You can get a robust debate pretty quickly when asking “how important will 5G fixed wireless be?” in the consumer home broadband market. Will it matter?

Probably. But it also matters more to some than to others, and will matter even if the net result is installed base market share shifts of just a few percentage points. So there is no actual contradiction between cable operators saying “fixed wireless is not a threat” and a few firms arguing it will be highly significant as a driver of revenues.

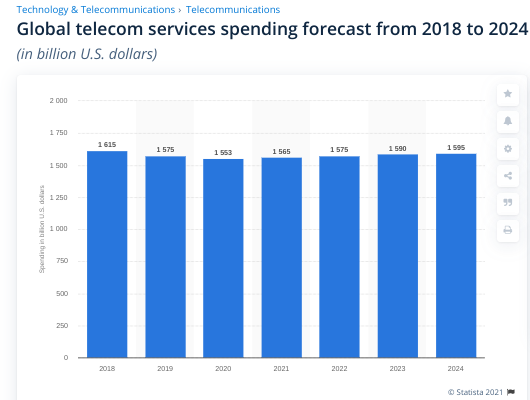

Keep in mind that the home broadband market generates $195 billion worth of annual revenue. Comcast and Charter Communications alone book $150 billion annually from internet access services that largely are generated by home broadband customers.

T-Mobile has zero market share in that market. Taking just two percent means new revenues of perhaps $4 billion annually. That really matters, even if cable operators minimize the threat.

“Addressable market” is a key phrase. Right now, Comcast has (can actually sell service to) about 57 million homes passed.

The Charter Communications network passes about 50 million homes, the number of potential customer locations it can sell to.

Verizon homes passed might number 18.6 to 20 million. To be generous, use the 20 million figure.

AT&T’s fixed network represents perhaps 62 million U.S. homes passed. CenturyLink never reports its homes passed figures, but likely has 20-million or so consumer locations it can market services to.

The point is that, up to this point, T-Mobile has had zero addressable home broadband market to chase. Verizon has had 20 million homes to market for that purpose. AT&T has been able to market to perhaps 62 million homes; Comcast 57 million homes and Charter about 50 million homes.

So T-Mobile and Verizon have the most market share to gain by deploying fixed wireless. And the value will not necessarily be that fixed wireless allows those two providers to “take half the market.” The revenue upside from share shifts in low single digits will be meaningful.

Some might counter that early fixed wireless will not match the top cabled network speeds. That is true. But it also is true that half of U.S. households buy broadband services running between 100 Mbps and 200 Mbps, with perhaps 20 percent of demand requiring lower speeds than that.

So even if fixed wireless offers lower speeds than cable hybrid fiber coax or telco FTTH, it might arguably still address 70 percent of the U.S. market.

It is conceptually possible that untethered access could eventually displace a substantial portion of the fixed networks business, longer term.

Up to this point, mobile networks have not been able to match fixed network speeds or costs per gigabit of usage. But that should change.

Mobile network speeds will increase at high rates, with a rule of thumb being that speeds grow by an order of magnitude every 10 years. One might argue that is less capacity growth than typically happens with fixed networks. +

But that might not be the relevant context. What will matter is how much speed, at what price points, mobile or fixed wireless solutions must offer before becoming a reasonable choice, compared to fixed access.

Assume that in its last release, 5G offers a top speed of 20 Gbps. The last iteration of 6G should support 200 Gbps. The last upgrade of 7G should support 2 Tbps. The last version of 8G should run at a top speed of 20 Tbps.

At that point, the whole rationale of fixed network access will have been challenged, in many use cases, by mobility, as early as 6G. By about that point, average mobile speeds might be so high that most users can easily substitute mobile for fixed access.

To be sure, cost per GB also has to be roughly comparable. But, at some point, useful bandwidth at a reasonable enough price could allow wireless solutions to take lots of market share from cabled network providers.

Matching cabled network headline speeds might not matter, as most consumers do not buy those services. Untethered options simply have to be “fast enough, priced well enough” to contend for significant share of the home broadband market.