Competition really changes the economics of consumer access networks, limiting revenue and constraining profit margins while increasing the amount of stranded capital investment. In the fixed networks business, capital is stranded when deployed, but earning no revenue.

Consider any one-product service provided by a single provider with 80 percent installed base or take rate. Add one competent new supplier, and theoretical “maximum” share for each provider drops to 40 percent. Add a third competent supplier and theoretical maximum share drops to 33 percent.

As a practical matter, dropping from 80 percent household take rates to 40 percent automatically doubles the cost per customer. When there are three competent suppliers in any single market, theoretical market share can triple per-customer costs of any network.

That change alone would destroy the original economics and business model. Triple play now is foundational because it directly addresses competitive market dynamics: three products can be sold to a smaller number of potential customers.

If each unit sold (for example) is about $40, then per-account revenue could be $120, not just $40 if a single product were the only supplier option. Such bundling practices help service providers compensate for lower take rates.

And that is the principal threat Verizon’s fixed 5G initiative poses for AT&T, Comcast and Charter. If Verizon is successful at taking accounts, the theoretical maximum market share for any of the providers drops from 50 percent (two equally skilled providers split the market) to 33 percent (three equally skilled providers each take a third of the market).

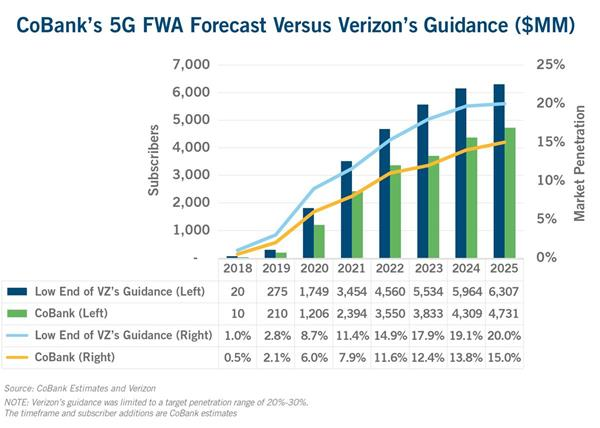

As always, opinions vary about the potential amount of substitution, in urban or rural markets, with the greatest skepticism about impact on rural markets. In many cases, that is because of signal propagation characteristics of millimeter wave spectrum in such bands as 28 GHz and 39 GHz.

It is reasonable to suggest that many believe lower-frequency signals in the 3.5-GHz band might be more important in rural areas, as 3-GHz and 5-GHz frequencies already are used by fixed wireless providers in rural areas.

Analysts at CoBank are in the camp that believes millimeter wave spectrum will not have very much impact on rural internet access, and also believes fixed wireless using millimeter spectrum will be less successful than Verizon estimates.

Still, others might note that, in urban and suburban areas, even using skeptical estimates, Verizon alone might be able to take significant market share from other internet service providers using cabled approaches.

In the first five years or so, such gains might only represent share gains between 11 percent to 18 percent, in the areas where Verizon builds fixed wireless networks. In substantial part, such skepticism is founded on transmission distances that might range from 500 foot to 1,000 foot cell radii.

To be sure, skepticism on the part of many observers, such as rural telcos who rely on cabled approaches, is to be expected. After all, fixed wireless is yet another alternative to existing telco or cable TV networks.

CoBank analysts believe the general absence of cable TV operators from the ranks of bidders for new millimeter spectrum indicate those firms are not worried about millimeter wave spectrum approaches. If they were threatened, CoBank analysts argue, cable operators would be bidding for spectrum, either to deny the use of such spectrum to would-be competitors, or to use the platform themselves.

Some of us would disagree with that logic. For institutional reasons, cable executives have disliked running services over any platforms they do not own, with a strong preference for HFC whenever possible. Already looking at use of leased facilities to support their early mobile efforts, cable executives might resist adding more one platform, especially if they conclude the revenue upside is limited.

Cable operators also seem to favor lower-frequency bands, such as 3.5 GHz, in part for reasons of cost, in part for reasons of signal propagation.

Nor would cable operators be able to simply “warehouse” spectrum very effectively, on a long term basis. “Use it or lose it” is the standard policy for new spectrum awards. And even if cable operators wanted to warehouse 28 GHz or 39 GHz spectrum, lots of other spectrum in the millimeter bands will be released for commercial use, and much of that spectrum will be available on an unlicensed basis (or licensed on a no-fee basis).

source: CoBank

![The Dangers of the Internet of Things [infographic]](https://cybersecuritydegrees.com/wp-content/uploads/2018/08/DangersIoT.png)