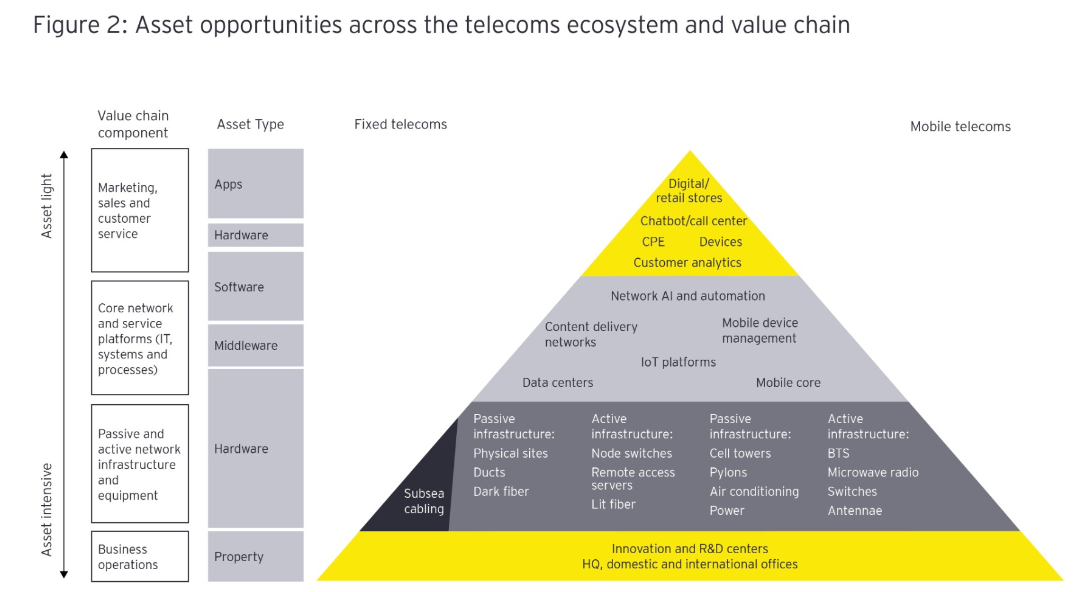

To the extent that high capital investment essentially creates a business moat against competition, any lowering of capex barriers opens the access business to further competition. So while any particular access provider might welcome lower capex, such as giving up infrastructure ownership in favor of wholesale access, there are trade offs.

That is the bargain mobile operators in Malaysia are making, as 5G infrastructure becomes a wholesale-only access proposition. On one hand, operators can avoid some of the capital investment to build their own networks. On the other hand, some degree of commoditization also results, as every competitor will have the same services, sold at the same price, with the same features.

And since the wholesale price sets a floor under retail price, there will be additional constraints on both pricing and packaging of the basic access product.

One has to wonder whether an asset-light business model is emerging in many parts of the connectivity business on a wider scale. In addition to operating as would a mobile virtual network operator, more access providers might choose to specialize, narrow the scope of their services or radically reshape their customer-facing marketing, sales and support processes to achieve lower costs.

Telcos using public hyperscale cloud computing services instead of managing their own private clouds provides another example of this trend. To a degree once unthinkable, access providers are reshaping, in some instances, their roles as infrastructure owners.

In part, that is because open access fiber-to-home networks enable operating modes that cost less, while still offering required levels of network performance. The trade off is a loss of pricing flexibility, as retail prices have to reflect the wholesale costs of securing access.

Since all competitors have the ability to purchase the same services, wholesale customers also lose some amount of ability to differentiate service levels. If every ISP offers symmetrical gigabit per second or multi-gigabit-per-second access, that ceases to be an area where competitive differentiation is possible.

So the bad news for access providers going asset light is that their products might become more commoditized than they are today. The “plus” of lower capital investment is accompanied by the “minus” of higher degrees of commoditization.

But such trade offs have been happening for a while. Access providers have been selling physical infrastructure assets to raise cash to reduce debt, for example. Were debt not a problem, would they sell? Perhaps not.

But most access providers struggle with the economics of building the next generations of mobile and fixed networks. Getting out of substantial parts of the digital infra ownership business seems the lesser of several evils.

It is happening to fixed network providers as well.

On*Net Fibra, the Chilean digital infrastructure company 60 percent owned by KKR and 40 percent by Telefonica, is buying rival service provider Entel’s fiber to home network for US$358, and will continue to operate as an open access wholesale network.

Entel’s FTTH network passes 1.2 million homes and businesses. On*Net Fibra will, after the deal closes, pass 3.9 million premises. The goal is to grow home and business passings to 4.3 million by 2024.

Telefonica had sold “non-core” Central America network assets in 2021, selling 40 percent of its towers business Telxius to KKR in 2017 before agreeing to flip the whole business to American Tower for €7.7 billion in 2021. Entel also sold its data centers to Equinix.

No comments:

Post a Comment