Telco interest in edge computing--especially multi access edge computing that uses telco facilities in some way--is driven in large part by the search for new revenue sources. Though mobile revenue growth rates remain significant in Africa, growth rates now have slowed in most other regions, perhaps going negative in some regions

The same might be said of interest in the internet of things or private networking in some cases: connectivity providers hope significant new revenue sources can be created in these areas. But it will not be especially easy. The size of new connectivity revenues might be smaller than many casually expect. New roles in edge computing, IoT or private networking will be more expensive and arguably outside core competency areas.

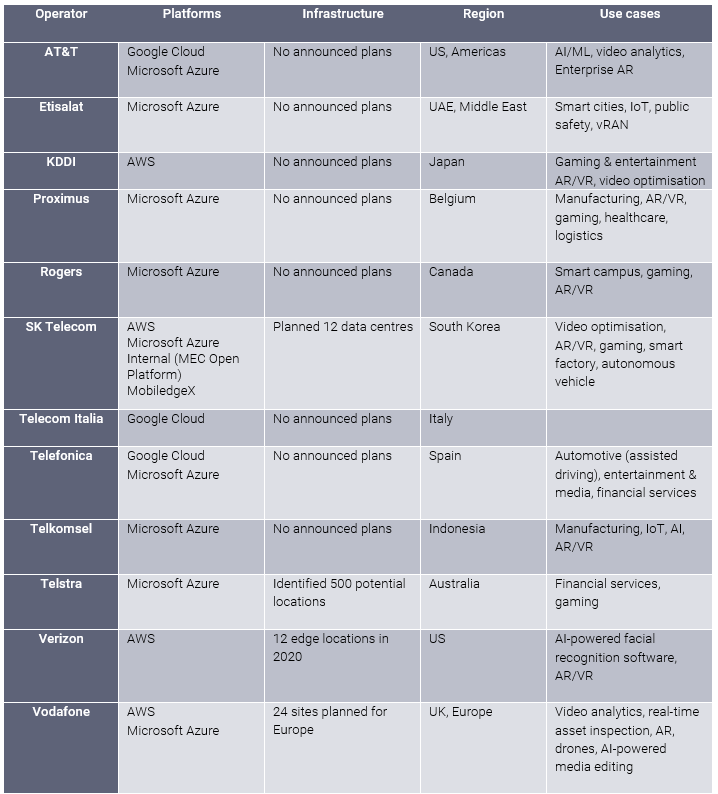

Few telco efforts to create new roles in computing have worked well, if at all. And multi access edge computing--or edge computing as a whole--still is “computing.” If computing as a service is the domain of the hyperscalers, so should much of edge computing be the domain of those same hyperscalers.

The risk and capital investment for any telco move into the “edge computing as a service business” arguably now is seen as too daunting, which is why the main trend seems to be partnerships with hyperscale platforms.

While clearly less risky and capital consumptive, such partnerships essentially have telcos acting as real estate providers (edge facilities) and suppliers of connectivity, in most cases. One might argue that is about the best they can hope for, at the moment.

Though other roles might eventually emerge, the immediate tack seems to include an acknowledgement that the opportunity to become “edge computing as a service” suppliers is highly limited, if possible at all.

No comments:

Post a Comment