Some competition, most would argue, is better than monopoly. Robust competition likely is normally viewed as desirable. But ruinous levels of competition generally do not last too long, as most suppliers simply go out of business.

It might be possible to view mobile service provider competition levels in India as quite-competitive. Whether the level of “ruinous” competition has been reached--with the market entry of Reliance Jio--is not clear.

But it might be logical to ask whether that is nearly the case. If so, one also would predict that many of the current smaller providers will go out of business, possibly through complete collapse but more likely as they are absorbed by one of the surviving competitors.

The point is that, unless governments try to prevent consolidation, too much competition often leads to ruinous outcomes for any industry subject to extreme levels of competition.

That the Indian mobile market is going to consolidate, in a significant way, now seems inevitable. With Reliance Jio’s entry into the market, and the inevitable price war that will follow, only the larger players will have the scale to survive. So smaller players will exit the market.

That could shrink the market by half.

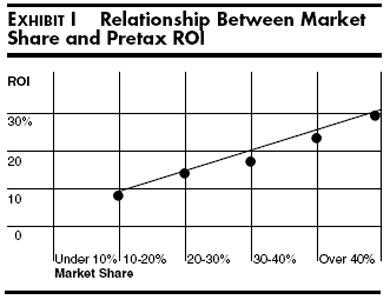

Over time, markets tend to consolidate, and they tend to consolidate because market share is related fairly directly to profitability. One rule of thumb some of us use is that the profits earned by a contestant with 40-percent market share is at least double that of a provider with 20-percent share.

And profits earned by a contestant with 20--percent share are at least double the profits of a contestant with 10-percent market share.

That is why one of the main determinants of business profitability is market share. Generally, entities that have high share are much more profitable than their smaller-share rivals.

Source: Marketing Science Institute

And that is likely to be especially true for business products that are not purchased frequently, or are hard to understand, such as business communication products and services.

For infrequently purchased products, the return on investment of the average market leader is about 28 percentage points greater than the ROI of the average small-share business.

For frequently purchased products (those typically bought at least once a month), the correspondingly ROI differential is approximately 10 points.

There are reasons for that differential.

Infrequently purchased products tend to be durable, higher unit-cost items such as capital goods, equipment, and consumer durables, which are often complex and difficult for buyers to evaluate.

One might argue that communications services also are products buyers generally find complex to understand and hard to evaluate on metrics other than recurring cost or upfront investment.

Since there is a bigger risk inherent in a wrong choice, the purchaser is often willing to pay a premium for assured quality.

Frequently purchased products are generally low unit-value items where risk in buying from a lesser-known, small-share supplier is less crucial.

Source: Marketing Science Institute

Such differentials also occur when buyers are fragmented, and no small group of consumers accounts for a significant proportion of total sales.

In such cases, the ROI differential is 27 percentage points for the average market leader.

However, when buyers are concentrated, the leaders’ average advantage in ROI is reduced to only 19 percentage points greater than that of the average small-share business.

When buyers are fragmented, they cannot bargain for the unit cost advantage that concentrated buyers receive.

Source: Marketing Science Institute

|

No comments:

Post a Comment