Fixed wireless using 5G will by 2026 support 180 million connections globally and generate US$70 billion in revenue, accounting for 40 percent of the total fixed wireless access market, according to ABI Research.

Some believe subscriptions could be substantially higher, though.

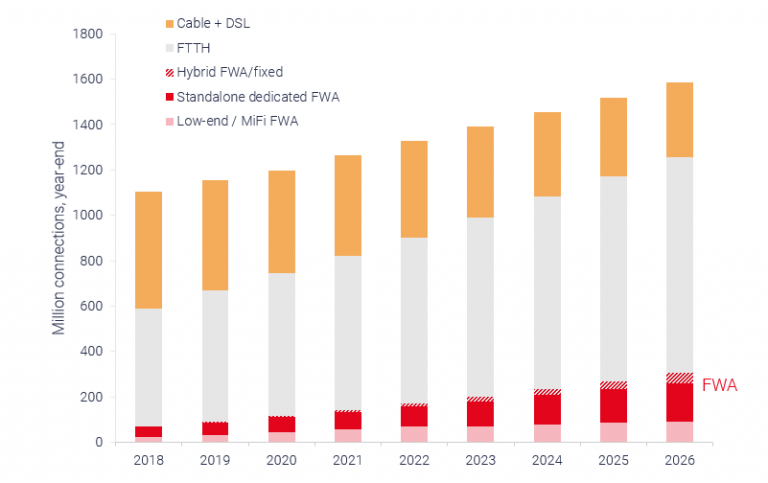

Adoption likely will be highest in markets where the cost of deploying fiber to home or hybrid fiber coax remains unworkable, and where demand for moderate-speed internet access is high. Some might argue that 5G fixed wireless is most directly the successor for 4G fixed wireless and digital subscriber line. In some markets that opportunity might last for a substantial amount of time.

In other markets there might be a window of opportunity that essentially closes within a decade, as cabled network capabilities continue to improve with faster fiber to home deployment and upgrades of hybrid fiber coax networks.

Some portion of the opportunity, in some markets, will remain as a platform for “out of region” by mobile operators who are able to compete for some portion of the home broadband market, especially customers who only want to buy moderate-speed services at lower prices.

The adoption forecast arguably is more difficult in markets where high rates of FTTH deployment or HFC are expected and where demand for gigabit per second speeds is robust. In such cases, 5G fixed wireless will be most-often adopted as an “out of region” strategy by mobile operators to compete with fixed network suppliers.

A decade from now, we might see that 5G fixed wireless expands its share of the installed base, compared to other access platforms. But as with satellite access, the market might remain a fraction of the total addressable audience.

Each new generation of satellite services has continued to appeal to the same potential customers: rural dwellers in areas where it is difficult to build cabled networks. That remains a low single-digit opportunity. Low earth orbit constellations will bring higher speeds and lower latency, but speeds and latency performance are increasing across the board, on every platform.

There is little reason to believe the relative market shares or installed base of home broadband customers gotten by satellite providers will change very much as the LEO constellations reach full commercialization.

Fixed wireless, on the other hand, should appeal to a wider audience of customers presently only able to buy copper fixed network service. And even that market window will narrow as more ISP FTTH connections are added, replacing copper.

Also, in some markets, where HFC networks are ubiquitous, it seems unlikely that 5G fixed wireless can keep pace with the next generation of HFC internet access, which will enable speeds up to 10 Gbps.

No comments:

Post a Comment