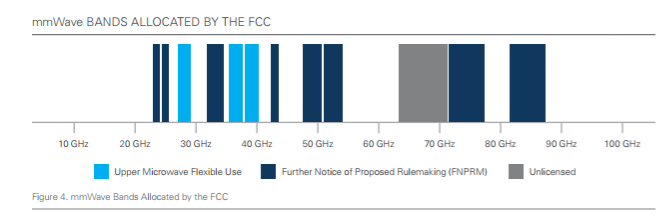

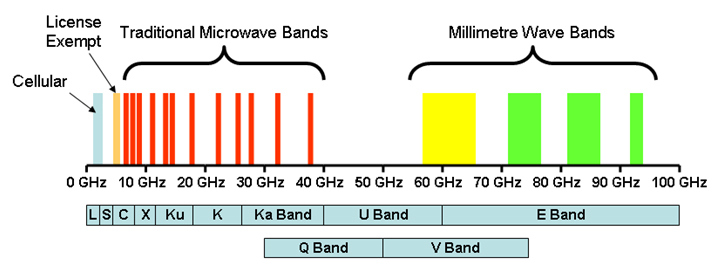

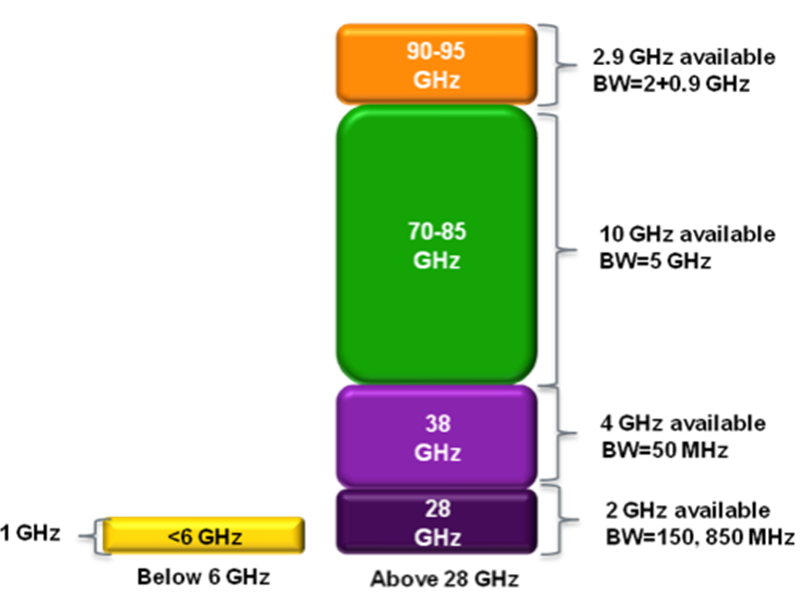

Consider that, in the U.S. market, the Federal Communications is releasing 11 GHz of new spectrum for mobile communications, with a total of possibly 24 GHz of new millimeter assets.

By way of contrast, licensed U.S. mobile spectrum amounts to 587 MHz, total, for the top four U.S. mobile firms.

So, in the near term, about 19 times more spectrum is going to be released, than is now in service industrywide. Longer term, as much as 41 times more spectrum could be available.

