Is it necessary for connectivity providers to become a full platform to generate significant revenues from cloud-based, internet of things and edge computing solutions? How much orchestration has to occur so connectivity offers add value? The answers may well determine how successful most telcos will be in the next era.

Also, how much orchestration of value can occur--and provide revenue growth--without a full shift to a “platform” role? That might be the more-important question, as few telcos can realistically expect to become the center of a big ecosystem, and operate as a true platform.

Today, virtually all telcos operate as “pipe providers,” not in the direct sense of supplying connectivity services, but in the broader sense of creating a product and then selling it directly to customers. Telcos have that in common with most businesses, in most industries, most of the time.

Accenture consultants have used a tripartite model of the potential evolution of telco services, beginning with “connectivity provider” and growing to become a “connectivity-plus-plus” provider. That would include adding roles in edge computing, security services and internet of things, for example.

The future role of “industry orchestrator” does not actually require a switch to a “platform” business model. It does require working with third parties to create new services bundling connectivity with line of business solutions, likely in some industry verticals.

What is important is that such an evolution does not require any telco to become a platform. It “only” requires adding more value to existing connectivity products, to provide higher value, and thereby reap a higher share of “solution” revenues.

In large part, the move “up the stack” or “across the value chain” towards end user applications is necessary simply because the core connectivity business is close to saturation, with little revenue growth from business-to-business or consumer lines of business.

Growth will necessarily have to come from new products beyond connectivity, as hard as that will be to achieve. That is one reason the industry has created the multi-access edge computing concept. It might allow a richer value proposition solving more business problems than “communications.”

source: IBM Institute for Business Value

Think of the way hyperscale data centers have created ecosystems of application, support and connectivity options for customers colocated inside the buildings. While often not a switch to a full platform model--which would require that the data center operator gets a percentage of all transactions between partner use of its platform--still uses the principle of the ecosystem to provide higher value for co-located partners, and thereby drives real estate value and revenue.

That poses other problems. If telecom companies decide to grow by acquisition, and they acquire software, technology or content assets, they face the impact of higher valuation assets.

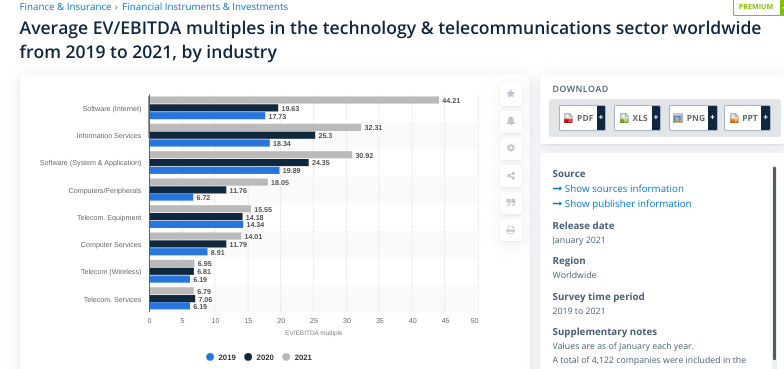

In 2021, for example, enterprise value multiples compared to cash flow multiples (EV/EBITDA)--the value of all stock and debt divided by free cash flow--were 44 times in the internet software business and just 6.8 times for the telecom industry, according to Statista.

Information services had a 32 multiple while software had a multiple of 31.

Essentially, telcos will be buying pricey assets with depreciated currency when acquiring assets “up the stack.” The alternative is an organic, “grow your own” strategy. That limits investment, but also tends to limit scale.

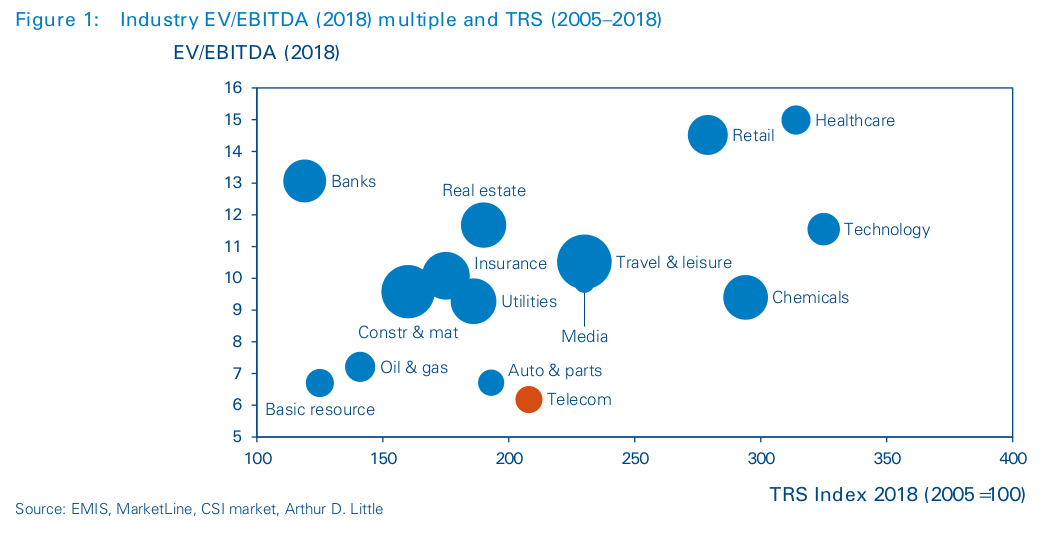

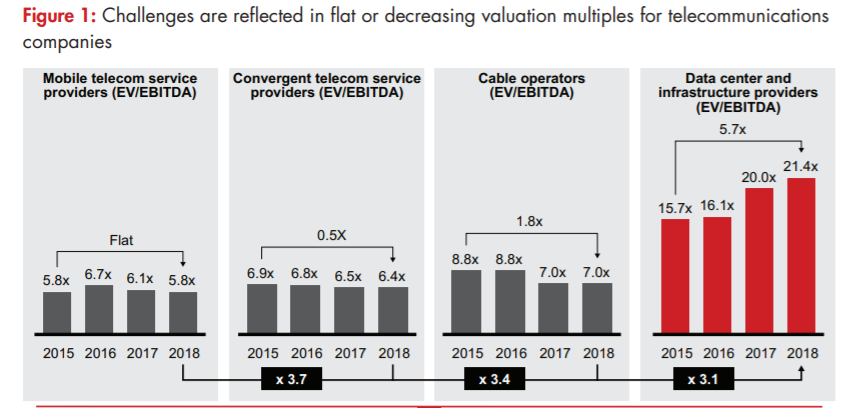

That valuation gap exists even within some related infrastructure areas, as data center assets, or infrastructure suppliers directly supporting data centers, have valuation multiples in the 21 range, where mobile operators are valued at about 5.8 times EV/EBITDA.

The obvious issue is that acquiring assets “up the stack” at the application layer is costly. If one assumes that connectivity providers eventually will have to make such moves, the challenge is how to amass enough free cash flow to do so.

The other path is organic growth, where the telco grows its own new services. The traditional issue with that approach is simply that it takes time, and rarely has been the way telcos gain significant scale in any new line of business. Consider software-defined wide area network services. Arguably not a single telco anywhere in the world can claim to generate as much as $1 billion in annual revenues from its SD-WAN offerings. Very few can claim such amounts from legacy multi-protocol label switching (MPLS) services, either.

Smaller connectivity providers will have scant chances to pursue such strategies, though. As small independent providers in any industry are squeezed out as scale providers emerge, smaller connectivity providers will have few choices but to manage costs as best they can until an exit event.

No comments:

Post a Comment