Connectivity services earned by mobile and fixed network operators will get a boost from edge computing. What remains unclear is the magnitude of the boost.

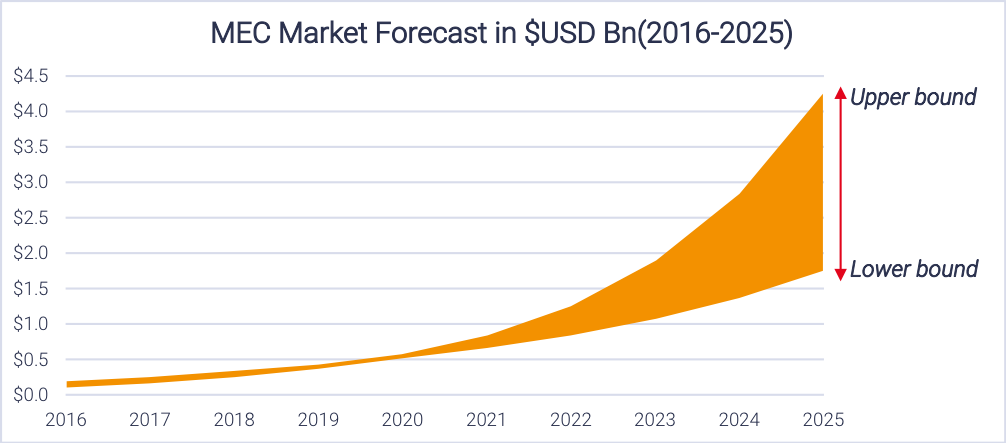

Software and services suppliers likewise see significant revenue opportunities, as do suppliers of computing infrastructure. Connectivity services could be in the range of $50 billion globally by about 2023, according to one KPMG analysis.

Generally speaking, most analyses of connectivity revenue--as a percentage of total edge computing activity--is about 10 percent to 11 percent. A new $50 billion revenue opportunity is significant, when it develops over only several years.

To be sure, much of the connectivity could be earned by fixed network providers supplying backhaul to regional or metro area computing centers. But a substantial amount of on-premises connectivity could be earned by other suppliers of local connectivity (Wi-Fi, Bluetooth, others) capabilities.

A significant portion of local area backhaul connections could be earned by low-power wide area networks rather than mobile or fixed services suppliers.

The general point is that connectivity as such is a 10-percent opportunity divided among several industry segments. About 90 percent of the edge computing opportunity lies elsewhere: hardware, software and services.

The issue is “how big” the revenue upside might be, for computing and connectivity providers. We cannot tell much right now, as edge computing service revenues are too small to note. Nor can we determine the ultimate range of roles connectivity providers might assume.

Right now, all revenue earned by all connectivity providers in any way connected directly with edge computing is quite small, by global standards. Basically, access providers might have roles as real estate providers (racks, huts, space); connectivity providers (5G and fixed); actuall suppliers of compute services; system integrators; platform providers or application providers.

Connectivity providers might hope to operate as the actual providers of edge computing services (compute cycles, for example). More complicated roles as platforms are feasible. Most complex of all are applications that might be created and owned by the connectivity provider. Simplest are traditional connectivity services roles.

It simply is too early to know how much success connectivity providers will ultimately have in the edge computing ecosystem, or what roles will prove most successful.

No comments:

Post a Comment