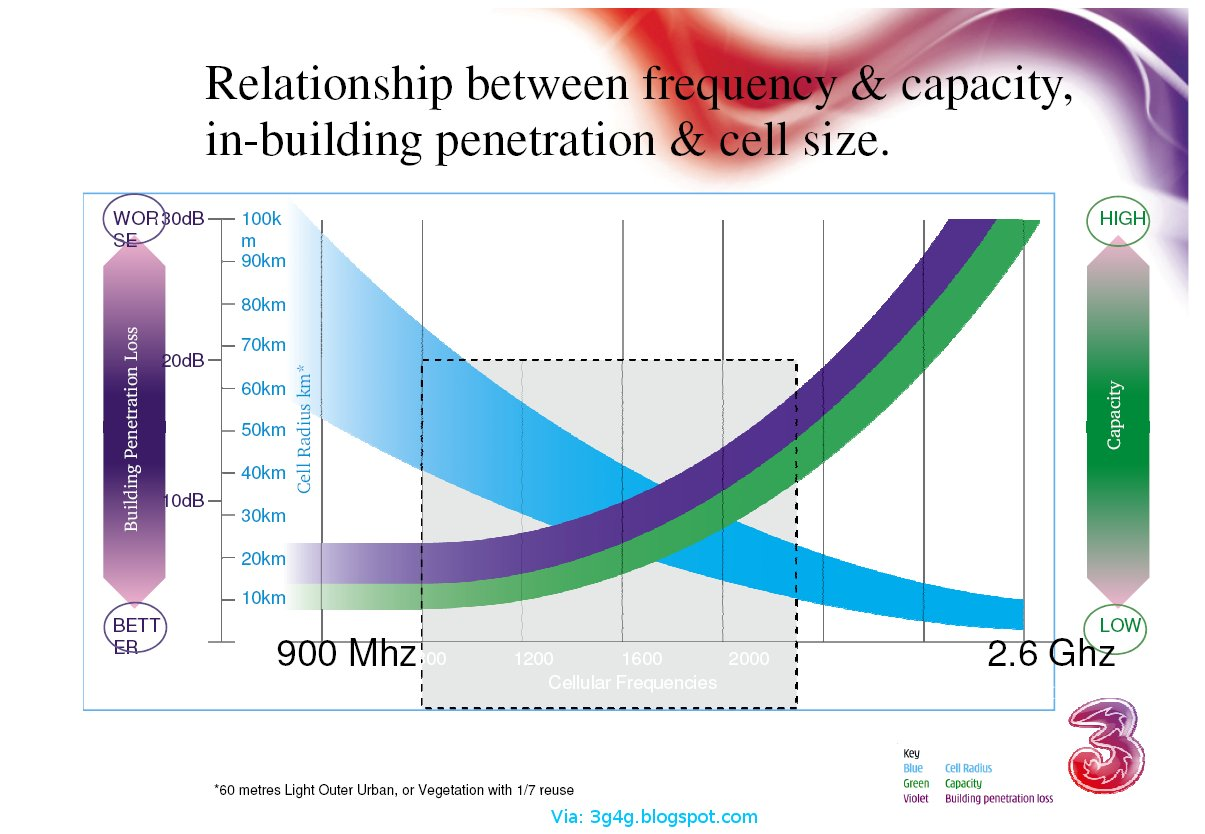

But that is just the physical spectrum. Higher-frequencies are capable of higher bandwidth. Data throughput at millimeter frequencies is between an order of magnitude to two or more orders of magnitude greater than mobile throughput at UHF frequencies below 1 GHz.

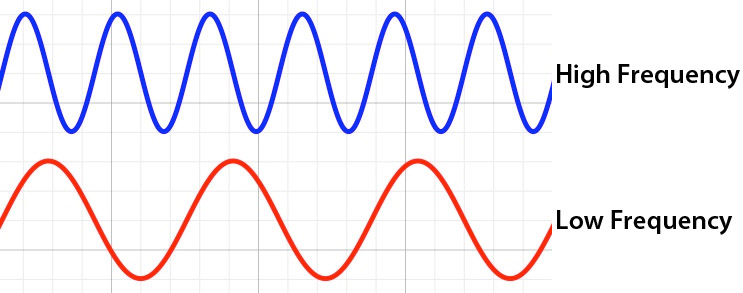

The reason is that frequency is directly related to the number of potential symbol representations. In other words, the ability to modulate bits (ones and zeros), in a physical sense, hinges on the number of times per second a waveform crosses the zero point, with the “high state” representing a “one,” for example, and the “low state” representing a “zero.”

Higher-order modulation is possible, but still is based on the physical number of waveform oscillations per second.

In principle, the more oscillations in any unit of time, the greater the number of symbols that can be coded in any single unit of time.

The point is that all our current business model assumptions will change dramatically. “Who” can use spectrum; what spectrum costs; how networks are built; where facilities are located; when infrastructure has to be deployed, by whom, will change.

In the future, especially with the ability to use protocols completely in unlicensed spectrum, the greater amount of unlicensed and shared spectrum, ownership of licensed spectrum will not provide the “moat” preventing market entry by new access providers.

The cost of licensed spectrum also should fall, with greater supply. And, to an extent not yet seen, application and product suppliers, plus competitive access suppliers, will be able to build and operate their own networks.

No comments:

Post a Comment