As a practical matter, policy debates about how to sustain competition in the mobility business while also sustaining the supply of services often focuses on whether the number of suppliers should be consolidated from four to three.

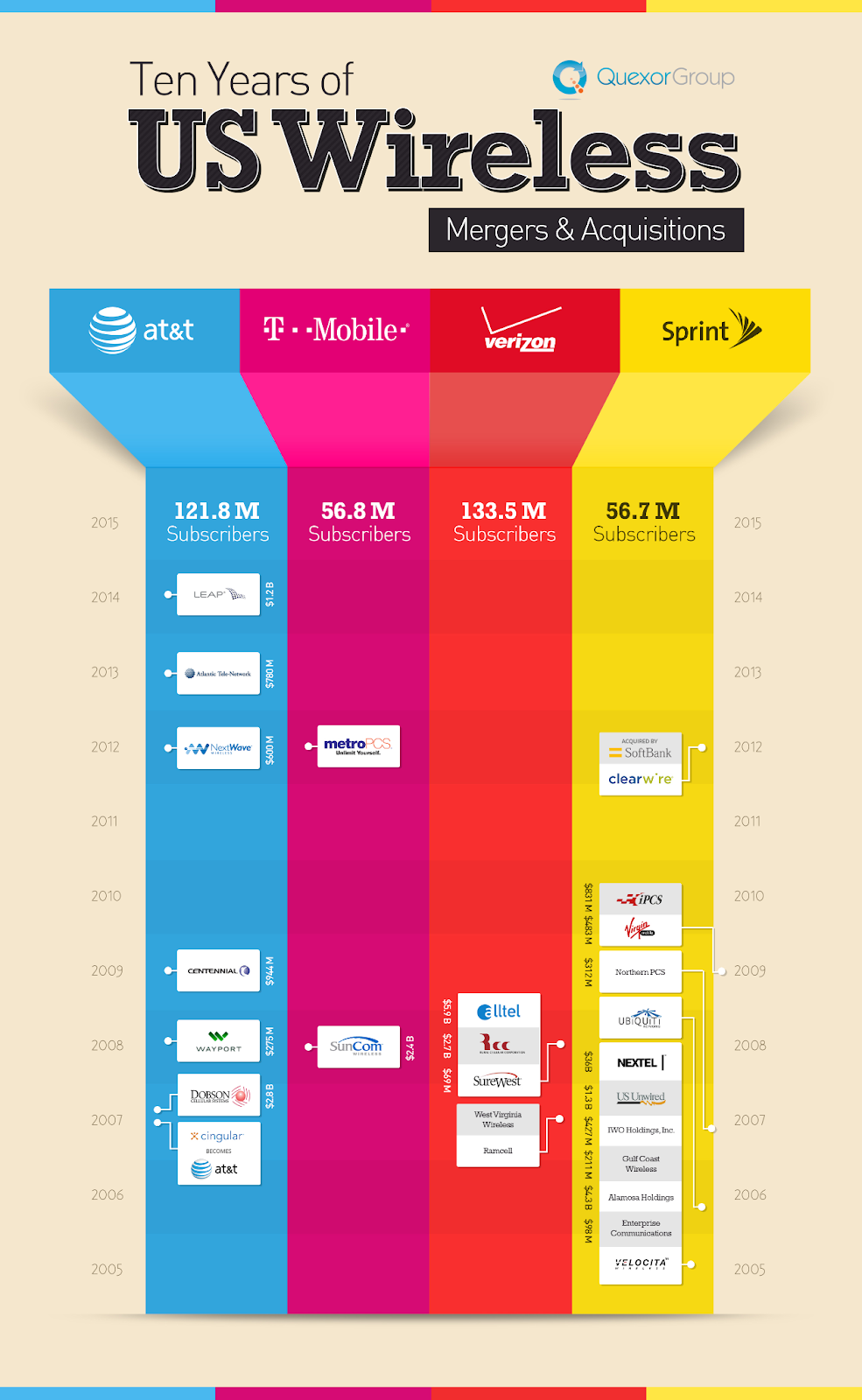

Most of us forget how complicated the early mobile “phone” business was, and how much asset rearrangement produced the current pattern. Consider the changes between 2005 and 2015, alone.

Over a longer period of time, the asset reshuffling was even more complex.

In the fixed networks business the dilemma is whether two viable facilities-based contestants can support themselves over the long term, or whether the only choice is a monopoly wholesale provider with retail competition.

It’s complicated. Some 25 years ago, U.S. policymakers believed that two national mobile operators were providing too little in the way of competitive benefits, leading to the granting of additional spectrum to enable a third national competitor.

Then market dynamics changed and a four-leader market developed, though a duopoly remained at the top of the market. With the merger of Sprint and T-Mobile, a three-supplier pattern now holds, though support for a fourth national provider (Dish Network) also was part of the deal-making around the merger.

In the fixed network market, however, just two competitors have provided genuine innovation and competitive benefits for consumers, perhaps assisted in part by the use of different infrastructure solutions. U.S. cable operators found ways to boost internet access speeds faster, and cheaper, than telcos could, leading to an installed base share as high as 70 percent.

Like the U.S. mobile industry, the fixed networks business was once more fragmented than at present. The AT&T breakup in 1984 resulted in eight large suppliers, AT&T in long distance and manufacturing and seven regional access companies.

These days, cable operators have emerged as key competitors for the remaining telcos, both in the fixed networks business and now are emerging as contestants in the mobility segment as well.

source: The Wall Street Journal

Where the wholesale, single-network framework has been used, competition has indeed developed as well, though one might argue that facilities-based competition tends to result in higher rates of innovation.

In the wholesale framework every retailer has access to the same products, purchased wholesale at the same prices. There is some room for differentiation of offers, but not much based on infrastructure features.

One certainty remains: a capital-intensive business such as “network access” tends to feature just a few providers. Periodic efforts to increase the number of suppliers always seems to result in reconsolidation.

It remains to be seen how much consolidation can happen while still providing competitive benefits.

{kind=link}

No comments:

Post a Comment