It long has been a sound bit of advice for firms operating in declining industries to harvest revenue, rather than invest. AT&T did that in its long distance business, and now is doing so in its voice and messaging business, as well as its linear video business.

But what to do about fixed network internet access investments is a big issue in many markets where the fixed network business is big, but declining, or small and barely growing. That is especially true when more growth is expected in the mobile segment.

Many observers were critical of AT&T for buying DirecTV, and are critical of AT&T’s effort to buy Time Warner. Some of the criticisms are similar to complaints made when AT&T was considering the purchase of DirecTV.

Capital should instead have been investing in the core fixed line network, instead, many argued when AT&T was considering the acquisition of DirecTV.

But it is not clear how much upside exists for AT&T, in terms of fixed network internet access revenue. You might argue that the best case for AT&T, for a massive upgrade of its consumer access network, is about 10 percent upside in terms of consumer market share.

That is by no means insignificant, depending on the assumptions one makes about the cost of the upgrades. Still, given that as important as it is, fixed network internet access now is a mature business, there are limits to how much capital a telco “ought” to invest, compared to deploying capital elsewhere.

Realistically, a major telco has to expect it will, under the best of circumstances, and in a two-provider market, split share with a competent and motivated cable TV provider. If cable now has about 60 percent share, and AT&T about 40 percent share, that implies a sort of share ceiling of 50 percent. That is one driver of revenue. The other is revenue per account.

But typical account revenues have not risen as much as one might expect, given consumer shifts to higher-speed services that tend to cost more.

Basically, internet access prices in the developed world have tended to move roughly in line with growth in gross domestic product, and are flat to declining in terms of spending as a percentage of gross national income per person, according to the International Telecommunications Union.

Though some believe there is much-more account revenue upside, experience so far suggests prices will be hard to boost, in the fixed network segment. Increasing competition from third parties is one reason. A shift to mobile access is another issue. Finally, consumers will only spend so much on communications services in general.

At least some might point to stock performance of T-Mobile US, compare that to AT&T, and draw the conclusion that AT&T would be better off putting its capital into network upgrades, not content acquisitions.

That mistakes a growth strategy based on taking market share with a strategy based on entering or creating new markets. Even if markets are not growing, attacking firms can grow simply by taking market share.

That is what cable TV companies have done in business service markets, voice services and internet access, for example. Growing by taking share was not possible for AT&T and Verizon, which already were the market share leaders in those markets.

That is germane when looking at T-Mobile US strategy, compared to that of AT&T or Verizon.

For starters, T-Mobile US--with no fixed network footprint--has only one avenue for growth: taking market share from other mobile service providers, something it has done.

And, in a zero-sum U.S. mobile market, T-Mobile US, with market share of about 15 percent, has room to grow at the expense of the other service providers, until some future time when it will be acquired or merged with another sizable firm.

In fact, should current predictions about the 5G era prove correct, T-Mobile US and Sprint might well require major fixed network assets to support small cell networks.

The point is that T-Mobile US has limitations and opportunities in its core business that are quite different from those of AT&T. Neither Verizon nor AT&T has seen much share change over the last decade.

So what makes sense--and is doable--for T-Mobile US is not necessarily sensible--or doable--for AT&T or Verizon.

As voice and messaging already have entered the declining part of their product life cycles, so too internet access and mobility itself have reached near saturation in the U.S. market. That means finding brand new sources of revenue growth beyond the legacy core.

That is not to say AT&T or Verizon can afford to neglect upgrades of their consumer internet access capabilities. But it would also be incorrect to argue that such upgrades can drive overall revenues over a decade’s time.

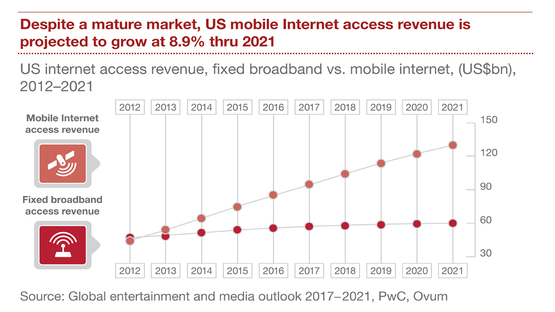

One might argue that U.S. mobile internet access revenue will grow. It is harder to make the argument that fixed network revenue will do much, based on past experience.

AT&T is a firm with many big decisions to make, and none of them are especially easy. Where to deploy capital for revenue growth is a prime example.

No comments:

Post a Comment