As bidding for 280 MHz of U.S. mid-band spectrum in the C-band exceeds expectations, it might be reasonable to wonder if mobile operators risk overpaying for 5G licenses. Given past experience with some spectrum auctions in Europe for 3G licenses, as well as some 4G auctions, it is a reasonable question.

But some will argue the C-band spectrum is strategic for a number of reasons. At a high level, it rarely is possible to run a large mobile business--and control costs or attempt differentiated packaging--without access to licensed spectrum.

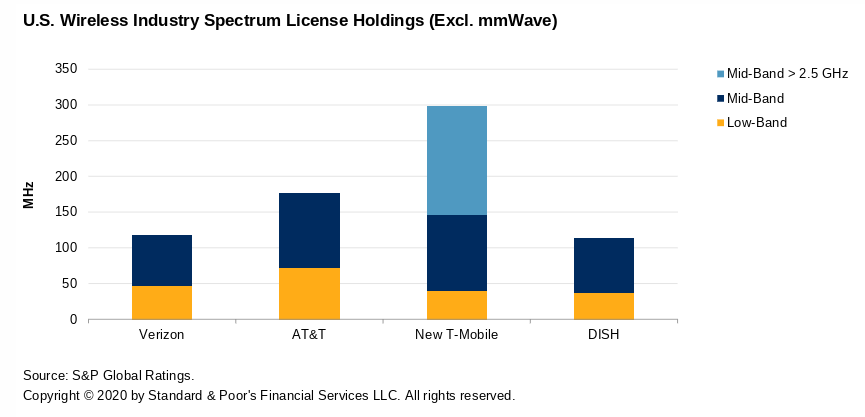

At a more-granular level, U.S. mobile operators have, up to this point, faced clear constraints in commercializing 5G services using the mid-band spectrum, especially in the 3.2 GHz to 4 GHz bands that have proven the best way to supply both 5G coverage and capacity. Most of the mid-band spectrum in those ranges have been licensed to other users in the U.S. market, where that has not been the case in most other places in the world.

That has meant the U.S. operators (with the exception of T-Mobile, which has a trove of 2.5 GHz spectrum) two relatively unappetizing choices: use the low-band or millimeter wave spectrum.

The downside: low-band provides good coverage, but no capacity advantages. Millimeter offers huge capacity increases, but at the price of coverage. The former means customers will not see faster speeds 5G promises; the latter means higher infrastructure costs and a slower commercialization timetable.

In a nutshell, AT&T and Verizon--among others--really need lots more mid-band spectrum to deliver on their 5G promises of higher speeds and coverage, in the near term. T-Mobile will be more than willing to tout the typical scale of its nationwide 5G network.

In principle, AT&T and Verizon might overpay for C-band spectrum, but at least so far, that is not an issue. C-band prices remain below the prices paid for AWS-3 spectrum that was vital for 4G, for example. Mobile operators always are wary of overbidding for spectrum rights, recalling the high prices paid for 3G spectrum in Europe, for example, which nearly bankrupted the auction winners. On the other hand, spectrum assets can be quite strategic, as facilities-based competition leadership without adequate spectrum resources is impossible.

The robust bidding for 280 MHz of C-band spectrum is an indication of the importance mobile operators place on mid-band assets. T-Mobile’s purchase of Sprint likewise was driven in large part by access to the trove of mid-band spectrum Sprint possessed.

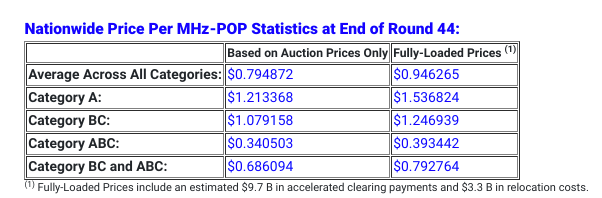

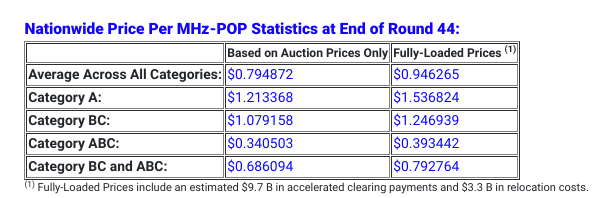

Spectrum prices in the recent CBRS auctions (also of new mid-band spectrum) generated average prices per person (per MHz-POP) of about 21.6 cents. The C-band auction already has average prices of about 79 cents per MHz-POP, higher when including the additional clearing payments to existing licensees. Including those payments, we already have hit about 95 cents per MHz-POP in the C-band auction.

Prices for the A block of frequencies, which it is estimated can be put into commercial use as much as two years earlier than the BC block, are running higher. After the end of round 44 of bidding, A block licenses were at an average of $1.21 per MHz-POP, with a price of $1.54 including the cost of clearing existing users from the spectrum.

{kind=link}