An agency of the U.K. government wants 15 million premises connected by optical fiber by 2025, with coverage across all parts of the country by 2033, as well as 5G coverage of “the majority of the population” by 2027.

As always, those goals set by the U.K. Department for Digital, Culture, Media & Sport are a statement of direction: actual investments and timetables will likely vary. But it also might be fair to say that the amount of investment risk larger than in the past, for several reasons.

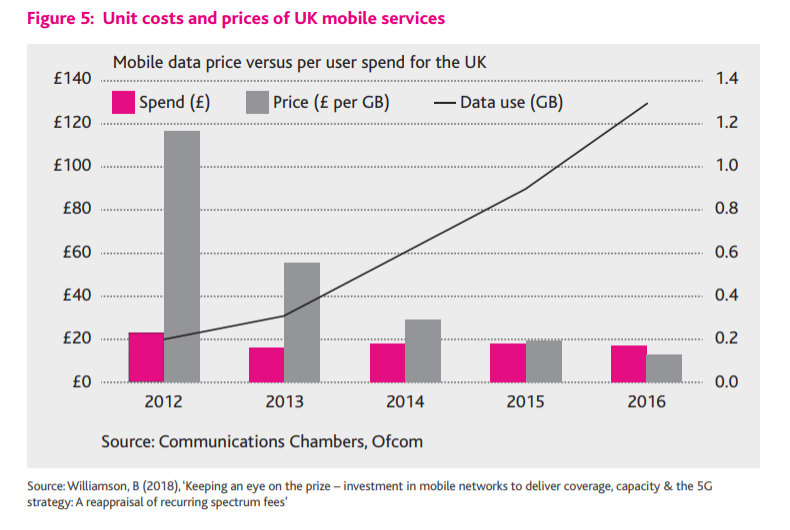

One key issue is that U.K. service provider revenue has decreased 1.7 percent a year since 2012. That raises the usual questions about additional investment in an industry with shrinking revenue.

The report sees some amount of facilities-based competition. “At least a third (with the potential to be substantially higher) of U.K. premises are likely to be able to support three or more competing gigabit-capable networks,” the report predicts. “Up to half (or lower if there are more three network areas) of premises are likely to be in areas that can support competition between two gigabit-capable networks.”

That poses the “normal risk” of stranded assets (service providers will not earn revenue from every home or business the network is built to support.

A convergence of fixed and mobile infrastructure also is foreseen. “In the longer-term, the government expects to see a more converged telecoms sector,” as fixed networks and 5G are complementary.

That means suppliers about to leverage both mobile and fixed assets could gain advantages.

Also, for the first time at scale, 5G could be a replacement for fixed networks. “The technology synergies between 5G and fixed networks are likely to create strategic advantages for those operators that have interests in both,” the report says. And one potential advantage is the ability to deploy commercial gigabit networks at lower cost than using fiber-to-home networks.

The industry has not, to this point, faced a scenario where mobile networks literally are a full and functional substitute for fixed networks, which have had the advantages of speed and much-lower cost per bit.

The point is that capital investment decisions carry higher risk, as competition could take new forms, at scale, and alter payback periods, account potential and profit margin.

But risk exists on the revenue side as well. Among the biggest unknowns is the amount and extent of revenue upside, with much of the benefit to come in the form of capacity gains, as mobile operators deploy 5G first where they face the greatest data demand.

Other new services will develop over time, it is assumed and hoped. “There is some uncertainty over the business models for 5G,” the report suggests. That will tend to lead investors to be careful about how fast, and how much, to invest in new 5G facilities. To limit risk, it will make sense to deploy 5G first in dense urban areas where capacity is an existing concern.

Such moves will better match investment to revenue upside.

Also, 5G might “also open up opportunities for new players to enter the U.K. market,” by which the report authors mean new neutral host infrastructure providers at venues, rural or outdoor small cell coverage. That could again affect business model assumptions about investment cost.

No comments:

Post a Comment