Mobility has been for a couple of decades the revenue driver for the global telecom industry, in some cases representing as much as 100 percent of revenue growth overall. But growth rates are slowing, everywhere, as more consumers become customers in every country and region, choking off the "grow by adding subscribers" business model.

Increasingly, the issue is convincing existing customers to buy mobile data services and other products, spending more in the process. Since we are at the beginning of the 5G era, we should expect capex to grow. The issue is whether this is a cyclical trend, or something more permanent. And, of so, what mobile operators will have to do to keep their business models in sustainable mode.

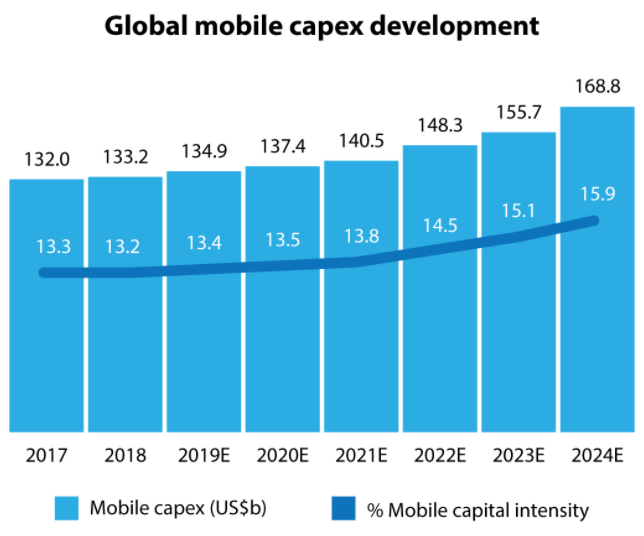

S&P Global expects mobile operators to boost capital investment levels as new 5G networks are built. Some acceleration of capex to build a next-generation network is not unusual. The issue is whether this is less cyclical, and more permanent an issue.

The companion issue is financial return from such capex. Mobile operators are going to be challenged to earn returns on the higher capex, S&P Global notes. The long standing issue is that although customer data consumption climbs as much as 50 percent a year, forcing networks to invest, revenue earned from providing those services is relatively flat. Buyers are not going to pay twice as much for twice as much speed, for example.

Also, average revenue per account or user is dropping globally, while global revenue growth is flat, and is projected to have zero to one-percent growth for the foreseeable future.

All that makes higher capital investment an issue.

No comments:

Post a Comment