If asked, most observers would likely guess that 5G, with its many new small cells, will cost more than 4G did. The only key differences might be the magnitude of the increases.

That might not be the case. Morgan Stanley estimates that the industry will spend $225 billion on 5G between 2019 and 2025, with the biggest outlays coming later. But the global mobile industry “spent about $275 billion on 4G,” analysts at Morgan Stanley have said. In other words, the industry will likely spend less on 5G than it spent on 4G, according to analysts at Morgan Stanley.

That might seem counterintuitive.

Korea Telecom, for example, estimates that 5G networks need four times the amount of cell sites for any given area compared to 4G networks, with a corresponding increase in the amount of backhaul to those sites. So the Korean Ministry of Information therefore has said that SK Telecom, KT Corp, LG U+ and SK Broadband can share the cost of building a 5G network, saving an estimated $1 billion in capital and operating expenditures over 10 years.

Xona Partners estimates that 5G will require six times the investment to deliver comparable coverage to existing 4G/LTE networks, in part because so many more cells will be necessary, and because some suburban small cells will need at least 32 accounts to sustain profitability .

But there are other concerns possibly at work, in addition to capex expectations. Time to market should be faster, in a four-provider scenario, than if each provider separately built its own radio access network and backhaul.

Also, such sharing should reduce upfront costs enough to compensate for a possibly-minimal increase in revenues. The Korean mobile market is characterized by relatively low retail prices, so capex cost control matters.

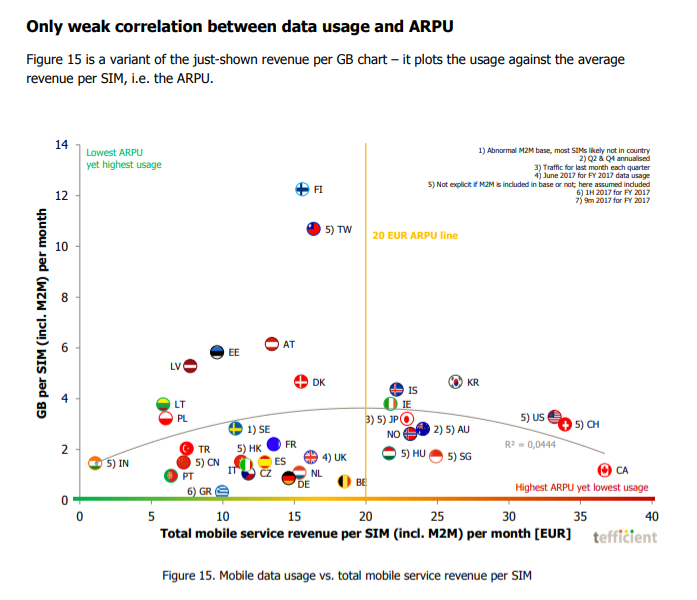

Capex concern, though it exists, might not have the same intensity in other markets. U.S., Swiss and Canadian service providers, for example, have gross revenue per account levels that are far above those in Korea and many other countries. Service providers in such countries might worry less about 5G capex, in relation to expected revenue upside, in part because relative revenue per Gbyte is more robust.

The point is that costs to deploy 5G might be less than 4G, not greater than 4G. Incentives to build 5G also will be higher in more-mature 4G markets, much less so in markets where 4G has been introduced relatively recently. On that score, the United States is among the most-mature 4G markets globally, so the network has been amortized.

The other issue is operator expectations about where revenue upside and profit might lie. With differentiation shifting away from the expensive radio infrastructure to the to the software and service layer, some service providers might conclude that spending as little as possible on the physical layer infrastructure makes sense.

The strongest such case, in a continental-sized market such as the United States or Australia, is to be found in rural areas, where a payback on facilities is nil to non-existent. Service providers might also be relatively indifferent in many cell areas where traffic is relatively light.

But U.S. service providers are unlikely to want to rely on others for infrastructure in the 10 percent to 15 percent of their networks that handle most traffic.

So space division is one reason some U.S. mobile service providers might be reluctant to embrace widespread infrastructure sharing (towers, yes; other facilities in rural areas, yes; large venues, maybe; busiest 10 percent of sites, probably not). There are places where sharing does not harm the business case; other places where it might; and some places where most of the actual customer interactions occur.

No comments:

Post a Comment